Our health insurance plan for 2021 is set! It was fascinating to take a couple of cold winter months to review a few options and get to a plan we felt comfortable with. The personal details we focused on for our research included living full time in the USA this year (instead of being international nomads), and changing our residency from Washington State to the state of Arizona this year as well. We started by looking at our previous insurance plan for 2019 and 2020, and then added two other options that seemed realistic for us in 2021.

Our goal with health insurance is to prevent major medical conditions and catastrophic emergencies from draining our retirement accounts. We want to avoid being in a situation where we’re dealing with a combination of medical and financial turmoil, which feels attainable since we reached FIRE (financial independence / retire early). And in case we haven’t said it enough, reaching FIRE definitely changed our lives. Our FIRE plan included making sure we had enough disposable income to pay for health insurance and a plan for our Long-Term Care needs as well. We kept this concept in mind as rule #1 when comparing our three options for health insurance in 2021. Those three options were global medical insurance, national health insurance in the USA, and ACA health insurance in the state of Arizona.

First, the Options We Won’t Consider

Since we keep getting asked questions about two health insurance alternatives, I’ll start by saying there are a few options that we are not willing to consider. We aren’t willing to consider having no medical insurance at all. We also aren’t willing to consider faith-based health share ministries or a direct primary care physician plan.

Health shares: Monthly premiums with health share ministries tend to be much cheaper than real insurance. But/and, health shares ministries offer scenarios like “freedom from insurance” for “like-minded” people following Christian traditions with a “commitment to core biblical principles.” Health share organizations can discriminate, exclude people, exclude pre-existing conditions, and refuse to reimburse medical costs for many reasons. Sure, LGBTQ families like ours can join as two separate individuals instead of joining as the legally married people couple we are. And sure, people can join and sign documents saying they will commit to following Christian traditions and avoid “behaviors and lifestyles” that the organization doesn’t approve of, and then people are free to disregard all of that and live normal lives like us. But that is not something we would do. If you don’t mind that health shares discriminate and you also don’t mind committing to their version of what’s acceptable in terms of lifestyle and behavior, there are lots of other good reasons to avoid them. For example, health shares tend to treat pre-existing conditions differently for people who were adopted, which makes no sense at all. And they really can refuse to pay for normal medical tests and normal medical procedures. They have no legal obligation to pay for medical claims! WTF? In short, health share ministries are offensive to us personally. And from a personal finance perspective they are poor wealth protection systems since there’s no guarantee they will cover your medical costs.

Direct primary care: These simply don’t appeal to us because they’re not comprehensive insurance. Sure, you might be able to save on costs with your primary care physician by having a direct connection to them and paying a monthly retainer to your one doctor to cover appointments with them. And sure, there are other benefits like saving time on paperwork by having direct access to a physician without involving an insurer. But this is not a real health insurance plan, it’s just a direct connection to a single physician. With direct primary care you’re still in a self-insuring scenario without standard benefits relating to the most important elements of essential coverage such as specialists, urgent care, emergency rooms, and hospital stays. If we’re living in the USA full time there’s no way we would consider being self-insured. The idea of having a gap of even a few days without comprehensive insurance in the USA terrifies us because medical costs are so extreme in our home country. That’s why we went to the UK for the last 3 months of 2020, to avoid losing our health insurance before the end of the year. In short, the level of financial risk with having a direct primary care physician instead of actual health insurance is too high for us personally. And from a personal finance perspective this is a poor wealth protection plan without systems in place to cover major medical costs.

Second, the Options We Did Consider

Option 1 – Worldwide Insurance With IMG

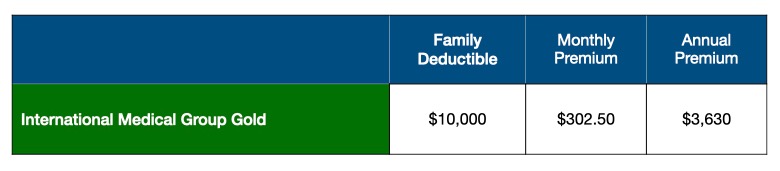

We were insured with International Medical Group’s (IMG) Gold plan for 2019 and 2020. Our plan was to start using our plan electively in 2020 for a broad range of preventative care as well as specialist appointments since preventative care becomes available after 12 months. But first we interacted with IMG a few times in 2019 because Alison had emergency blood pressure issues when we moved from Ecuador to Panama.

When Alison received emergency care as well as specialist care in 2019 we were able to waive half of our $5,000 deductible for treatment outside of the USA so we only had to meet a $2,500 deductible. But our total out of pocket costs were only $1,623 (for an emergency room visit, lab tests, a visit with a cardiologist, an echocardiogram, multiple visits with a primary care physician, a 24 hour blood pressure monitor, and about six months of blood pressure medications). We were grateful that we never met our reduced deductible in 2019.

In 2020 we increased our deductible from the original $5,000 family amount to $10,000 in order to lower our monthly premiums, and we scheduled some appointments for March and April of last year. We had appointments with a primary care physician and some specialists in Mexico including a cardiologist, a dermatologist, and an ophthalmologist. We managed to see the ophthalmologist but once COVID became a pandemic our other doctors canceled our in-person appointments and social distancing became our new primary focus. We were disappointed to see our medical tourism plans fall apart last year but we came up with a new plan for health care in the USA.

We each had a pair of virtual appointments in September of 2020 with a primary care nurse practitioner in the USA to handle our preventative care appointments and order our comprehensive blood tests. The preventative care appointments and blood tests were billed through the UnitedHealthcare PPO network, IMG’s arm for medical services in the USA. Our IMG insurance allowed for $250 of adult preventative care services per year after 12 months of continuous coverage. Our costs totaled $372 (for four virtual appointments with a primary care provider, one trip to the lab for blood tests for me, and two trips to the lab for blood tests for Alison). That’s after UnitedHealthcare negotiated our costs down on our behalf and covered $250 for each of us. That $250 for preventative care would have gone a lot farther for treatment outside of the USA, but we were happy with how things went with our care inside the USA using our IMG plan. We never met our deductible in 2020 and we were especially grateful for that.

IMG Premiums for 2021

Minimum Essential Coverage With IMG: All benefits are available (outpatient services, emergency services, hospitalization, mental health services, prescription drugs, rehabilitative services, laboratory services, preventative and wellness services, pediatric services, and maternity and newborn care). Though maternity and newborn care are only included at the platinum level. Whether these benefits are available before or after meeting your deductible is another matter, as long as they are available.

