And another question, is all this I-bond enthusiasm FOMO or mo money?

We’ve all been hearing lots about inflation-linked savings bonds (I-bonds) lately. And lots of you have been asking us if we’ve jumped on the current I-bond train ourselves. Before we answer that question we’ll dig in and research what I-bonds are and how they work.

We are not certified financial professionals. For more information read our Disclaimer.

Learning about I-bonds

Investopedia is one of our favorite online libraries for personal finance research so here’s their definition of I-bonds: “Series I bonds are non-marketable bonds that are part of the US Treasury savings bond program designed to offer low-risk investments. Their non-marketable feature means they cannot be bought or sold in the secondary markets. The two types of interest that a Series I bond earns are an interest rate that is fixed for the life of the bond and an inflation rate that is adjusted each May and November based on changes in the non-seasonally adjusted consumer price index for all urban consumers (CPI-U).”

Wow, that’s a mouth full.

I-bonds are very trendy right now in this crazy high inflationary period, but they’re not new and they’re not just a trend. They’re a low risk savings and investing option that’s been around since 1998, designed specifically as protection from inflation. I-bonds have a minimum holding period of one year and a full maturation period of 30 years. The real rate of interest for I-bonds is a composite of a fixed rate and an inflation rate, and the Bureau of the Fiscal Service announces the rates for I-bonds each May and November. The current fixed rate for I-bonds is 0%, the current semiannual inflation rate is 4.81% (half of 9.62%), and the current composite rate of 9.62% is set for May through October of 2022. Which means the guaranteed interest rate is 4.81% for 6 months. I know, confusing right?

The US government created the savings bond program in 1935 because they needed a new funding source to help fund parts of the government and they also needed to encourage people with relatively small sums available to get into the stock market since people were afraid to invest after the Great Depression. My paternal grandparents were a perfect example of this. They were afraid and in fact never invested in the stock market.

One of the challenges with I-bonds is the rate only being set for 6 month periods, unlike CD’s which currently have unimpressive low rates of around 2.25% to 2.55% for a 5 year fixed term. Another challenge is that I-bonds can stop earning interest altogether during deflation when the consumer price index decreases. Another challenge is that I-bonds can only be bought, held, and redeemed within a US Treasury savings account. You can’t just buy and sell I-bonds in your Vanguard (or Fidelity or Schwab) account.

On the plus side, because I-bonds are government savings bonds your original principal is always safe. Unlike other types of bonds that can be bought and sold on a secondary market and lose their value with interest rate volatility, I-bonds are considered rock solid safe.

The best thing about I-bonds is their amazing current rate, which is a product of this particularly crazy high inflationary period. Here’s a historical chart of I-bond interest rates so you can see the rates the government has set for them during their entire history. It’s interesting to see how the fixed rate and inflation rates have changed between the current 6 month rate all the way back to the original rate set in 1998.

