August was a big month for Congress and Biden when it comes to passing significant bills. The one we were watching closely was finally signed into law as the Inflation Reduction Act, also known as the “IRA,” which is a little confusing since that acronym is already taken by our retirement accounts. Of course Biden had more ambitious plans for the bill for sure, we’re just relieved that congress could agree to sign this version of Biden’s original Build Back Better Plan. And spoiler alert, we’re very excited about the Affordable Care Act (ACA) related changes in this new law!

We are not certified financial professionals. For more information please read our Disclaimer.

What We’re Hearing on the Street

Although this new IRA law’s name suggests it will reduce inflation, that’s not really what it’s about. The main focus areas of the new IRA law are increasing corporate taxes, reducing prescription drug costs, and the most significant investments and policy changes the US has made for climate change so far. Yahoo!

Below is a Forbes list of highlights for the new law:

- Creation of a 15% corporate minimum tax rate: Corporations with at least $1 billion in income will have a new tax rate of 15%. Taxes on individuals and households won’t be increased. Stock buybacks by corporations will face a 1% excise tax.

- Prescription drug price reform: One of the most significant provisions of the Inflation Reduction Act will allow Medicare to negotiate the price of certain prescription drugs, bringing down the price beneficiaries will pay for their medications. Medicare recipients will have a $2,000 cap on annual out-of-pocket prescription drug costs, starting in 2025.

- IRS tax enforcement: The IRS has been sounding the alarm for years about being underfunded and being unable to deliver on its duties. The bill invests $80 billion in the nation’s tax agency over the next 10 years.

- Affordable Care Act (ACA) subsidy extension: Currently, medical insurance premiums under the ACA are subsidized by the federal government to lower premiums. These subsidies, which were scheduled to expire at the end of this year, will be extended through 2025. Approximately 3 million Americans could lose their health insurance if these subsidies weren’t extended, according to the U.S. Department of Health and Human Services.

- Energy security and climate change investments: The bill includes numerous investments in climate protection, including tax credits for households to offset energy costs, investments in clean energy production and tax credits aimed at reducing carbon emissions.

But what about inflation? How come there’s no mention of inflation in that list of highlights for the Inflation Reduction Act? According to estimates from the Penn Wharton Budget Model, “The Act would very slightly increase inflation until 2024 and decrease inflation thereafter. These point estimates are statistically indistinguishable from zero, thereby indicating low confidence that the legislation will have any impact on inflation.” And the Congressional Budget Office (CBO) agrees the new law’s effect on inflation will be negligible at best. We would have loved some actual inflation relief in the inflation recovery law!

Another bonus of the new IRA law is that it should reduce the national budget by 4% over the next 10 years. Closing a few tax loopholes used by the wealthy by adding a new 15% corporate minimum tax and a 1% fee on stock buybacks will create new corporate tax revenue streams that will contribute to a nice reduction in national spending. That 4% reduction in spending may not sound like much but every bit helps.

And however much the new law falls short on fighting inflation it really is a breakthrough regarding human-caused climate change policy. The new law brings real incentives on the corporate side to encourage renewable energy production, and on the individual side the law offers new tax credits and rebates for greener energy upgrades. It’s a relief to have politicians in office who are willing to pass climate change laws for things that could make a real difference, like cutting greenhouse gas emissions by at least 50% from 2005 levels by 2030. Biden may seem boring after the massive drama caused by the previous guy but we’re ok with that, especially since Biden is getting beneficial things done.

And here’s what we’re most excited about — the new IRA law lowers health care costs! We were thrilled back in 2021 when Biden’s American Rescue Plan Act (ARPA) expanded ACA subsidies above 400% of the Federal Poverty Level (FPL) and also increased subsidies for people with incomes between 100% and 400% FPL. But those improvements were only set to last for two years, 2021 and 2022. We’ve been anxiously waiting to see what’s next, and the wait is over!

We almost never have a conversation about money and retirement with folks without spending a lot of time talking about the costs of health care in this country. Anyone who tracks how our health care costs compare to any other country will recognize the changes in this law as very good news. The new IRA law will save the average ACA marketplace enrollee $800 annually. It will also empower Medicare to negotiate with drug companies and lower costs on prescription drugs over the next decade. Drug companies will also be required to issue rebates for drug price increases that are higher than inflation. All good things!