What We Like About IMG: Global coverage with no tax implications. $250 for preventative care each period/year. For treatment outside of the USA, or treatment in the USA using the concierge system, they waive 50% of the deductible up to a maximum of $2,500. They negotiate rates with providers in the USA to get costs down. You can enroll at any time, as long as you’re willing to leave the USA and travel internationally with enrollment. And when I called them in a panic in 2019 to clarify the rules before taking Alison to the emergency room in Panama, the IMG representative I talked to basically said, “Don’t worry honey, you can go to any hospital and see any doctor. If they don’t accept our insurance we’ll still reimburse you for costs over your deductible.”

What We Don’t Like About Our IMG Plan: Pre-existing conditions are not covered, and IMG can refuse coverage for individuals based on their pre-existing conditions (and they have refused coverage for some of our friends including a cancer survivor). There are a ton of limitations and exclusions for various types of medical treatments that we think should be covered such as abortion, infertility, sex change, etc. Coverage limits exist including $5,000,000 per policy for each individual; $2,250 per day for hospitalization/room & board in a semi-private room; and $4,500 per day in intensive care. And of course what we disliked the most is their limit of 180 days allowed in the USA, but I can understand that since health care costs are so expensive in the USA.

Bottom Line on IMG: We were very happy with our global health insurance from IMG. We started our policy in January of 2019 and we’ve paid for coverage through the end of January in 2021. Our policy requires that we reside outside of the USA for six months or more in a calendar year, and since we have no plans to travel internationally anywhere near that much in the next few years this policy no longer fits us. But we would gladly consider using IMG again in the future if a full time travel lifestyle becomes safe and desirable for us again someday.

Option 2 – National Insurance With HSP

I wanted to make sure we considered at least one option for national health insurance in the USA, outside of the ACA system. I got into this option knowing nothing about it beyond the fact that these plans don’t have tax implications and we had hoped to continue with health insurance that wouldn’t have tax implications. My attempts at gathering information from some FIRE community friends who have this type of insurance themselves didn’t answer enough of my questions so I contacted an insurance agent and had her build a couple of proposals for us. The agent explained that the plans she works with are commonly referred to as “RV health insurance” because they’re most frequently used by people who live a nomadic travel lifestyle within the USA. The plans we discussed are not ACA compliant and you don’t need an RV to qualify. These plans are a popular alternative to the ACA for people like us who don’t have employer-sponsored benefits and are also too young to qualify for Medicare. Even if people are living in one place and not living nomadically like RV’ers.

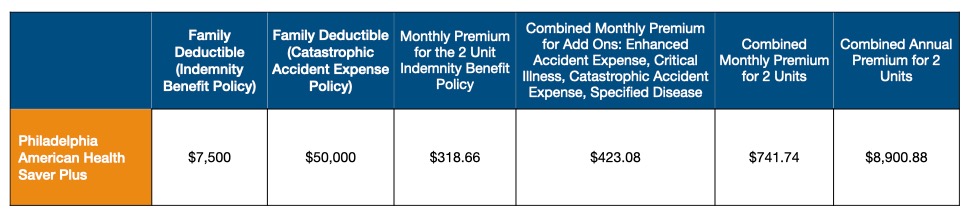

The plan I ended up focusing on was the Philadelphia American Health Saver Plus (HSP) Gold Edition Policy. The agent I worked with clarified that this plan starts with a main umbrella policy and then offers some additional pieces you can add to get an overall package that looks similar to what we’re used to seeing in a single health insurance plan. Of course you can opt to only take the main umbrella and decline any other pieces. But since we’re looking for health insurance and wealth insurance with that plan, we only looked at the combination of pieces that the agent said would offer us more comprehensive protection during a major incident. When I asked if there were also bronze and silver options the agent said there’s only one policy and it’s called “gold” to differentiate it from previous versions that were not as benefit rich as the current plan. The HSP policy has different deductible levels and it also has different “unit” levels. The more units you have the better and more expensive your policy will be. We priced the two unit plan and the 3 unit plan, but skipped the 1 unit plan since it carries too much risk of having huge medical bills that wouldn’t be refunded.

In order to try to simplify the confusing amount of details and options I was given for the HSP policy, I’m only including costs for the recommended 2 unit package below. Note that there would also be $70 in non refundable application fees for this package.

HSP Premiums for 2021

Minimum Essential Coverage With HSP: Most benefits are included (outpatient services, emergency services, hospitalization, prescription drugs, rehabilitative services, laboratory services, and pediatric services). But maternity and newborn care are not included. The only mental health related treatment they cover is confinement. Preventative care appointments are allowed after 60 days but there’s no coverage for routine health exams, periodic check-ups, or routine physicals. Whether these benefits are available before or after meeting your deductible is another matter, as long as they are available.

What We Like About the HSP Plan: Nationwide coverage with no network provider limitations. No tax implications. Lower premiums. People can enroll at anytime.

What We Don’t Like About the HSP Plan: No network means they don’t negotiate costs with providers on your behalf. Pre-existing conditions are not covered for the first 12 months, and they can refuse coverage for individuals based on pre-existing conditions. There are a ton of limitations and exclusions for various types of medical treatments that should be covered such as abortion, infertility, sex change, etc. Qualified reimbursements are at fixed prices like $3,000 max for the first day of hospital admission after hitting your deductible (and reimbursement options are lower for lower deductibles and plans with fewer units). Coverage limits exist including $250 per year for mammogram costs and $500 for the first three years for colonoscopy costs without polyps.

Bottom Line on HSP: This plan would cover us outside of our residency state in the same way it would cover us in our residency state. Even though it’s more affordable than unsubsidized ACA plan options it’s still expensive. And it carries too much risk of having huge medical bills to pay without reimbursement so it doesn’t meet our requirement for providing wealth protection.

Option 3 – Neighborhood Network With the ACA

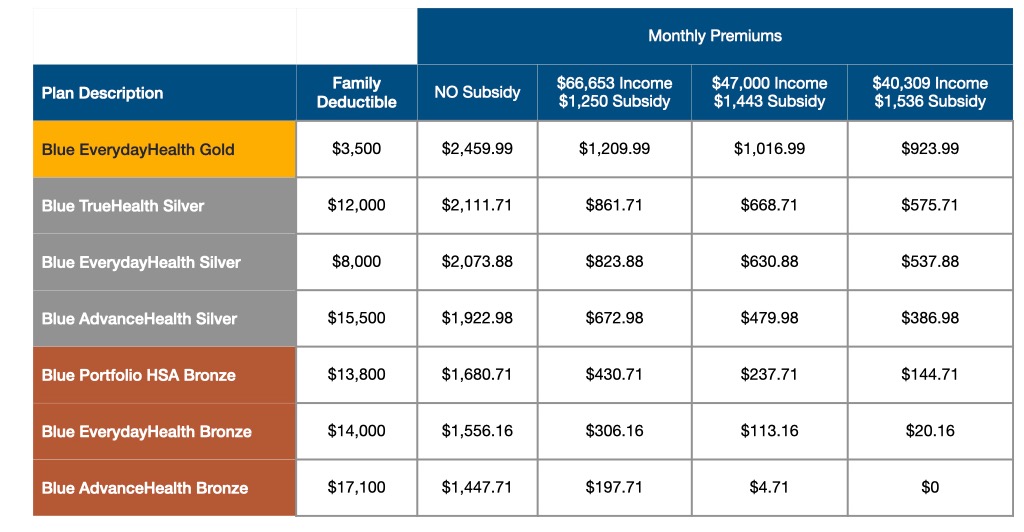

There were 28 Affordable Care Act (ACA) plans available in the specific county in Arizona we will be moving to in about a month including three gold plans, 16 silver plans, and nine bronze plans. All 28 of those plans were HMOs, there wasn’t a single PPO option available. The most expensive family deductible was $17,100 and 20 of the plans had high deductibles over $10,000.

