Yes, 2021 was a strange year. It was Covid Pandemic Year # 2 so how could it not be strange?! Lots of people asked how our spending in 2021 compared to our spending in 2020. The answer is easy – they can’t be compared. In 2020 we were nomads with few belongings and very few bills to pay, and we only spent 5 months in the USA (along with 4 months in Mexico and 3 months in England). 2021 was focused primarily on setting up a new home base for ourselves along with construction of a separate living space for our housemate.

We are not certified financial professionals. This post contains affiliate links. For more information read our Disclaimer.

Lots of people also asked if we regretted our decision to buy a home in Arizona and set up a compound, and that answer is even easier – We have zero regrets! We could not be more glad, confident, and grateful about those decisions!

We did our best to plan for everything and estimate our spending accurately last year, but there were too many changes and unknowns for us to hit the bullseye this time. Spoiler alert – In 2021 we went way over our spending budgets for our household and our construction project, and it turned out that was okay.

We planned for 2021 by swapping out our simple nomad budget with a more complex home owner budget. We started with our 2018 budget categories since that was the last time we owned a home and lived full time in the USA, and that was also the year we retired early. We did our best to estimate costs for things like utilities, insurance, taxes, and food and of course we were off on almost everything since we don’t have a crystal ball.

Budgeting for 2021

As we all adjusted to life on the compound last year we tracked our spending and updated our budget to include things that popped up in real life. And we added things that were missing from our budget, including spending for mental health.

In January of 2021 we looked over the budget we put together and acknowledged that we were just guessing on all of the numbers. So we added a bit of padding (10% of our budget for the year) to our portfolio withdrawal. And we reminded ourselves that we have access to our emergency fund as a backup which holds more than two years of living expenses. Though we had no intention of using that emergency fund to cover regular spending since it’s intended for a major market drop to make sure we wouldn’t need to sell equities in a down market.