What We’re Hearing from the Health Care Industry

In a recent article from the Kaiser Family Foundation (KFF), the big highlight of the IRA law is reduced prescription drug costs for folks on Medicare. The changes reducing Medicare drug costs are huge for people age 65 or older on reduced incomes with expensive health care costs to cover. But since we’re not yet old enough for Medicare we’re even more excited about extended subsidies for ACA coverage, and the fact that this IRA law essentially removes the ACA cliff for another 3 years.

The KFF article noted 5 specific benefits relating to the ACA:

- IRA will prevent shocking out-of-pocket premium increases. In some 33 states, there could have been premium increases as high as 53% with the return of the subsidy cliff for folks making over 400% FPL.

- IRA will block the “Double Whammy” we were dreading in 2023. Premium rates were due to rise on average 10% with the range being between 5%-14%. By delaying the return of the subsidy cliff by 3 years, participants will avoid the double shock of the return of the cliff AND an annual premium increase.

- IRA was passed just in time! The timing of passing IRA was critical as insurances were in the process of updating their premiums. So with its passage, the IRA will reduce confusion for providers and participants as open enrollment approaches in November.

- IRA and the Covid pandemic. As we come out of the current Covid health emergency, folks who have been on Medicaid may become disenrolled upon returning to full time employment. Since IRA provides a continuation of ARPA subsidy levels, more folks can find low or zero cost coverage on the ACA.

- Will IRA boost ACA enrollment numbers? The cost to the federal government to extend ACA subsidies is estimated at about $25 billion a year with IRA. However, reduced premiums make it more likely that people will be able to afford healthcare on the ACA and enrollment will increase.