ACA Tax CREDITS

Lots of people reference the second-lowest cost silver plan (SLCSP) when they talk about ACA costs. Some people reference the SLCSP vaguely enough that it comes across as a recommendation, but it’s not a one size fits all option that works for everyone. The reason to make note of the SLCSP is because it’s a baseline for tax purposes. Every state in the USA calculates subsidies based on premium costs for their own SLCSP, though many locations reference the one and only silver plan they have available for their calculation.

ACA subsidies are premium tax credits. Unlike most tax credits ACA subsidies can be taken before filing taxes and in that case the government pays your subsidy directly to the health insurer and you pay your share of premium costs to the insurer as well. We’re choosing to use our ACA premium tax credits in advance, which means we have to carefully monitor our actual income throughout the year and if our taxable income changes in 2021 we have to immediately modify our application with actual numbers and recalculate our subsidy to match our income. Some people might choose the option of claiming the entire ACA premium tax credit on their tax return at the end of the year. We’re more comfortable taking ACA premium tax credits in advance and being vigilant with our income, since withdrawing the entire cost of premiums from our portfolio would raise our taxable income and lower our subsidies at best, or raise our taxable income above the ACA cliff and disqualify us from receiving subsidies altogether.

For tax purposes we are Married Filing Jointly (MFJ) with no dependents. We’re able to qualify for tax credits to help pay for an ACA marketplace plan as long as we can keep our taxable income level below the 400% federal poverty level, which is $68,960 for 2021. Our spendable income is well below the limit, but our taxable income including Roth conversions can easily disqualify us from subsidies if we continue with our previous Roth conversion strategy.

In 2019 we converted $62,000 from our IRA’s to our Roth accounts and once we added our spendable income (in the form of dividends, capital gains, and other interest) to that amount to calculate our total taxable income we would not have qualified for ACA subsidies for that year. In 2020 we converted a little less at $58,000 from our IRA’s to our Roth accounts, and once we added our spendable income to that amount we would have exceeded the 400% poverty level again and been disqualified from ACA subsidies for last year as well.

One additional complication for 2021 is that we need to buy a car this year which means we’ll have to withdraw extra money from our portfolio for that purchase, boosting our taxable income some more. With all of that in mind we came up with a new strategy for 2021, and we tried verifying the implications of our taxable income plan with our CPA. Sadly, they didn’t understand the question and didn’t take the time to dig in deeper. This is the type of experience we’ve had with our last two CPAs now with every question we ask relating to our own personal finance situation. We had hoped for more helpful information from them but I guess we have become special FIRE unicorns with personal finances our traditional CPAs aren’t familiar with. Nonetheless, we did our research through the IRS and a few FIRE community members and decided to reduce our taxable income by lowering our Roth conversion.

In 2021 we will convert $6,500 from Alison’s IRA to her Roth instead of continuing with around $60,000 in conversions for our family again. By making that change we qualify for a higher subsidy of $1,536 per month. This lower estimated taxable income and a less expensive bronze level plan means we’ll end up with premiums of $144.71 per month, and a savings of $18,432 for the year in premiums.

ACA Enrollment Periods

The open enrollment period went from November 1 until December 15 and we used that time to do all of our ACA research, this time focusing on the county we decided to live in next year. We weren’t originally sure if we would qualify for subsidies in 2021 so we considered postponing our start in the ACA in order to save money since we could have kept our IMG plan until July before being disqualified by overstaying in the USA. We then would have qualified for a Special Enrollment Period either by choosing July as the right time to officially move our residency from Washington State to Arizona, or by “losing” our previous insurance with IMG when that policy was canceled. Another topic our CPA firm staff were all unable to discuss with us. We verified our Special Enrollment Period options by calling the ACA help line not once, but three different times on three different days, because we needed to hear the same answer about our special enrollment options from multiple people in order to feel confident. But once we finalized our income plan for 2021 our monthly premiums turned out to be lower with Blue Cross than with IMG, which was shocking, so there was no reason to delay starting our ACA plan.

Ambetter vs Blue Cross

Among the 28 plan options offered in our county there were only two insurers, Ambetter and Blue Cross. Blue Cross offered seven plans and Ambetter offered 21 plans. Before we retired we were insured by Blue Cross through an employer so there was familiarity there, but we had never heard of Ambetter before.

The Ambetter plan prices were all lower than the equivalent Blue Cross counterparts, and some Ambetter plans included vision and dental coverage which was very appealing. Since I saw so many different Ambetter plans I assumed they were well known in our area, but since we had never heard of Ambetter I did some digging and found that as of 2018 Ambetter was providing plans in 15 states, and a class action lawsuit alleged they misled customers with physician coverage networks that were narrower than advertised. For the 2021 plan year Ambetter is claiming services in 20 states. Ambetter is still an unknown and unproven brand from our perspective, which is ok for little things like clothing but we wouldn’t go with an unknown brand for a car purchase and we definitely wouldn’t go with one for our health insurance.

Blue Cross of Arizona

The next thing we did after dropping the Ambetter options was to drop the one gold level Blue Cross plan because the premiums were so high at $2,459.99 per month unsubsidized. We want to avoid having super high premiums because that’s a commitment to paying high prices and we’d rather commit to lower premiums in hopes that we won’t have to pay the full deductible in a given year. Then we also dropped all of the plans that require coinsurance after meeting your deductible. There were three plans requiring coinsurance between 30% and 50%, and those plans come with a guarantee of still having to pay substantial out of pocket costs after meeting your deductible, which means they fail our test of providing wealth protection.

It was fascinating to see exactly how different income levels and subsidies change premium prices. We were initially leaning towards a silver plan but in the end we picked a bronze level policy, the Blue Portfolio HSA Bronze Neighborhood Network plan. That plan has the lowest deductible in the bronze category and lower premiums than any silver plan, and seemed like the right fit for us for next year since we’re relatively healthy and have a relatively large emergency fund.