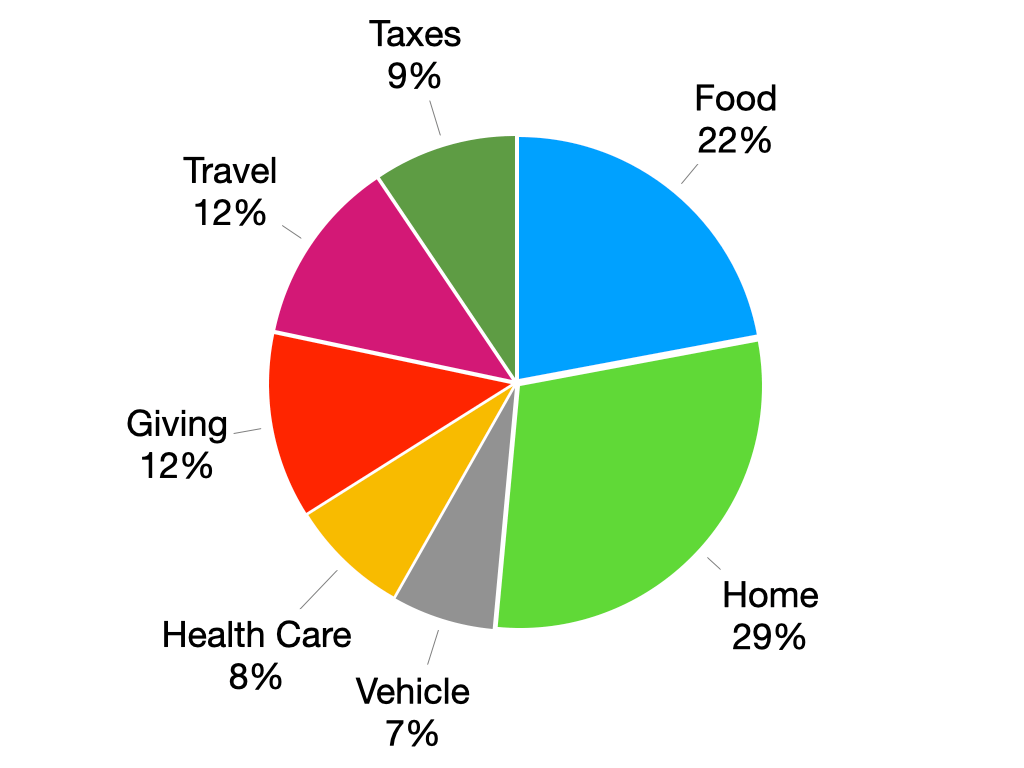

Our Spending Went WAY UP in 2021

In early January we made our annual portfolio withdrawal from our Schwab brokerage account. That withdrawal gave us cash for our living expenses, including things like food and utilities and some extra spending for furniture and home related supplies. We already had cash set aside to cover construction related spending on the separate space we were building for our housemate, plus some remodeling projects we wanted to complete in the main house.

In January we also traveled from England to Seattle where we used to live so we could empty our storage unit, and then drove to Arizona to move into our new house. Initially we settled in with just our nomad bags and things from our storage unit, but within a few days we started shopping for the things we wanted and needed in our new home.

Home Owner Spending

We enjoyed putting our home together during the first half of the year, and then our housemate joined us for the second half of the year. We saw the benefits of our new style of owning a shared living compound right away, and it’s clear that having a compound is a good thing for us!

We were curious about how our recurring living expenses would be impacted each month. We knew we were taking on a lot with our new utility bills as well as annual taxes and insurance for our property, plus car related expenses, and everything else. Having a home can be surprisingly expensive!

The first thing we noticed in our home related spending was that we let our streaming subscriptions multiply. Oops! When we were traveling full time in 2020 we had Audible, Netflix, and Hulu. That’s it. By end of 2021 we were paying for Audible, Spotify, a WNBA pass, Amazon Prime Video, Netflix, Hulu, Disney+, and Apple TV+. Having a home doesn’t require all of that so we’ll be doing some trimming to that list of subscriptions. But honestly our increased subscriptions were great replacements for going to the movies, seeing plays in the theater, and going to stadiums for WNBA games now that the Covid pandemic has made us uncomfortable about group events indoors.

On the very bright side, having a housemate has proven to be a big help to us financially. We didn’t design our compound so we’d have income to gain, we wanted a sharing community in a co-living arrangement. We set a fixed affordable rent amount that would allow our housemate to thrive financially, and hoped this sharing community arrangement would benefit all three of us in approximately 10 million ways. And our plan is working! Our housemate’s rent covers our monthly utilities and some maintenance. This means home ownership doesn’t have as much of an impact on our living expenses and that’s a huge bonus for us as early retirees.

Food Related Spending

Are you sitting down? Our food spending went up by around 25% in 2021. It was no surprise that we spent more on food while living full time in the USA. But on top of that grocery prices in the USA went waaaay up in 2021!

Another big reason for that massive increase in food spending was that we ordered restaurant meals about once a week last year. We were actually making an effort to order restaurant food consistently with the intent of contributing to our local economy that way. We also spent a fair amount of time traveling around the USA visiting with family and friends and enjoying restaurant food in California, Colorado, New Mexico, and Massachusetts. Food gives me joy so I don’t feel bad about that spending!

Giving

Since we increased our overall budget last year, we also increased our giving budget to match. And we hit that bullseye perfectly. Don’t get me wrong, we budget for giving since it’s a sizable part of our spending and we try not to go over our budget. But this is one category where increasing our spending is a good thing.

Giving is important to both of us, and we have lots of plans for giving in the future that we’re excited about. We like to imagine how our lives will change over time when we model our portfolio growth in our fancy spreadsheet. But I’ll save those plans for a later post.

Travel Related Spending

Since travel is something we value we were excited to add a travel category back into our budget last year. We picked a dollar amount for travel around the USA in 2021, and made sure we took that budgeted amount seriously. We love the way changing the scenery improves our happiness and sense of adventure, and we were proud of ourselves because we did not go over that budgeted amount.