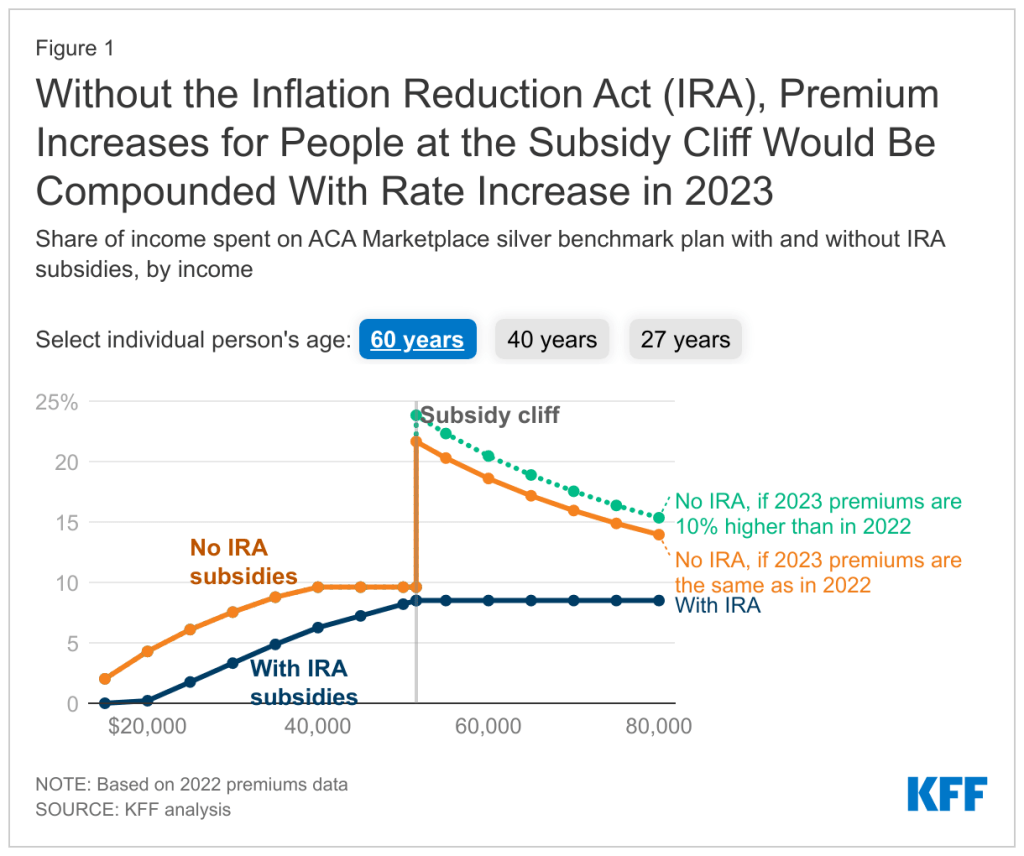

The following chart from KFF shows the original rate percentages for premiums for a single 60 year old person. Note the increased premium cliff for this example individual. With the extension of the enhanced subsidy provision of ARPA in the new IRA law, the maximum premium level is around 8.5% of your income.

What We’re Saying Here at AOC

The part of the IRA law we’re most excited about is the extension of reduced premiums for the ACA because that impacts us directly starting in January. For us specifically that means if our income is over 400% FPL this year, our premium could have been as high as 24% of our income next year. That would have been a big financial strain and would have renewed my anxiety about having enough money for a long retirement. But with the IRA law in place our premiums will max out at 8.5% of our income for the next 3 years and that’s much better than the alternative if ARPA’s ACA improvements had been allowed to sunset at the end of this year.

I’m relieved and thrilled to know what the ACA is going to look like for another 3 years. We have been hoping that ARPA’s expanded ACA subsidies would be made permanent this year, but at least we get a few more years of enhanced subsidies. This is particularly helpful right now as we wait for the market and economy to recover a bit as we are still in that early retirement window when sequence of return risk (SORR) is on our minds.

And it’s interesting to see IRA’s ACA changes coinciding with tax changes. We are assuming that on January 1, 2026, the tax brackets will jump back up from 12% to 15%, and from 22% to 25%, and from 24% to 28%, etc. We shall see if our crystal ball has any real seeing power!

We are willing to allow our retirement income to rise above the 400% FPL in order to make Roth conversions and keep our taxes lower after required minimum distributions (RMD’s) start. So what does all of this mean to us? What would the likely scenarios look like?

We won’t know our total dividend income until mid December, but assuming we find our total income for the year above the 400% FPL that 8.5% flat rate is an important part of staying on budget, which is why we pay so much attention to the ACA cliff. We’d rather not have to increase our budget in 2023 just to pay for more expensive health care premiums. We don’t love the 8.5% flat rate personally but having a consistent number for anyone over 400% FPL is a big improvement. Just imagine a family of 2 working hard to make ends meet with an income of only $73,241, just $1 above the 400% FPL, having to cope with an increase in the cost of subsidies. If we use the estimates from KFF that means that family of 2 would be dealing with an average estimated increase of 10%, or worse as much as 14%. If that couple was paying $144/month for a bronze plan like we were at the start of last year, and that number jumped to $1,440/per month or even more that would really mess with their bottom line!

Since the IRA law will delay the return of the premium cliff for another 3 years we can move forward with our plans. Knowing we have a 3 year crystal ball telling us where our health care premium costs will land we can start updating our money goals for the next 3 years.

Now we can…

- More accurately estimate our ACA premiums at 8.5% of our income

- Plan for our estimated tax payments next year

- Update our plan for Roth conversions in December

- Feel much more confident regarding our 2023 budget

Health Insurance is Wealth Insurance!!

According to our personal finance strategy health insurance is wealth insurance, which means managing our health care costs is critical to our financial wellbeing. One of the biggest reasons is the predictably of costs. We still aren’t comfortable with the overall cost of health care in the US but having health insurance and pooling our risk through an insurance product, will help us keep health care costs lower.