Out of curiosity I then looked back at the equivalent Ambetter plan again which has an HSA plus dental and vision benefits. The two plans have the exact same family deductible at $13,800. The Ambetter Essential Care 2 HSA + Vision and Adult Dental costs $1,667.19 per month without subsidies, compared to $1,680.71 per month for the Blue Cross HSA plan. We could have saved a little money on premiums with the Ambetter option. More importantly we also could have had free annual dental checkups and cleanings, as well as free annual eye exams and costs savings towards prescription eyeglasses with the Ambetter plan. But again, we didn’t want to go with an unknown brand for health insurance. Maybe we’ll switch to Ambetter in the future after they have been in the marketplace for a few more years and grown their network.

Blue Cross Premiums for 2021

Health Savings Account (HSA) BONUS

We were not originally looking for an HSA plan. HSAs can be fantastic retirement accounts, but we wouldn’t open HSA accounts at this point solely for investment purposes since we would need to fund an HSA by pulling money from other investment accounts or with our emergency cash. But since the plan we chose comes with an HSA we fell into a new research project to make sure we understood what we can do with HSAs beyond the investment account option. And just because the HSA option exists with our plan, we don’t have to open HSA accounts. But after doing some reading we will each be opening HSA accounts. Since the standard MFJ deduction for 2021 is $25,100 and most of our income will be in the qualified capital gains brackets and taxed at 0%, we don’t have enough ordinary taxable income for an HSA tax deduction to be beneficial.

So why pick a plan with an HSA? We each want to fund HSAs for the purposes of paying for some larger elective qualified medical expenses as well as non-elective medical expenses that might surprise us. We also want to open HSAs to unlock tax-free IRA dollars for future long-term care expenses. And it turns out that process could lower our ACA premiums as well. Here’s our plan for making all of that happen:

Qualified HSA Funding Distribution (QHFD): We’re now limited in our ability to make sizable Roth conversions while also qualifying for ACA subsidies. But we can make a once in a lifetime rollover Qualified HSA Funding Distribution (QHFD) from an IRA to an HSA up to the annual HSA maximum per person regardless of age. Since we’re MFJ, in 2021 we’ll move $7,200 for family coverage plus a $1,000 catch-up contribution from Alison’s IRA to her new HSA since Alison is over 55 years old. Then next year in 2022, I can move $7,200 for family coverage from my IRA to my HSA, and Alison can move a $1,000 cash catch-up contribution into her HSA. One thing to keep in mind is that after making QHFDs we will be required to remain eligible for our HSA accounts for 12 months following each transfer. This will be a great way to unlock some tax free IRA funds early and reduce our RMDs in the future. This was another tax related topic that our CPA firm couldn’t speak to, so again we are unicorns!

IRA Distributions After Age 59.5: Regular HSA contributions using IRA distributions are allowed after age 59.5 without penalties. That combination of IRA distributions and the HSA contributions basically cancel each other out for tax purposes and keeps you from increasing your total taxable MAGI. Pre-tax dollars coming from an IRA after 59.5 are taxed at current ordinary income rates and contributing those funds to an HSA almost makes the IRA distribution a non-taxable event. If we combine funding an HSA with smaller annual Roth conversions we’ll basically be doubling the funds we’re shifting out of our IRAs into tax-free accounts ($6,500 into a Roth and a max of $8,200 into an HSA), making those funds available for future long-term care needs.

Qualified Medical Expenses: The other reason we’re motivated to fund HSAs is that we know we’ll have qualified medical expenses in the coming years. I have some pretty significant vision problems and it’s getting harder and harder to manage my vision with eyeglasses. I have been planning to consider elective corrective eye surgery in the near future and I was hoping to have that done in Mexico with the awesome eye surgeon I met there last year, but that doesn’t seem realistic now. So my new plan is to use HSA funds to help cover the deductibles, copayments, and other costs of having that procedure done in the USA where it’s much more expensive. Thank goodness lasik eye surgery, radial keratotomy (RK), and other corrective eye surgeries are qualified expenses under IRS Section 213(d) and reimbursable using HSA funds.

Our HSA Funding Strategy:

Blue Cross Neighborhood Network: In the county we’ll be living in next year we’re only able to choose neighborhood network plans which means our network is limited to our county for most services and treatments, with some specialized care only available in Maricopa County’s bigger hospital system two hours away. We’ll have to be extra careful about staying in our network for any medical treatment we receive.

Minimum Essential Coverage With Our Blue Cross Plan: All benefits are included (outpatient services, emergency services, hospitalization, mental health services, prescription drugs, rehabilitative services, laboratory services, preventative and wellness services, pediatric services, and maternity and newborn care).

What We Like About Our Blue Cross Plan: Pre-existing conditions are covered. You only pay your network cost share for emergency services, even if those services are received from health care providers outside of your network (we still have to be very careful about what qualifies as emergency services outside of our network).

What We Don’t Like About Our Blue Cross Plan: ACA premiums are incredibly expensive without substantial subsidies. Coverage varies by state / is not equal across the USA. There are a ton of limitations and exclusions for various types of medical treatments that should be covered such as abortion, infertility, sex change, etc. We are limited to our neighborhood network for all care other than emergency services, which means we don’t have access to comprehensive health care outside of the area we live in.

Bottom Line on Blue Cross: It’s frustrating for us that we won’t be able to do as large of Roth conversions if we’re on the ACA and want to qualify for subsidies to help control our premiums. But what matters most for us is having comprehensive health insurance in the USA with pre-existing conditions covered. We’re grateful to have a deductible that we can cover with our emergency fund cash and peace of mind that our insurance will do its job after that. We’re very fortunate to have a health insurance plan that works for us since not everyone can afford an ACA plan.

The one thing that is most frustrating about ACA insurance is that it’s supposed to be affordable. It is the Affordable Care Act after all. But there are tons of families in the USA who don’t qualify for subsidies and can’t afford ACA plans, and that is unacceptable. As the ACA is reformed over time it must be made affordable for the families who need it most including everyone without extra cash to help cover all of the minimum essential coverage elements of comprehensive health care.