Maximizing I-bonds

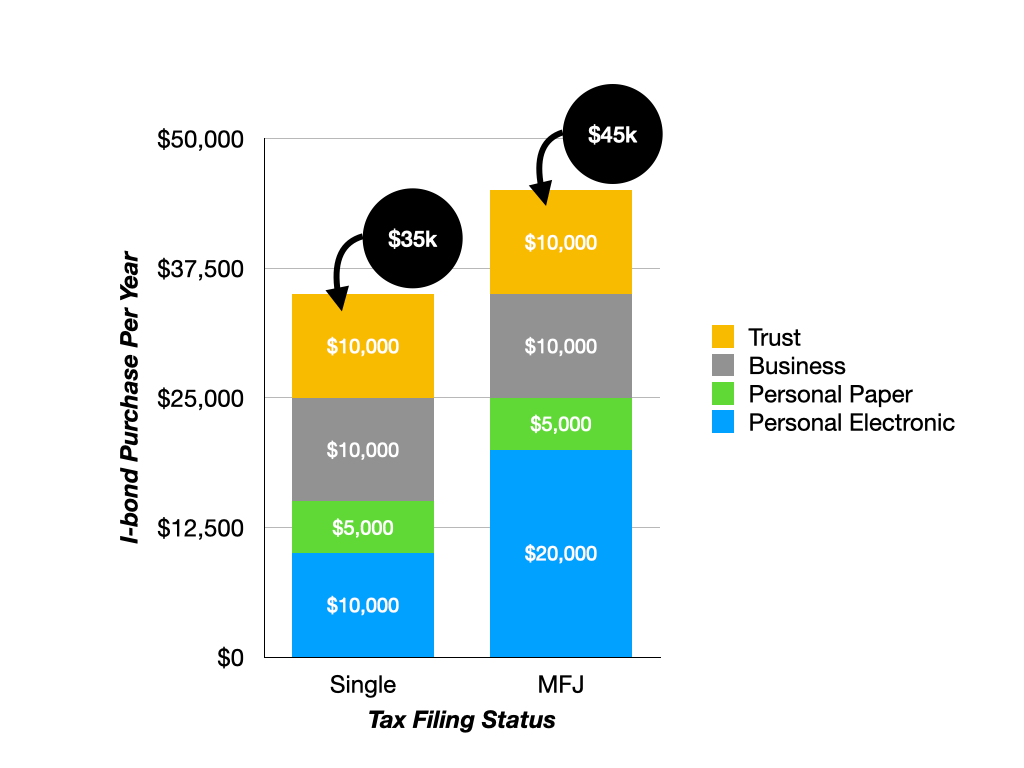

I think it’s unfortunate that you can’t buy unlimited amounts of I-bonds like you can with CD’s or other types of bonds. Being limited to $10k in electronic I-bonds and $5k in paper I-bonds per year isn’t much. But there are a couple of other ways for some people to accumulate more than the personal limit for I-bonds.

Businesses and Trusts also qualify as entities that can purchase I-bonds, which means business owners and Trust owners can create US Treasury savings accounts for those types of entities as well and purchase up to $10k each year in I-bonds. I found that interesting since we just created a new Trust ourselves to hold our property and brokerage account since we built a compound and we want to protect our housemate’s right to live there if he outlives us. The drawback would be opening a separate US Treasury savings account for each entity to hold the $10k allowance in electronic I-bonds with its own EIN number.

The chart below makes it look like we can all buy a lot of I-Bonds. But in reality, not many folks have their own business nor do they have a Trust. Most people are limited to $15k per year as a single person or $25k per year as a couple.

Good reasons to buy I-bonds

So now we know there are some good reasons to hold I-bonds as part of your portfolio, including…

- Inflation linked return

- Original capital protection

- Portfolio ballast to reduce impacts from market volatility

- Bond ladder of stable guaranteed capital and a 6 month guaranteed return

- Can use them for education

- Can give them as a gift

The most attractive thing about I-bonds is the inflation linked return rate, which is currently a 6 month rate of return of 9.62%. But we have to assume after 6 months that rate will be adjusted. Earlier this year it looked like the previous 6 month rate of 7.12% was going to drop for the May to October period, but luckily (for I-bond owners) it went up instead. One thing’s for sure – these rates are WAY better in the short term than any high yield savings account out there!

Reasons not to buy I-bonds

Even though there are amazing rates on the current series of I-bonds, there are reasons why people might not want to buy them, such as…

- Not a great emergency fund option (you can’t sell them in less than 5 years without a penalty)

- Limited annual purchase amount (only $10k in electronic I-bonds and $5k in paper I-bonds are open to everyone)

- It would take years to build up a large enough holding of I-bonds to make a BIG difference in a portfolio

- You must buy them direct from the US Treasury

How to buy I-bonds

If you do want to buy I-bonds before the current six month rate period ends… Just open a US Treasury savings account for yourself, link that to your bank account, and then you can buy electronic I-bonds in any amount from $25 to $10k.

And if you want to buy paper I-bonds using your IRS tax return, you can use IRS Form 8888 to buy them in any amount from $50 to $5k. And once you receive your paper I-bonds in the mail you can convert them to electronic I-bonds and hold them in a US Treasury savings account instead of physically keeping them in paper.

Time for the spreadsheet!

We’ve been hearing from other people that it can be hard to figure out what kind of impact I-bonds would actually have on a portfolio. Lucky for you we’ve been using our money crush spreadsheet to test how $10k in I-bonds would affect a range of portfolio sizes and we have some numbers to share.

Let’s say you have a $1M portfolio, and like us, you’re targeting a nominal return of 6% annually. If you buy $10k in electronic I-bonds within the current period at the 9.62% rate that means 1% of your total portfolio is in I-bonds, and the 9.62% rate is equivalent to a 4.81% annualized return on your original $10k. The total nominal annualized return from those I-bonds is equivalent to 0.0481% of your 6% target return for your whole portfolio, and the 6 month return on your $10k of I-bonds is equivalent to $481 at this time.