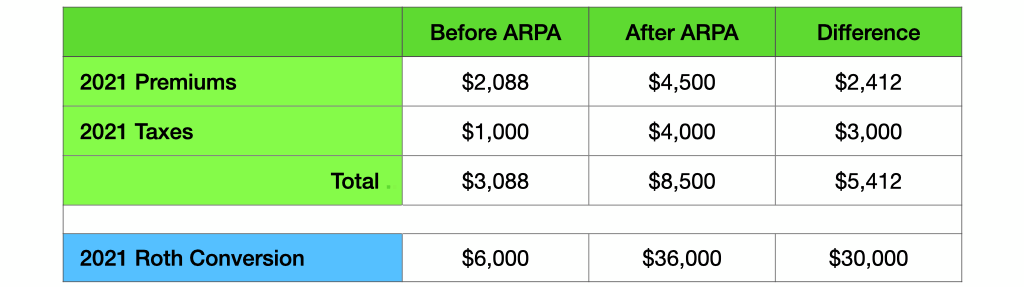

Case in point. With the passing of ARPA in mid 2021, we chose to increase our Roth conversions for last year as the ACA cliff was no longer in place. We originally chose to go from paying only $144/month in health care premiums along with only a $6,000 Roth conversion, but our plans changed after ARPA was passed and our premiums dropped to zero. At that point we chose to pay $375/month in premiums so we could make a $36,000 Roth conversion. That choice also increased our federal taxes from less than $1,000 in 2021 to $4,500 for the year as we had some subsidies we had to pay back at tax time due to our change in strategy mid year.

Why did that make sense to us? Being willing to pay more in health care premiums and front loading our taxes allowed us to shift more of Ali’s large retirement IRA account balance over to her Roth all while staying within the 12% tax bracket. That should help keep us out of a much higher tax bracket in the future. Now that the IRA law has been signed that means the current lower tax brackets are due to expire and revert back to previous higher levels after 2025, and the enhanced ACA subsidies will also expire at the same time. Interesting…

As shown in the table below, with no ARPA in place we had managed to keep our taxable income including a small Roth conversion below the 400% FPL so we could avoid the ACA cliff. By doing that, we had very low health care premiums and taxes in 2021. But that strategy also meant our Roth conversion was very low. Then when ARPA was passed we shifted gears and upped our Roth conversion, along with our taxes and ACA premiums. Why? Because our long term tax savings from avoiding high RMD’s in the future far outweighs the extra $5,412 we paid in taxes and premiums last year.

By choosing to pay a bit more in ACA premiums at 8.5% of our income and 4 times our original income tax target last year, we were able to make a Roth conversion that was 6 times larger than our original target. For us, it was worth filling up our 12% tax bracket to move over so much more to Ali’s Roth. We’ll keep sharpening our pencils, updating our withdrawal strategy, and keep making progress on our goal to make Roth conversions in order to take advantage of the enhanced subsidy extension over the next 3 years.

One last note on our current health care plan since we’re living full time in the US… As most of our friends and family know, I had to have rotator cuff repair surgery back in mid June. Before the surgery I tried to do as much research as possible to understand how much the whole surgery and recovery were going to cost. We keep a chunk of money set aside to cover our out-of-pocket costs each year but I was going to sleep a lot better if I knew what it was going to cost up front. As my surgery date got closer, I still didn’t have enough info to understand our share of the costs but it was clear we’d max out my $7,000 individual deductible. We each have a $7,000 individual deduction and a total family deductible of $14,000. That is a lot of money, but we chose our bronze level plan with its high deductible partly so we could have access to HSA accounts as well and there was only one plan available to us with an HSA.

Getting new HSA accounts in retirement allowed us to tap into our IRA’s and make a one time qualified HSA funding distribution (QHFD) for each of us. When it’s time to contribute to the HSA’s with money from our brokerage account we’ll be able to take tax deductions for those contributions. Between our two HSA accounts funded by QHFD’s over the last two years along with my catch up contributions, we have the option of tax-free withdrawals from our HSA accounts to help pay our share of costs. And our costs are still climbing since I’m now paying for physical therapy twice a week. This has been an unusually expensive year for us medically since I had surgery and Ali needed some expensive immunotherapy treatments for her respiratory issues as well. Thank goodness this kind of “big spend on health care year” isn’t typical for us.

As we carved out money for my surgery costs I wanted to know how having insurance would help. The table below includes a few of the bills we’ve gotten for my surgery so far. Note how much money was billed for each of the providers listed, and then the contracted price allowed in our ACA insurance plan. Finally and best of all, note how much money our insurance saved us. It really sucks to see this discrepancy knowing the kinds of issues it can create for people. We’re really glad we have insurance!