Bizarre Cost Comparisons

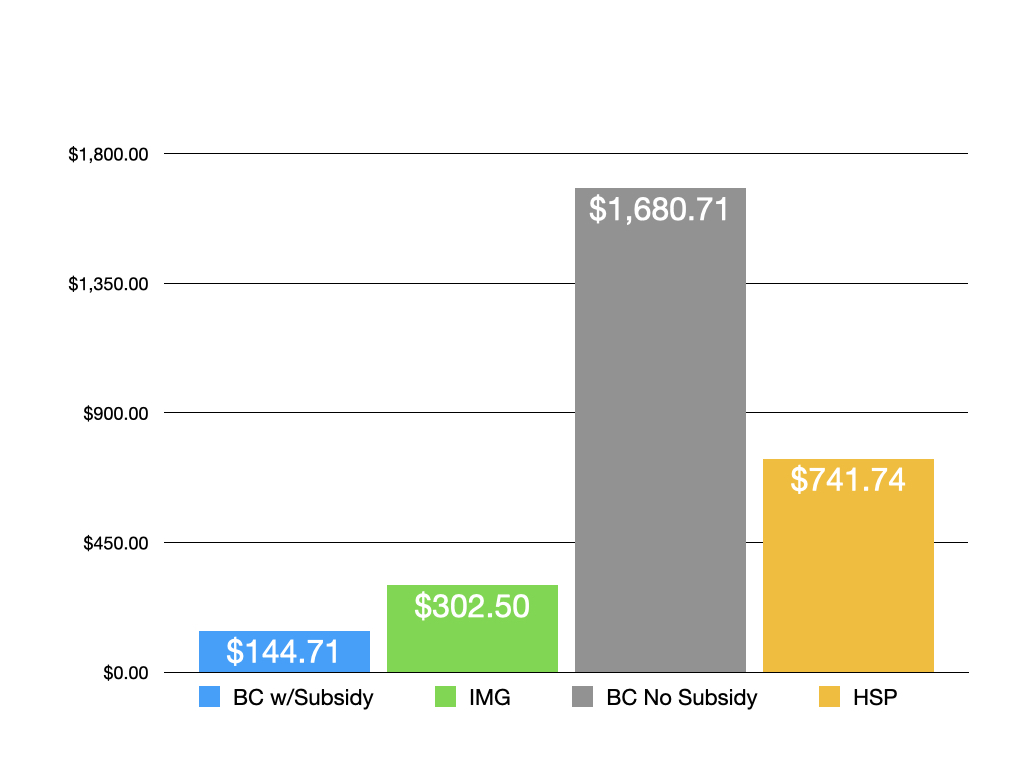

When we started our research into our 2021 health insurance options we really had no idea how expensive or affordable it might be. Our intent was not to choose the cheapest plan, it was to choose the most logical and comprehensive plan for us in 2021 alone. Now that we’ve finished reviewing all of these plans it’s pretty bizarre to compare the prices. Especially considering the fact that we chose a plan that is both the most expensive and the most affordable of the three plans we reviewed. The bar chart below includes the Blue Cross plan we chose with and without our subsidy, along with the costs for the IMG and HSP options as well.

The AOC Bottom Line on Health Insurance

In case it’s not perfectly clear by now, we believe having real health insurance in the USA is incredibly important. It’s health insurance and it’s also wealth insurance. We currently have almost three year’s of living expenses saved as an emergency fund — and we still need comprehensive health insurance. Making a frugal choice to go without real health insurance in the USA would feel far too risky for us.

Our Blue Cross health insurance through the ACA marketplace started on January 1, 2021. And we’re currently still covered by IMG for January as well. We feel a tremendous amount of relief knowing our safety net is in place, and that gives us the confidence we needed so we can return to living full time in the USA.

We are not certified financial professionals. For more information please read our Disclaimer.

How were you able to start your ACA plan of Arizona when you aren’t moving to Arizona for a month or two? I thought you had to be a resident before you could get that plan.

LikeLiked by 1 person

Great question Susan! The short answer to your question is that we don’t have to be in our house in Arizona to qualify for our new ACA plan. And here’s the long answer…

We already own a home in the state of Arizona and we used our home address in Arizona for our ACA application. We also initiated our ACA coverage during the Open Enrollment Period for 2021 with no previous ACA related residency. So there’s no formal change of residency in the ACA application process in our case (if we had applied in a Special Enrollment Period we would have triggered it through a change in residency but again we did not choose that option). Within our ACA application we legally declared residency in the state of Arizona for tax purposes as well as health insurance purposes, and we will be filing 2021 taxes as residents of the state of Arizona starting January 1.

We look forward to arriving at our new home in January and we’re glad to have crossover of two insurance plans until end of January. Between now and then we’re covered for emergencies by two plans, which is twice the emergency safety net we’ll have later on if we leave Arizona with only our ACA plan in place.

LikeLike

Congrats on choosing a plan and getting through the obstacle course that is the US healthcare system. I love how detailed your posts are! I have never heard of the QHFD and will now be researching that info for myself. Any particular resources you can recommend for information?

LikeLiked by 1 person

YES!

If you work with a tax professional do send some questions their way about the QHFD since they might know more than our CPA did.

We found the QHFD by accident through our research about HSAs and then did more digging on that topic specifically. As we learned more our biggest question was about the ability for each of us to do family level QHFDs into our two separate HSA accounts and that level of detail doesn’t seem to have as much content as the basics, but everything about the QHFD is worth reading.

Here are a few of the sources we found that answered our toughest questions about this particular HSA funding option. We found the Intuit Q&A to be the most helpful in answering our question about both spouses being able to do QHFDs into their own separate HSA accounts.

https://www.irs.gov/instructions/i8889#idm139932616590976

https://ttlc.intuit.com/community/retirement/discussion/can-wife-make-qualified-hsa-funding-distribution-from-ira-for-8-100-in-2020-if-high-deductible-plan/00/1718706#

https://wealthyaccountant.com/2019/04/28/the-once-in-a-lifetime-ira-transfer-to-an-hsa/

https://www.fiphysician.com/qhfd-a-backdoor-hsa/

LikeLike

Make sure you read all the way through all the comments on both the Intuit Q&A and The Wealthy Accountant post. We also posted on some FB FI and accounting groups and had little feed back sadly. I’m sure we will learn much more when it’s time to file.

LikeLiked by 1 person

Info not prayers. Ugh

LikeLiked by 1 person

You’re welcome Kelly. Thanks for the “chat!” 😁

LikeLike

Wow! Another excellent article. So full of interesting information. Very interesting to read how the ACA option impacts your Roth conversion strategy.

You bring up a good point concerning the actual affordability of the affordable care act. It is ironic that financially independent individuals are in a unique position to utilize ACA to it’s fullest potential. They have much more control over their level of income from year to year due various reasons and can still live well on less. However, middle and lower middle income families often see little too no benefit.

BTW, you don’t need no stinkin’ CPAs.

LikeLiked by 2 people

HA!! I 100% agree that we don’t need a CPA anymore for our personal income tax filings. But we still want a CPA to handle the taxes for the two family trusts we manage, one for Alison’s aunt and another for my aunt. We don’t want the tax liability for those trusts to rest on our shoulders. Too much information? 🙂

As for how unaffordable the affordable care act plans are, that is definitely our main takeaway from this research project. And it’s depressing. FIRE people like us are in a great position to handle ACA premiums, but there are huge numbers of American families making too much to qualify for a decent subsidy but not enough to afford an affordable care act plan. What can we do about that? Maybe I’ll write letters to Senators Elizabeth Warren and Mark Kelly.