But what if you bought your $10k in I-bonds during the previous 6 month period (between November 2021 and April 2022) when the rate was 7.12%? The return from those I-bonds is equivalent to $356 for 6 months, and when you add those two return rates up you would have gained a total of $837 on your $10k, once you hit the 1 year minimum holding period. But then if you sell your I-bonds in less than 5 years you’ll lose the last 3 months of interest (grrr).

The next test we wanted to run was to calculate earnings on $10k of I-bonds if you buy them this year and hold them for a full 5 years so there’s no penalty for selling. But unfortunately that’s really impossible to do since we can’t predict future interest rates for I-bonds.

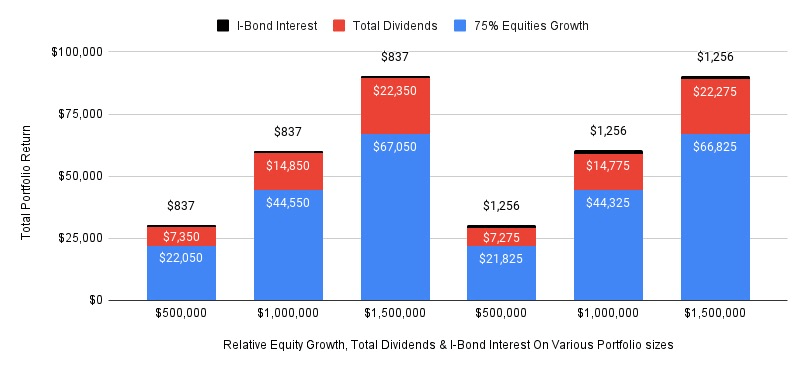

We also wanted to compare the kind of return you could get from holding I-bonds to what you would hope to earn from $10k in a US broad market index fund ETF within a $1M portfolio. It’s definitely possible for a $1M portfolio to generate a total return of $60k in a year from an average nominal 6% return on equities, with a 75% equites allocation, while also earning 1.5% in dividends. In this example the interest from I-bonds represents 1.4% of the $60k total return, which is a bit higher than its original 1% weight in a $1M portfolio.

We ran these types of tests using 3 different portfolio sizes including $500k, $1M, and $1.5M. The screenshot below from our spreadsheet shows the relative weighted impact of holding I-bonds within each of the 3 portfolio sizes. The clearest message in the spreadsheet was that the impact of earning $837 in interest from I-bonds decreases as your portfolio size increases.

Personally I think spreadsheets are the best! But we are very visual people and we also like to use all sorts of charts and images to help us communicate our thoughts, even when it’s just me and Ali talking and making plans together.

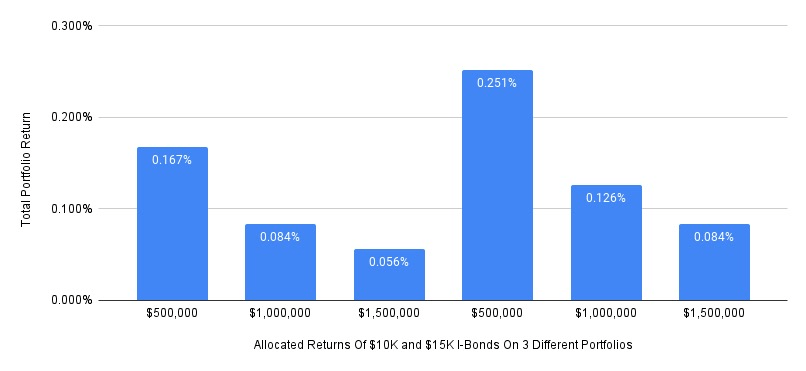

The chart below from our spreadsheet shows the relative weight of $10k and $15k in I-bonds on the same 3 portfolio sizes. The clearest message in the chart below was that the little red line for I-bonds is really hard to see, which makes sense as we dig deeper.

If you buy the $10k maximum purchase quantity for electronic I-bonds, that growth impacts 1% of a $1M portfolio. And if you buy the $15k combined maximum of electronic I-bonds plus paper I-bonds, that growth impacts 1.5% of a $1M portfolio. The more I-bonds you buy the bigger the impact.

But what if you have a $2M portfolio, or larger?

