We are not certified professionals. For more information about us please read our Disclaimer.

Our daily living expenses, as full-time travelers

Money can feel like a “chicken or an egg” kind of topic. At what point shall we jump on the merry-go-round to start the conversation? There are so many options! The topic of daily living expenses for our new life is a huge one, so for this post I am focusing on our own actual daily living expenses as full-time travelers. And I promise to try to make it fun.

Fixed and variable expenses

For us, paying attention to our “fixed expenses” and also our “variable expenses” is important for tracking our actual daily living expenses. To only focus on our variable expenses and only track costs relating to being on the road would not give us real daily living expense numbers. It’s very important to me that our budgets and tracked costs all be 100% accurate with no dollars hidden under the rug.

Variable expenses

These include things like housing (or “pillow costs” as I like to say), transportation, any excursions we take, going out to dinner, and shopping so we can cook at home.

Fixed expenses

These include things like our 5×10 storage unit back in Seattle, our Netflix account, and our global medical insurance premiums.

Shedding the extras and making a shift

Before we left Seattle we worked hard on cutting as many fixed expenses as possible so we wouldn’t take too many of them with us on the road. We sold our condo which meant no more HOA fees (we had already paid off our mortgage and have no debt of any kind) and no more utilities, property taxes, or condo insurance. We also sold our car which meant no more car insurance and no more gas purchases. We dropped our Hulu account, and we also dropped both of our AT&T cellular accounts. But we did add to our fixed expenses by getting a new Google FI cellular account with global phone coverage. We rented a new 5’x10’ storage unit so we could keep some of our personal belongings for future plans. We also opened a new Traveling Mailbox account to manage our banking and government related mail.

The biggest expense – medical

And the biggest expense of all is paying for our new global health insurance. Shockingly, our health insurance with associated deductibles and related out-of-pocket healthcare costs represents almost 15% of our current daily living expenses. And because of that, our fixed expenses represent nearly 60% of our total daily living expenses. WOW! But I’m jumping ahead on the budget. And I will have more to say about budgets, or Money Jobs as we like to call them, in a later post.

Tracking our spending

In order to develop my own opinions about daily living expenses and build our current budget, I did a lot of research and benefited from the experiences of many others who have posted about their own budgets. Many of the people I have gained valuable ideas from are either full-time travelers themselves, and/or members of the FIRE (financial independence/retire early) community.

One idea we have adopted is to track every penny we spend every single day – as suggested by Billy and Akaisha Kaderli. Billy and Akaisha retired back in 1991 and they have been testing and proving their ideas ever since. Tracking our daily spending helps me identify changes in our spending habits over time. And as we continue traveling this year it will also clarify which locations around the world helped our dollars stretch the furthest.

“No matter what stage of life you are in, it is important to know your financial health. This is not something you do just around income tax time but throughout the year. It’s good to check in at least monthly or, as we do, daily. The same as any successful business must know their income and liabilities, so should you.”

— Billy and Akaisha Kaderli

You can find more info on Billy and Akaisha’s budgeting ideas on their website.

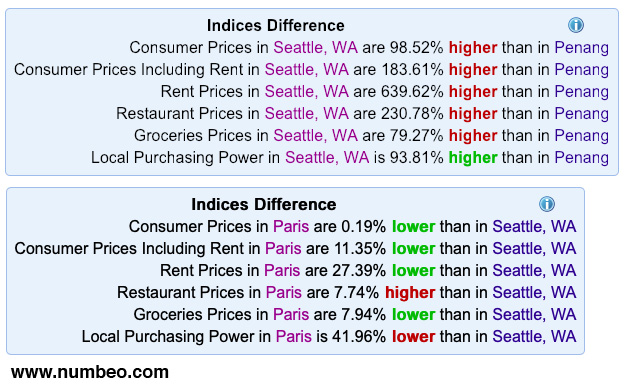

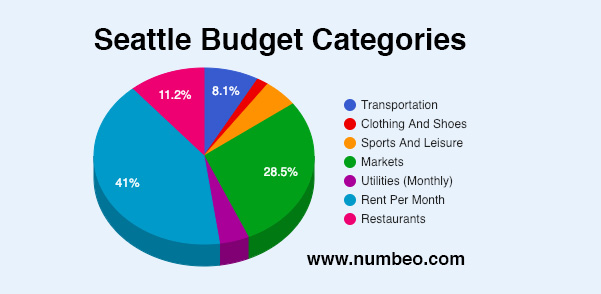

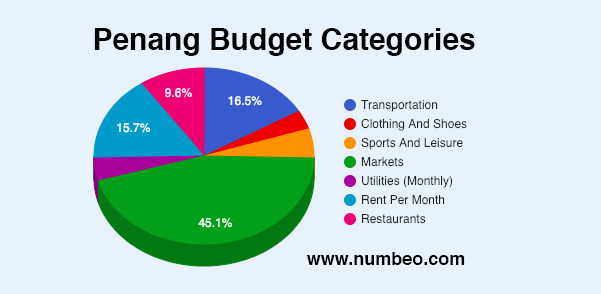

How much does milk cost in Penang?

Even though we are still new to being full-time travelers, it’s clear that our variable expenses are extremely location dependent. For instance, in 2018 using Seattle as our baseline, I looked at the relative cost of living in a long list of locations on Numbeo’s website. The Numbeo tool helped us choose the locations we now plan to live in over the next year. We were interested in Southeast Asia, which proved to be a great region for us to start out in. I could tell we would do well reducing our variable expenses in Southeast Asia compared to what we were spending in Seattle. For example, Seattle’s cost of living is nearly twice as high as that of Penang in Malaysia. Another example location is Paris, the most expensive place we plan to live in this year, with a cost of living that’s 1.4x more expensive than Seattle.