LikeLike

Wow, this is super helpful! Appreciate your detailed and organized posts. 🙂

LikeLiked by 1 person

Thank you!!! Glad this post is helpful for you and hope you have a happy and healthy 2021. 😊

LikeLike

Love your article on this. We too ran the gauntlet of options when we started our own FIRE journey. We have been insured via the ACA for the past few years, this year doing a bit of Roth conversion. Never looked at the HSA option plans deeply, but next year (55 for me) that will be something we look at to help with medical costs and RMD planning.

LikeLiked by 2 people

Thank you Tony. Now that we’ve come up with the current plan we are definitely going to stick with the HSA option. The IRA to HSA transfers won’t make up for the Roth conversions we wanted to do but they will help both on the IRA side and on the medical costs side. We’re so glad we figured this out and picked the plan we did. 😊

LikeLike

Thanks for performing and then sharing your research into the complicated health care market! This is probably the scariest part of retirement planning. Hopefully the state of health care costs and insurance improves over the next decade, need to read as much as possible to understand it as it develops.

LikeLiked by 1 person

I do think health care in the USA is the biggest challenge for planning early retirement since our country set the system up to provide health care through employment (huge mistake) instead of a consistent national system like other countries have. The only thing we know to do for sure when planning for retirement is way over estimate budgets so we can manage the cost of health insurance while we’re still young and can’t qualify for Medicare. Our expenses while employed are not remotely consistent with what they will be after retirement when we are 100% responsible for paying taxes as well as for overpriced health insurance costs without the benefits employers provide. Like you said I have to assume the current ACA system is still in its infancy and the government will continue to improve it over the next decade. We will all be watching and hoping for the best!

LikeLike

We wound up with a similar plan for my wife, since I’m covered by the VA. We did try to optimize for limiting overall annual expenditures, so paid a slightly higher premium in exchange for a lower total out of pocket cost.

The sad irony of the ACA plans is that the ones that require $0 out of pocket (with the subsidy) are the ones that require the highest deductible – the Bronze plan. The intended target of the ACA usually can’t rock up with a five digit deductible annually; after all, the 100% federal poverty level for a married couple is $17,240 in AGI.

It’s disappointing about not finding a CPA to round the final turn and give you specific numbers. I’d give my clients a plan and then tell them to verify the numbers with their CPAs. You’ve done the leg work that a CFP would typically do. Fortunately (trusts notwithstanding), you’re in a relatively uncomplicated tax position that should leave you with only a few numbers to fill in on the optimization model. The challenge is, if you have short term capital gains or ordinary income, optimizing over 2 years to determine how much to pull into the current year or push back into next year, since conversions and asset sales must occur in the tax year itself.

It might be worth checking out https://www.early-retirement.org and seeing who pops up as a competent CPA if you decide you need help in the future. However, you can probably just as easily take 2020 returns and plug and play for next year and get pretty close; the trick is including the tradeoff of subsidy premiums for tax $ over multiple years. It seems like you’ve got the modeling and planning pretty licked! 🙂

LikeLiked by 1 person

I honestly can’t imagine how people are able to afford the ACA with these types of incomes when they aren’t retired FIRE community people. The deductibles and premiums are not at all logical for a typical family’s financial health. Imagine having that type of income with a mortgage and 4 mouths to feed, and then trying to come up with those 5 digit deductibles. There’s so much risk for people in these brackets.

It must be interesting to be in a situation like yours where you and your wife don’t have access to the same health care programs. It’s great that you have the VA system in place for yourself though. And it’s interesting to know that your wife picked an ACA plan that’s similar to ours.

Those awesome FIRE-related CPAs are out there, we just haven’t found them yet. But at least we have a FIRE CFP friend to bounce ideas off of! 😊

Maybe I’ll take some CPA classes this year…

LikeLiked by 1 person

This post was so informative I had to read it multiple times!

I am glad you called out the Health Shares. The religious ones bother me. The discrimination against people with pre-existing conditions seems like the exact opposite of being all inclusive that a religion would normally try to be.

We just did our 2021 HSA contributions this morning but will definitely have to check out the QHFD for 2022.

Dragon Gal had insurance with Ambetter in 2020. She didn’t need to use the insurance at all but from my research it seems like they have been around in our area for a long time. BCBS was an HMO and required a PCP and referral while Ambetter was an EPO and didn’t require a PCP or referrals to specialists. For 2020 I was still on Cobra with my job.

For 2021 we are getting small business insurance through our state. We met with an insurance broker and he guided us through the process. We created an LLC and as a husband/wife we can get small business insurance without needing an additional employee not related to us. There are no subsidies for the plans but we are able to be with BCBS in a nationwide PPO instead of a state-only HMO. The plans are comparable in costs to ACA plans without subsidies but at least give us the larger network. I really want to still see some of my specialists and they are not in the marketplace plans but are in the small business plans.

You two should start your own side business…you can teach the CPAs about optimization for FIRE. Ha ha!

Dragon Guy

LikeLiked by 1 person

Thanks for saying that about the health shares. I think the only solution there is to force those types of organizations to follow the same rules that insurers have to follow in order to protect the families that rely on them. The lack of consistency is problematic. It is very unChristian of them to refuse to cover normal medical expenses under the guise of “pre-existing conditions.” I really appreciate your feedback on this topic.

As for the HSAs, do check out the QHFD. It’s like the best kept secret in HSA account options. We’ll be looking forward to hearing what you find out about doing a QHFD in 2022.

That’s interesting about Ambetter. I don’t know what area you’re in but it would be interesting to know how long they have been there. Another friend of ours in Washington State said Ambetter has been in that area for a few years, but their medical practice didn’t actually accept Ambetter. That’s the only other person I’ve found who had heard of them at all. I have read that PPOs seem to be disappearing in the marketplace for personal use, but are still available to corporations. HMOs seem to be more desirable for insurers and that’s very unfortunate since I think PPOs work better for people.

I love that you’ve figured out the LLC hack for yourselves in order to get around some of the bigger limitations of the ACA, and just created your own PPO insurance plan outside of the marketplace. Bravo Dragons! 👏👏👏

LikeLiked by 1 person

As always, this is so comprehensive! It’s the biggest, hairiest area that’s held me up in our projections for any ER future.

I’ve been thinking that more and more there is a call for specialty CPA / finance advisors who understand and advise on the tax implications and nuances of being retired early.