In the next chart you can see the projected returns from the 75/25 allocated return starting with the $10k in I-bonds, then 1.5% dividends, and finally equity growth on a $1M portfolio.

The impact of I-bond returns on your portfolio’s total annual return really starts to come into focus when compared to the other streams of income generated from different investments in a portfolio that’s producing a 6% nominal allocated return and 1.5% in dividends.

It always helps to convert return rates into dollars to understand the impact of different investment strategies on a total portfolio!

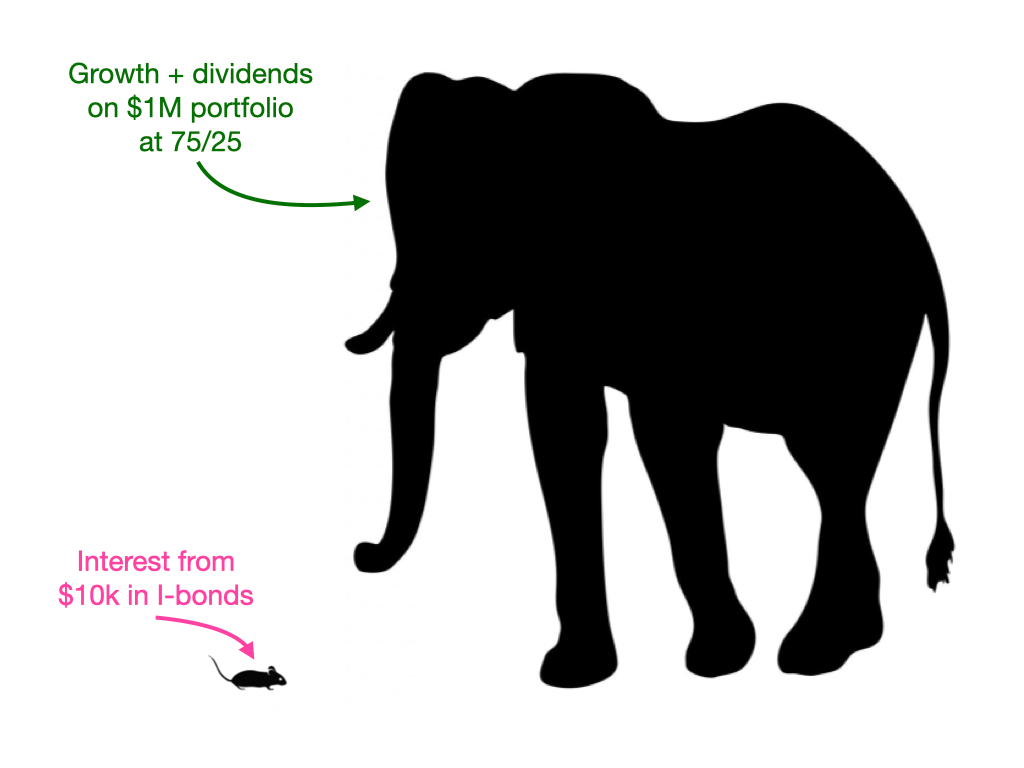

The chart below makes it clear that the overall advantage of I-bonds decreases as the size of your portfolio increases. The smaller your total portfolio is, the larger the impact from $10k in I-bonds on your total portfolio. Conversely, the larger your portfolio is, the smaller the impact from I-bonds on your total portfolio.

The chart above shows the diminishing impact of $10k and $15k I-bond holdings on the same 3 different portfolio sizes. In other words, that amazing 9.62% return on $10k turns into an allocated 0.084% on a $1M portfolio. That return rate is like comparing a mouse to an elephant.

The pros & cons of I-bonds

After doing some research and testing some numbers the I-bond picture becomes pretty clear, and understanding the pros and cons of I-bonds (or anything in personal finance) helps us make informed decisions. With every investment type there are pros and cons to consider, and we are all unique money managers so the impact from holding I-bonds would be unique for each of us. You just have to know your own goals and decide if I-bonds are something you want or need in your own portfolio. We’ve summarized the pros and cons as we see them from holding I-bonds below.