It’s amazing how far apart the original charges are from what the insurance company would allow. And it’s great to see that our existing bronze level plan means the providers must accept these lower contracted prices for each procedure. Just looking at these 3 main provider bills that I’ve received so far it’s great to see that our ACA insurance has already saved us more than $15,000. That number shocks me even more when I remember that savings was calculated with only those main bills that were submitted to insurance for my surgery so far. I know there’s a second surgeon who assisted and a second anesthesiologist who assisted with their own charges, plus some X-rays and an MRI, the cost of the nerve block, the immobility sling I wore for six weeks, all of the doctor consultations before and after, and all of the ongoing physical therapy appointments as well. I’m still dreading seeing the grand total cost to us after we get all of the bills but knowing our insurance is doing it’s job is very reassuring.

I realize now that I’ve needed this surgery for a few years. When I had an MRI in February they identified a partial tear but by the time of surgery in June they discovered I had a full tear and it certainly wasn’t going to heal on its own. I’m grateful we have a home base now so I can do my recovery with a good team around me and insurance to keep it all from messing up our safe withdrawal plan. And I’m also grateful that we have not had to sell any equities during this down market year because all of our emergency fund categories were fully funded back in January since we moved our FU money into a “shit happens” fund, including that chunk of money we had set aside in our HSA’s and in cash to cover our out-of-pocket medical costs.

The Game of MAGI’s, IRS Income vs ACA Income

There are a lot of acronyms in personal finance and one of our favorites is MAGI. Sounds magical doesn’t it? Modified adjusted gross income, or MAGI, was a concept we used to think of as representing our taxable income only. For IRS MAGI you start with your adjusted gross income (AGI), then add a bunch of things back in like IRA contributions and student loan interest.

Now that we have an ACA marketplace insurance plan we have to use another modified adjusted gross income calculation for understanding our ACA subsidies. The ACA’s MAGI is more simple, but that only makes it more confusing since these two income related MAGI’s are not the same. The ACA also takes your adjusted gross income, but there’s a lot less to add back in to find your MAGI for the ACA. In order to calculate your MAGI for the ACA you take your adjusted gross income and add back in any…

- Non-taxable Social Security income (which we can ignore for now since we’re too young for Social Security)

- Foreign earned income and housing expenses for Americans living abroad (which we can ignore since we live in the USA, for now anyway!)

- Tax-exempt interest (which definitely applies to us)

So there you go. Your IRS MAGI and ACA MAGI are NOT the same. Understanding the difference is important for us both because we’re money nerds and because we want to keep our income within the 12% ordinary income tax bracket, and the 0% capital gains tax bracket, and ideally also below the 400% FPL in order to maximize our ACA subsidies. Those are the 3 criteria we do our best to hit in order to deploy our personal safe withdrawal strategy at the start of each year. And now, since we can’t post a Money Crush story without using our spreadsheet, bring on the spreadsheet graphics!

The table below that we use in our Money Crush spreadsheet for these types of calculations includes a variety of categories including ordinary income and Roth conversions, which are subject to ordinary income tax brackets; qualified dividends and capital gains, which are subject to more favorable long term capital gains rates; cash/cost basis; a target budget for the year; and the 400% FPL which is where the old ACA cliff used to kick in and the 8.5% flat rate still kicks in.