LikeLiked by 1 person

Thanks, and yes we totally agree. We had the same concerns and that is all related to our decision to completely avoid the ACA for the first two years of our early retirement. We ran ACA numbers every year but I still feel like we weren’t really able to see what we would have to spend on an ACA plan until we filled out the application with a couple of years of experience in retirement already under our belt. Reaching FIRE gives us the ability to modulate or manufacture our income and we had to experiment with a variety of income totals in order to figure out how to manage our ACA plan costs. Pretty ironic when you think about it. It’s nice that we have the ability to keep retooling the costs that way, but that’s really a reminder that the system is kind of crazy and really not set up to be a solution for the majority of people who really need it.

LikeLike

thanks so much for the article, it was excellent. my biggest need is an ACA plan that will cover me in the entire US and that’s super hard to find for the plans i qualify for with subsidy. they all seem to cover you either by county or state, unfortunately.

LikeLiked by 1 person

Yes that broader option for ACA coverage really seems to be disappearing and that is very disappointing. My fingers are crossed that we’ll see it again in the future. And I think there may be some states still offering that type of PPO coverage with out of state network access. But if it’s out there I don’t know where. Something to keep an eye out for though.

LikeLiked by 1 person

Wow the complication of it all is astounding!!

Left the US 25 years ago, and are now happily retired in Europe, where health insurance is paid through taxes. We’ve had some major health crisis develop for my wife some years ago, and we got them sorted brilliantly in Asia for a fraction of the premiums you mention. Very informative post, I can’t even imagine the amount of work it took you to put this all together. My two cents: if you plan on living in the USA, I agree with you that health insurance is extremely important. If, however, you ever consider living abroad and just visit the US, you can save the premiums and invest in your lifestyle. We buy health insurance ad hoc when we visit the US through Pacific Prime Insurance Company in Hong Kong. If you are ever in Northern Italy, please come and visit. Gea and Julie

LikeLiked by 1 person

Thanks Gea. That’s exactly our plan for insurance and the future. We aren’t interested in living in one place as expats, but if/when we can go back to living nomadically with limited time spent in the USA we know exactly how to do that. We’ll be grateful for less complicated taxes and much less expensive health care costs again some day.

We LOVE northern Italy! We spent some time in Florence and Cinque Terre in 2014 and can’t wait to return for another visit to see more of the area next time. It would be fun to get your Italy travel advice and to meetup with you two.

LikeLike

Calling the ACÁ hotline 3 times to verify your special enrollment options was very smart. I had the misfortune of having to interact with the Social Security Administration multiple times in 2020 for 3 different family members. I was rarely given a correct answer. Even the seemingly simple task of correcting my mother-in-law’s address and getting her SSA 1099 tax form resent involved hours of work, several different wild goose chases, and a mountain of frustration. Thank you for doing all this research and writing it up so thoroughly. While everyone’s situation my vary, blog like yours help all of us navigate these waters.

LikeLiked by 1 person

Hi Jacqueline,

Your calls to SSA last year sound really frustrating and discouraging. Our first call to the ACA was interesting because the person we talked with sounded a bit cavalier. On the second call we listened to someone pick up a physical book, flip through the pages, and then read the answers, and they did match the first person’s answers. On the third call the person knew the answers off the cuff and again repeated the same rules/options again. Even with all of that we were nervous but confident enough to move forward. I can only imagine how you felt and still feel after your calls to SSA.

Thank you so much for your comment. You are right that all of our situations vary but there are some similarities and lessons for us all in these stories and I appreciate hearing yours as well. It helps to know we are not alone!

LikeLike

Excellent post! I am a little over 5 years away from the RE portion, and my wife and I will both be 53 with two of our kids still on our insurance. Insurance through my company would probably fall into some kind of super platinum level, and I know we won’t be able to continue that after I retire. I am hopeful that something really good will come out of the blue party having control of the Presidency and Congress over the next two years.

Starting my research now to learn about the ACA subsidies and all of the other tiny details has been eye opening.

LikeLiked by 1 person

The fact that you are now 5 years from RE is fabulous. Congrats on being in the home stretch! It definitely makes sense to start thinking about what it would be like if the cost of ACA insurance is roughly the same as it is today with inflation when you retire, just in case. We were trying to run the numbers for our share every year starting in 2018 so it wouldn’t be as shocking when we were ready to get on the ACA this year. But I have to say it was still quite shocking.

We will be hoping for good changes coming down from Congress and the White House as well. Fingers crossed!!

LikeLike

Thank you so much for this post! I really appreciate you outlining the options you considered and why you picked what you did. I had no idea about the IRA to HSA options you mentioned – how awesome!

I’m very anxious to retire from my corporate job and health insurance is the biggest question mark. Happily we (we’re both 50) have a revenue-generating business/LLC that will cover our expenses and pay for whatever health insurance we choose. Hopefully in the near future we can take advantage of IMG and spend six months traveling internationally, but for the rest of 2020 I’ll be looking for options on the exchange or through an agent for small businesses.

LikeLiked by 1 person

Hi Sarah, thanks for the feedback!

It sounds like you have some great retirement hacks in place with your LLC for income and insurance. It also sounds like there are some excellent insurance options on the small business side that we don’t have access to on the exchange. When do you guys plan to retire?

As for travel, I hope the next year when we all can safely travel internationally for six months again is not too far out because I am looking forward to that!

LikeLiked by 1 person

Both of us were laid off from our corporate jobs in 2018. My husband never liked working for The Man and didn’t want to go back. We were in good financial shape so he’s considered himself retired ever since (he did work a summer job in 2019). I felt like I wasn’t done, so I started another corporate job in February, three weeks before they sent us home to work, where I still am. It’s been…fine, but my heart just isn’t in it anymore. We started the LLC mid-2019 to buy a revenue generating web site, which we purchased in September 2019. What we thought would be side hustle money has become very lucrative, with the revenue being enough to cover business and personal expenses plus money left over every month. Knowing I have F U money makes corporate life a challenge. 🙂 I’m hoping to quit my job this spring and once the pandemic is over, we want to slow travel like you with a potential international relocation at some point.

LikeLiked by 1 person

The LLC and website sound like they have worked out so much better than hoped for or expected. Good for you guys! I certainly know what you mean about corporate life being a challenge once you have that FU money in place. So here’s a question – why wait until spring? Also I don’t think we can say for sure that the pandemic will be over at a specific time. Here’s a related question – do you have your plan for post retirement completely laid out? If not this would be a perfect time to really focus your energy on that right now!!