Check out the Numbeo graphics below. The two Indices Difference graphics compare the costs of Seattle to Penang, and the costs of Paris to Seattle. I have also included two Budget Categories pie charts for Seattle and Penang. The differences are clear – and they are not a problem. We can balance Penang with Paris, spending time in low cost and high cost locations.

Where should we draw the line?

Digging deeper, I want to know more about our high fixed expenses because they feel really high right now. For instance, is it reasonable to have fixed expenses representing as much as 60% of our total budget or is that way too high? Is this just part of our “step down” into a new lifestyle and an obvious area for more cutting? Or does that number fit our new lifestyle, and if so, will it start to look more normal over time? It’s hard to imagine numbers that high ever seeming reasonable, but we’ll know more in a few months.

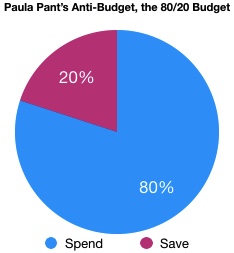

The Anti-Budget

As a general rule, I don’t like nitpicking at individual budget items. I prefer to focus on saving and investing rather than spending, and I’ve found a great term for this on Paula Pant’s “Afford Anything” blog. Using Paula’s terminology, I’m more of an “anti-budget” kind of person. The anti-budget means you target your savings first and then you can spend what’s leftover after that. Simple! And it also offers the fabulous idea of saving at least 20%. Amen! Exactly what we were been doing throughout our careers. For more info on the anti-budget, check out Paula’s post on Afford Anything.

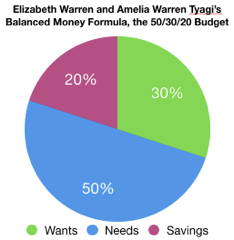

The Balanced Money Formula

Admittedly, I do enjoy putting a more detailed budget together. As I was looking for other examples of budget ratio guidelines, I came across the Balanced Money Formula, or the 50/30/20 budget, outlined in Elizabeth Warren and Amelia Warren Tyagi’s book, “All Your Worth: The Ultimate Lifetime Money Plan.” This budget also supports the idea of saving 20%. And it divides spending between “needs” and “wants.” For more information on the Warrens’ Balanced Money Formula check out J.D. Roth’s Get Rich Slowly book review.

Find your own way

I think the Balanced Money Formula makes sense, but I still prefer Paula Pant’s idea of focusing on your savings first and making that your top priority. This type of thinking was incredibly important for us as a step ladder to higher and higher savings over the last few years. By 2017 I had set our own budgeting goals to make sure we saved at least 50% first, spent about 30% on our needs, and lastly spent only about 20% on our other wants.

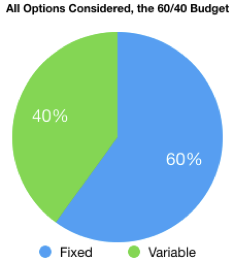

Today things are different. Since we left our careers we are no longer in our accumulation phase and we aren’t as focused on what we are saving anymore. So I removed the savings category from our budget for now. Moving forward, I have simplified the budget categories and rejiggered the percents to get a 60/40 budget with 60% allocated for the necessities we are committed to (our fixed expenses), and 40% allocated for the other things we want to pay for (our variable expenses). That also includes a 26% housing target within the fixed expenses, an idea I learned from Billy and Akaisha Kaderli’s years of traveling the world after early retirement. Bingo! That’s the formula I used to build the All Options Considered 60/40 Fixed/Variable Budget. You have to give yourself a target to strive for right?

The conclusion – for now

For now I’m very comfortable with the All Options Considered 60/40 Fixed/Variable Budget. I’m also comfortable knowing our main goal for this first year is to practice a new kind of mindfulness for how we spend our money. I know we are early in the process of creating new spending habits for ourselves in this nomadic lifestyle. To be generous and cautious, we are giving ourselves a total budget for traveling in 2019 that is equal to the average of what we were living on in Seattle over 2017 and 2018. I consider that more than reasonable as a starting point because we worked so hard in 2017 and 2018 to trim our spending way back as we prepared for 2019. And if you are wondering what our Safe Withdrawal Rate is, I will definitely cover that in a later post!

Of course I’m hoping we will spend far less in 2019 as nomads than we did as frugal travel planners while still living in Seattle. And once we have lived with this budget long enough for some of our placeholder numbers to become reality, I will follow up with another post about our actual fixed and variable expenses in 2019. It will be interesting to see what we decide to categorize as needs or wants.

I know a lot of people like to play Candy Crush, though I am not one of them. When I’m working on budgets and finances, Ali loves to say that I’m playing my game, Money Crush. I love my game! I’m really looking forward to tackling higher and higher levels of Money Crush and seeing how it all shakes out over 2019 and beyond!

[…] a previous Money Crush post, “The AOC Budget and Our Daily Living Expenses” I wrote about building our budget for our new life on the road and very importantly, […]

LikeLike

[…] Since these types of care are so much more affordable in other countries like Thailand and Mexico, the idea of medical tourism is attractive. And paying out of pocket does not sound like a budget breaker. We have done enough research on the options out there, and we know our eyes and teeth well enough to plan ahead. That’s one of the reasons our medical budget is set at around 15% of our total budget for 2019. For more detail see our post on “The AOC Budget and Our Daily Living Expenses.” […]

LikeLike