Pros

- Low risk

- Inflation protected

- Earns compound interest rather than simple interest

- Interest is tax free if used to pay college tuition

- Earnings are exempt from state tax

- Original investment can’t be lost

- Earnings can be liquid after 1 year

- No penalty if held for at least 5 years

- Can be given as a gift

Cons

- 1 year minimum term

- They’re conservative savings bonds

- Individuals are limited to $15k per year

- If sold before 5 years you lose the last 3 months of interest

- Interest rate is only set for 6 months

- When inflation is low I-bond rates are low

- Combined interest rate can drop to 0% with low inflation

- Only available through the US Treasury

- Gifts count towards the recipient’s limit

The design of the US government savings bond programs allows for rates to be set for 6 months so they can be changed regularly as inflation changes, and the purchase limits can be changed at any time. As an example, the US Treasury changed the annual purchase limits in 2007 from a $30k purchase limit down to only $5k in order to “refocus the savings bond program on its original purpose of making these non-marketable Treasury securities available to individuals with relatively small sums to invest.”

Should YOU hold I-bonds?

Only YOU can answer that question. Remind yourself of what kind of investor you are now and what kind of investor you want to be. Think about what you need from your cash savings and how accessible you need that cash to be. Think about how much effort you want to put into the buying process, how much time you want to spend tracking interest rates, and how long you would intend to leave your I-bonds in the US Treasury before you sell (1 year, 5 years, 30 years?). And of course think about whether you would buy them as gifts for others, for yourself, through your business, or through an estate Trust.

For some people I-bonds are well worth the effort because 9.62% is an awesome rate, regardless of whether it’s only for 6 months or lasts longer. We certainly have talked to lots and lots of people who have bought I-bonds this year and if that’s you too, more power to ya!

Personal finance is personal so do your research and then decide what’s best for you and YOUR portfolio!

Back to the original question – what about us?

People have been reaching out to us to talk about I-bonds and ask if we have purchased any ourselves. The short answer is no.

If this was 2018, which was the down market year we retired in and I-bonds had similarly high rates back then as they do now — we would have considered buying I-bonds instead of CD’s. At that time we were looking for higher interest savings vehicles to hold some of our cash we needed for our first few years of early retirement. Since it was a down market year we were a bit nervous about retiring early, and finding higher yields for our cash helped us with that nervousness. For the period from May 2018 to October 2018 the 6 month composite rate for I-bonds was only 2.32%! During the next 6 month period from November 2018 to April 2019 the rate was 2.83%, and then it dipped back down to 1.90% for the following 6 months. Back then we found 2 year fixed rate CD’s earning 2.75%, which we bought within our brokerage account and held there for 2 years and that worked great for us at the time.

Not that it’s 2022, we are different investors today. In this moment the only way I think we’d be interested in buying I-bonds is if we could buy them in any amount we wanted. For example, it would be appealing if we could put something like $200k in I-bonds right now.

In our Personal Money Statement (PMS) we wrote that we’ll strive to achieve a nominal 6% return annually using ETF’s. We won’t chase volatile home run style returns the way people chase individual stocks and IPO’s, and we won’t chase interest rates as a reaction to market volatility. At this point in our personal finance journey we have a simplified portfolio with only 5 ETF funds across all of our accounts. We don’t have any money squirreled away in smaller amounts like $10k or even $20k.

There’s also a general style for investing in the government savings bond program that doesn’t feel like it fits with our personal investing strategy. We know the government savings bond program fit perfectly with Ali’s grandma’s investing strategy. As a depression era kid grandma Ali’s grandma was always looking for financial safety and government savings bonds were the perfect carrot.

But I can say if we did buy I-bonds with some of our cash savings this year, our minimum holding period would be 15 months in order to get at least a full year of return after losing 3 months of interest. And we hit our tax target this year (hooray) so there was no refund to use for paper I-bonds. As for our new Trust, buying I-bonds through that entity doesn’t appeal to us. The idea of opening a couple of US Treasury savings accounts in order to buy $35K in I-bonds (that’s our max since we don’t own a business) sounds like more hassle than it’s worth.

That’s it for now

For us there isn’t enough incentive to buy I-bonds given the total impact on our portfolio, the effort it would take, and the lack of liquidity that would mean for that cash. We want the option for 100% liquidity in the cash portion of our portfolio, and we want all our investments in one institution for ease of access. We’re not interested in chasing interest rates like the latest shiny object, as one of our CFP buddies said when we were chatting the other day. We’re keeping our focus on understanding how our total portfolio is impacted by any money move we make, and I-bonds just aren’t available in large enough amounts to make us want to jump through hoops to get them.