LikeLiked by 1 person

Thanks for asking these thoughtful questions! The timing is due to a few factors. The job is in a nearby city and we got a apartment there (while keeping our house) to minimize commuting and live in the heart of a fun, walkable area. I worked from the office and used the apartment for three weeks before we were sent to work from home. (womp womp) We are moving out next month at the end of the lease, so I want to have some time to bank that extra money for a few months in case they make me pay back my signing bonus (which they can since I’m leaving before two years). The other big reason is because of my manager. He’s someone I knew/worked tangentially with at our previous company and he’s terrific. One long-time team member is retiring this month so for me to do the same immediately after would really put a lot of strain on the team. I’m planning to talk to him in the next week or so about it to give him a head’s up but with multiple months’ notice.

No, we don’t have a post-retirement plan completely laid out – that’s a great suggestion1 I think it would be a plan for the near-term/COVID life and then something different for post-COVID (if/when that ever happens…). I was just thinking about our post-corporate life budget so that’s probably a great place to start planning!

LikeLiked by 1 person

That all makes sense. You are lucky to have a boss and a team that you actually care about and people you work with that care about you. Your exit plan sounds very thoughtful.

As for post-retirement planning I think it’s time to get started on that! At this point I think it’s crystal clear that planning for one year at a time is really all we can ever do realistically. And even then we can still expect things to change. Since you’re looking at retiring around June that gives you a great first run at post-retirement planning for a shorter time frame with just the second half of 2021 in mind. And the next thing you know it will be 2022 and we can hope the world will be a much brighter and safer place next year, which means even more possibilities. It will be good for you guys to take some time now to think about what you each want life to look like after retirement. Those conversations are always eye opening and lots of fun for us as we start focusing on the things we want to change and the things we want to plan for. One person told us recently that these conversations are like opening cans of worms that lead to more cans of worms – mostly in a good way I hope!

LikeLiked by 1 person

We have been talking about setting up an LLC. More research!!!!! The QHFD is one of those little known tricks that was fun to stumble across. We have set up our first HSA and will start the transfer from Alison’s IRA next week. Keep your eyes on the horizon!

LikeLiked by 1 person

You guys obviously have a talent for writing, so you may want to consider starting an authority site, or focusing on making this site a revenue generating one. I think it was Mad Fientist who put the idea in my head in spring 2019 about buying an income producing web site. By June we had our LLC, by July we had our business bank account funded and by August we were looking at Empire Flippers daily for sites in our price range (which wasn’t a lot considering they often sell sites for millions). There weren’t a lot that met our price criteria and what did appear went quickly, like within hours. We ended up finding our site on Flippa, which is the Wild West of web site buying and selling, but got very, very lucky. The seller was honest and legit, we immediately saw the potential of the site and the asking price was fair so we pulled the trigger. We’ve increased revenue by over 300% and I feel like we’ve won the lottery. I had planned to stay with my corporate gig for three years so I’d be fully vested in their generous retirement contributions then we’d assess retirement then. But (truth bomb) perimenopause is kicking my ass and while I love my coworkers, I don’t want corporate problems anymore so I think I’m peacing out by June at the latest.

LikeLiked by 1 person

I’m so glad you are bringing this revenue generation topic up. We decided in February 2019 to start our blog and to not make it a revenue generator. But we also said we have permission to change our minds about that at any time. This is on my mind a lot lately, mostly as a “why not?” topic. So I appreciate the feedback and encouragement from you to think this through some more. And it will be great to be able to share some ideas with you more on this topic. 😊

LikeLiked by 1 person

[…] Our health insurance premiums are going down from $302.50/month for global insurance with IMG, to now paying $144.71/month after subsidies for an ACA plan in Arizona. […]

LikeLike

So relieved that you did your research and didn’t choose Am better. I started panicking on your behalf when I read that name! My partner had an ACA plan with them a few years ago, and there was not have a single doctor in our state that was in their network that was accepting new patients.

LikeLiked by 1 person

Wow that is interesting to hear!! I wonder what state you had that experience in, though I gather that’s pretty common. I sent out a general Facebook message asking friends if they had heard of Ambetter and only one had, and he said the health care practice he worked for refuses to accept Ambetter and that was a red flag for sure. Hopefully you all have an insurance plan that works well for you both now!

LikeLike

It was in Illinois.

LikeLiked by 1 person

Thanks for the feedback Maggie. I was a bit tempted to just go with Ambetter since they have lowered their prices to entice people to buy in. But I’m so glad I didn’t take the chance. I can only imagine the frustrations your partner was dealing with while insured through Ambetter.

LikeLike

[…] likely don’t include the full cost of health care and taxes. Do some research to see what your health care expenses might be without an employer. Also, do some research to see how much people pay in taxes without an employer. Then add some or […]

LikeLike

[…] since we were living as international nomads, but now in our third year of retirement we’re using ACA health insurance because we’re in the USA full time and health insurance is wealth insurance in this country. […]

LikeLike

Great read! I’ll add I think you may be underrating direct primary care providers. All the ones I have looked into make it VERY clear they are not health insurance – and recommend that their members get catastrophic insurance for serious illnesses.

What they are is a great way to get timely and quality service (i.e. no 4 week wait times to see a doctor for 5 minutes!) so that you can address the vast majority of health issues that come up without having to go to an expensive Urgent Care clinic or Emergency Room.

I also think that if you shop carefully – you can find a doctor who actually WANTS to make people better, rather than spending all their time working with insurance companies. That type of practice I think attracts them…that is the type of person I want sitting down with me for an hour and actually getting to know what is going on with my body!

I’m still trying to determine what my health care coverage plan will be for next year going into retirement. Right now I am leaning towards an ACA plan similar to the one you describe (a cheap wealth protector) and to pay a moderate subscription to a DPC which I will use for anything that is not a catastrophe.

Man I really sound like a commercial don’t I? I’m really quite impressed by this approach to delivering care:)

LikeLiked by 1 person

Thanks Steven! I’m not intentionally underrating DPC options we just decided they don’t appeal to us since we want to work within the insurance industry to capitalize on the full list of specialists rather than relying heavily on a primary care provider. We have been very fortunate to find specialist doctors and especially nurse practitioners who specialize in the areas we need most including cardio, allergy, mental health, and women’s health. Of course we hate the insurance industry and the cost of health care in the USA in general, but we have a wonderful network of specialists that we are very happy with and so far all of our needs are being fully covered by our ACA insurance plan and we’re thrilled with our nurse practitioners and doctors so no complaints here at this point.

But we would love to hear more about what you choose for yourself in retirement so I hope you will follow up once your plans are set. Cheers!

LikeLike

[…] have Affordable Care Act (ACA) marketplace Blue Cross insurance and we’re benefiting from President Biden’s American Rescue Plan (ARP). The ARP expanded ACA […]

LikeLike

[…] Health (and Wealth) Insurance – AllOptionsConsidered […]

LikeLike

[…] to our personal finance strategy health insurance is wealth insurance, which means managing our health care costs is critical to our financial wellbeing. One of the […]

LikeLike