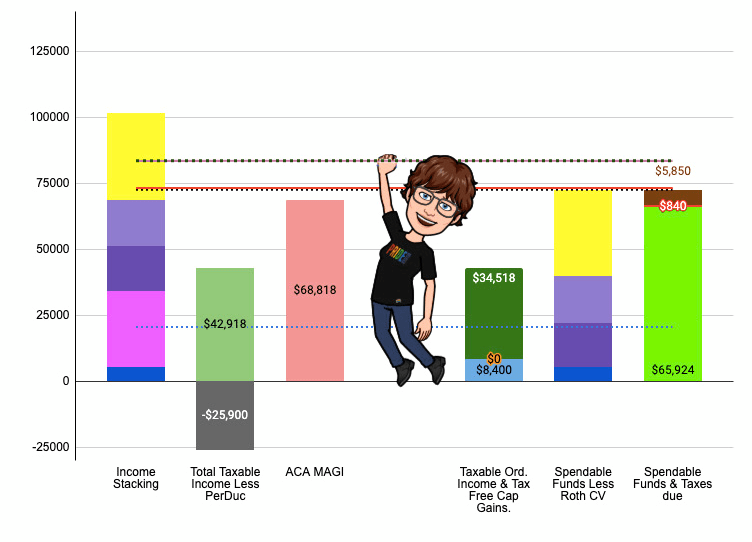

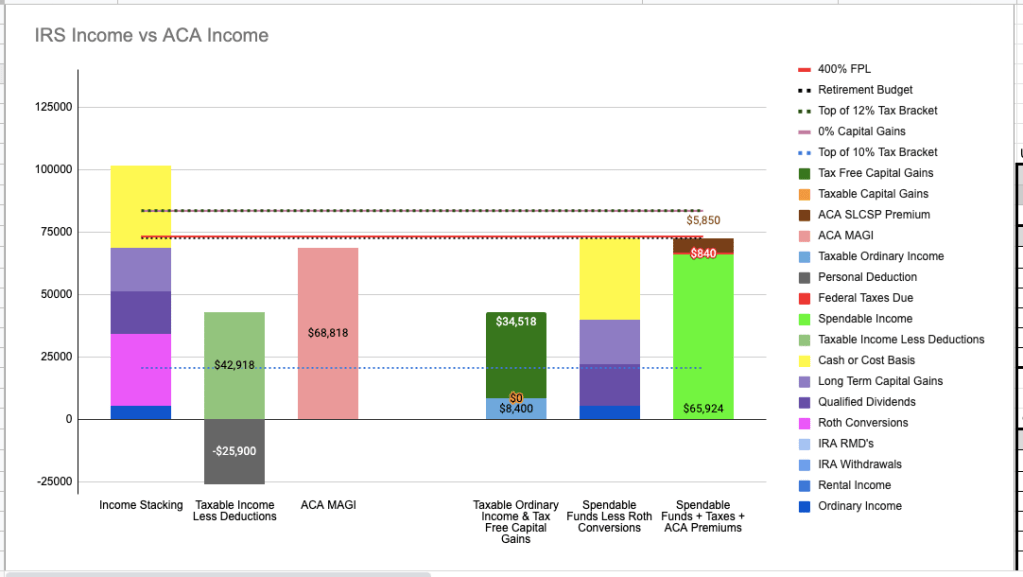

We plug numbers into the table above so we can produce charts like this one below…

On first glance this chart is confusing for everyone who isn’t in my brain with me. Here’s how we explain it to others, starting from left to right…

Income Stacking

The first column in the chart above is stacking up different kinds of income from the data table using Example 1 in our spreadsheet. The stack starts with ordinary income, then Roth conversions which will be subject to ordinary income rates, followed by long term capital gains and long term qualified dividends. And finally at the top in yellow we see a combination of cash and or cost basis from the sale of investment holdings.

Taxable Income Less Deductions

In the next column in the graph we show all taxable income after the standard deduction has been subtracted. In this example we started with about $68,000 in taxable income and after the deduction we ended up with about $43,000 in taxable income.

ACA MAGI

The third column shows how much of the original taxable income, from the first column, is considered when calculating ACA premiums. Basically, you go back to your original adjusted gross income and add back a few things like tax free interest on muni bonds and your personal standard deduction. In this example, and in lots of cases but not all of them, that takes us back to the that original $68,000 taxable income number.

Taxable Ordinary Income and Tax free Capital Gains

The 4th column is pretty simple since we have zero taxable capital gains, and then it shows how much of the ordinary income is taxable and how much is not. In this case only $8,400 in taxable ordinary income after the standard Married Filing Jointly (MFJ) deduction is taxable. The rest of the income was long term capital gains which is not taxable since it fits nicely under the qualifying threshold for 0% capital gains.

Spendable Funds Less Roth Conversions

In the 5th column we stack all of the income after the Roth conversion was made, since those funds have now been moved from an IRA account to a Roth account and are no longer available at this time but the move means those funds still count as income. This stack includes all other income for this example including cash and cost basis. As you can see, that stack runs right up to the dashed line representing the retirement budget. Perfect!