And to answer the other question everyone is asking us right now — aren’t we freaking out about how poorly the market is doing this year??? No we are not freaking out. We also aren’t watching the market every day. We do not regret deciding to shift our allocation up to 80/20 this year from our original 75/25 ratio when we retired because that still feels like the right move for us.

If we could do anything right now we’d buy more equities this year but we don’t have any extra cash available since we just bought an Airstream trailer (and no we definitely do not regret that decision!). We are very happy that we shifted some funds out of our cash holdings back at the end of 2020 into personal real estate. At this point that investment is up 30%. It’s a balance and having a bit of diversity is what will smooth out this crazy ride.

As I write this post the S&P 500 is down around -16% year to date, and that’s painful. But that doesn’t change the fact that the overall market trend is still up. The S&P 500 has gone up an average of 11.46% per year (including the start of 2022) since January of 2019 when we started our first full year of retirement. We’re aiming for an average annual total growth of 6% over the long term, so tracking only the long term market trends helps us keep our focus on the big picture. And for us that means the only metric we need to know is that our portfolio is up a cumulative allocated rate of 44.11% today from where it was in January of 2019, and that’s including the current market drop.

We aren’t trying to predict where the market will land by the end of this week or this year, and we aren’t in a place of fear. We’ll continue chasing an overall portfolio growth rate of 6% on average over the years, knowing some years will be down and other years will be up. Our portfolio is doing what it’s supposed to do, despite the market correction this year. We don’t want to increase our bond holdings and since life is so unpredictable we especially don’t want to lock any cash away where it’s not liquid and accessible in an emergency!

Do I have any I-bond FOMO myself? Maybe a little, but really what I have is I-bond curiosity!

Hi Allison,

As always your article is very well articulated along with nice pictures/graphs, but is there a way to see the snip of the spreadsheet in a larger font or via a link on Google Docs perhaps? I don’t know whether I should blame my eyesight in this case or if it was intentional, but I wanted to look at the Excel picture…so this particular picture isn’t “pretty” for me, LOL.

Overall, you write a great educational content and I thank you for that.

LikeLiked by 1 person

The spreadsheet screenshot is a bit tough to see since it’s so wide. But since you asked nicely we’ve added a PDF you can open and zoom in on. Enjoy! 🙂

LikeLiked by 1 person

Fun analysis. It makes sense to not complicate your portfolio just for one time 10K purchase. In my case, I have been buying I-bonds regularly, so it was a no-brainer to buy them again in 2022. They add up after a few years. For example, a couple buying 25,000 per year can have 250,000 in 10 years. I view them as inflation adjusted cash/bond allocation portion of the portfolio.

LikeLiked by 1 person

I totally agree that buying I-bonds can be a long term strategy if buying over time and doing what it takes to get that $25K a year. And if its something you start early as part of your plan, excellent. I do also like the compounded interest and that its protected from any loss do to market fluctuations. And I still feel like it would take some time to build up a big enough stash to make a dent fast enough.

LikeLike

Oh definitely takes time to build a stash of inflation protected portfolio. One can supplement low 10K limit of I-bonds with TIPS now that their real yields are rising. Soon they can be as attractive as I-Bonds and they do not have that silly 10K limit.

LikeLiked by 1 person

I bought I-bonds! I have a pretty specific use case: I’ve been saving money to take a year off, so the bond purchase has been part of that bigger picture.

Of the money I am willing/planning to spend over the next year:

– about 43% is in cash/in my checking & saving accounts

– about 43% is in the stock market

– the final 12% is in an I-bond.

About the I-bond: I won’t get the full year of interest, because I fully plan to cash it on its 1st birthday, but that’ll be a LOT more interest than I earned on the 43% sitting in the bank.

About the stock market: yep, it’s been painful to watch my Fun Money shrivel a bit. Right now I’m just letting it ride, and hope it’s back up by December/Jan when I’m planning to tap it. If it comes back up to a specific number before then, I’ll cash it out early, and if it’s still down I’ll just tap it when I need it and it will probably mean I have to get back to work sooner. I’m so very grateful to have this learning experience well before I actually retire!

I have one more I-bond and some other money market funds that are held aside to live on if it takes a while to get a job.

LikeLiked by 1 person

[…] in reaction to this wacky year of market craziness, and the answer is no. We aren’t buying I-bonds or anything else that’s trendy. We have no intention of dropping any of our existing funds or […]

LikeLike