Spendable Funds + Taxes + ACA Premiums

This final column shows a cost of $5,850 for the ACA’s Second Lowest Cost Silver Plan (SLCSP), as calculated from the value of the ACA MAGI in the third column. This stack also tells us there will be $840 in federal taxes due to the IRS, as calculated from the second column showing Taxable Income Less Deductions. We don’t show state taxes here but you should add them in when doing your own personal calculation. That $840 was calculated after taking the standard deduction for MFJ and really benefited from including such a large percentage of long term capital gains that qualified for the 0% capital gains tax rate. The other number included in the calculations of this stack is $65,924, which is the actual spendable funds available to cover everything else in the annual budget.

Make sense? Putting all of these figures together in one tab of our spreadsheet helps us keep track of the two different MAGI’s when building out our goals for income, health care premiums, and Roth conversions at the start of the year when it’s time for us to take our annual withdrawal for our living expenses. This chart is complicated but it makes things easier for us when we’re calculating IRS Income and ACA Income!

Conclusion

Health insurance is wealth insurance no matter where you are in the world. In some places like the US, you will pay more for health care than in other countries. But if you live in the US what matters is staying on top of your health and of course having insurance is critical. With the passage of Biden’s Inflation Recovery Act we have 3 more years of predictable, manageable premium costs so we can make our goal of bigger Roth conversions a reality. Hooray for the new Biden IRA!

If you have more questions check out this video from KFF explaining how the new IRA law changes the ACA and Medicare…

Another amazing post! I had no idea MAGI and ACA MAGI were calculated differently.

LikeLiked by 1 person

There are lots of different MAGIs depending on what you are trying to calculate. It’s used to determine taxes, ACA premiums, if you can contribute to Trad IRAs or Roths and how much of your social security is taxed. Here is a great video that goes over the 6 most common uses for the MAGI calculation. Enjoy! https://www.youtube.com/watch?v=xE5bNtsfwOc

LikeLike

So glad that the ACA portion was included in the IRA for you two! I’m super stoked about the climate change portion 🙂

LikeLike

There were lots of things we liked in the IRA bill. Having a minimum 15% corporate tax is also good. And separate from that, we are very happy for folks who are getting a bit of a reprieve from student loans. I think we can loose site of how much of a difference in someones life a $10K or $20K loan forgiveness can make.

LikeLike

The deferral of the “cliff” will just make the chasm wider in 3 years. Your reduced anxiety should probably be greater worry. These large deficits and higher interest rates will just mean that you will pay that higher cost through the inevitable inflation that results from the bad policies implemented in the IRA. The prudent response should be to tell your audience to increase savings as costs will rise dramatically.

LikeLike

We don’t look at any kind of policies enacted by congress or presidents as good or bad per se. It’s an inefficient use of our energies. As long as we have voted, policies are what they are. We did share highlights of the law from two outside sources partly because we look at these details somewhat objectively – It’s just data at this point. This post is about the extension of enhanced ACA subsidies, and the double whammy coming in 2026 when the 2017 Tax Cuts and Jobs Act sunsets at the same time as extended ACA subsidies.

Worrying helps some people prepare but not us. The new IRA law is a “worry reduction” for us since we now know what will happen with both ACA subsidies and taxes for the next 3 years. But worrying about what will happen in the 2022 and 2024 elections is not productive for us. Though we will do our best to support our preferred candidates in both elections for sure. Finding the silver lining in our personal finances calms us down and helps us stay open to what might come next. At AOC we are always looking on the bright side while doing research to understand what changes might come, hence our motto, All Options Considered.

LikeLike

[…] instead of the limits for the 0% Capital Gains/12% Ordinary Income tax brackets would help you take advantage of enhanced premium credits offered by the Inflation Reduction Act of 2022 for another 3 […]

LikeLike

It’s always enlightening to see your money brains at work. Thanks for sharing.

LikeLiked by 2 people

Thanks Skip! Health insurance costs are still among the main topics we tend to focus on. And on the good side, health insurance costs aren’t as intimidating as they were before we retired. We just need to keep an eye on our strategy and put enough focus into the budget items that matter most to us, like health care!

LikeLike