Meeting our travel budget perfectly was not due to good luck or witchcraft though. This just happens to be an area we can more easily control. We’ll take the win, even if it really is neutral from a budgeting perspective.

Our travel expenses in 2021 included Airbnb’s and hotel rooms for each location we visited, plus a rental car in Boston. The only chance we had to use travel reward points last year was for our Boston flights, and we definitely pumped up our stash of travel rewards with our spending.

The one thing we felt a bit unsure about was whether we should continue to pay for the subscription services we got used to as nomads including our Traveling Mailbox, Trusted Housesitters membership, and a VPN. I felt less sure about the VPN but we do use it when we travel and Alison was strongly in favor of keeping it so we are still paying for that at this point.

Our Traveling Mailbox also felt like a splurge last year but we got used to it when we were nomads and we love the convenience. Now that we have a housemate who can collect our mail when we’re gone we did think about dropping our traveling mailbox. But we also set it up as the primary address for a small trust Alison manages and that made it even more useful for us since the system handles deposits for the trust. For now we’re going to keep our traveling mailbox.

At the start of 2021 Alison was leaning towards canceling our TrustedHousesitters account, because our house sits in 2020 were all canceled due to the Covid pandemic and it just didn’t seem as useful anymore. But I was strongly in favor of keeping it so we agreed to wait and see if we did any pet sitting in 2021. Standard membership for TrustedHousesitters costs $169 per year, which we look at as the equivalent of spending a night or two in an Airbnb in the USA. That means we need to book a at least a week of house sitting each year in order for that membership to be worth paying for. We booked a 2 week house sit in February, took care of some goats for about a week in November, and ended the year with a 10 day house sit in December. We definitely still love housesitting, and it helps us create getaway opportunities without paying for an Airbnb or hotel. Worth it!!

Health Care

Our health care costs were on a wild roller coaster ride in 2021. We planned for double spending in January with one last month of IMG nomad insurance plus our first month of ACA market place insurance.

After that we intended to pay for consistent lower premiums on the ACA marketplace, and we got that number to $144.71 per month after subsidies. Then starting in May our ACA premiums dropped to zero dollars thanks to Biden’s American Rescue Plan (ARP) and we were thrilled with that. But by the end of the year we decided to change our plans… again.

There’s a lot of advice out there about doing everything you can to show a lower modified income in order to maximize your subsidies and pay as close to zero as possible for ACA health insurance. But here’s the reality, we don’t have to optimize everything. We could set our income to allow for a tiny $6k Roth conversion, maximized subsidies, and zero cost premiums for our ACA plan. Or we could better take advantage of the ACA related improvements in Biden’s ARP to allow for a bigger but still modest Roth conversion, take modest subsidies, and still end up with premiums that fit within our budget. We see more value in shifting our perspective around tax planning from paying the lowest amount of taxes in a given year to reducing our lifetime tax obligations. All of our spreadsheet modeling has shown us that paying a bit more taxes now on larger Roth conversions will help us control our future RMD’s, which is more beneficial to us than rock bottom ACA premiums.

Since Roth conversions are a priority for us we chose to make $40k in Roth conversions in 2021, which pushed our health care premiums back up to $276.71 per month. That also meant we had to pay back some subsidies. And that’s worth it to us in the long run.

Then in July I resumed mental health counseling with costs fully covered by insurance for a few months, until my psychologist dropped insurance and I had to pay out of pocket. The cost of therapy this time went up to $200 per hour, and it was soooo worth it! I also started weekly group therapy with Al-Anon (a support group for loved ones of alcoholics) and added weekly donations of $5 or $10 to my group, also soooo very worth it!

In 2021 we also had the benefit of an HSA with our new ACA market place plan. In January we deposited $8,200 into Alison’s HSA, with a $7,200 Qualified HSA Funding Distribution directly from her IRA. And since Alison is over 55 years old she also got to include a $1,000 catchup HSA contribution. We were reimbursed for $4,700 in qualified out-of-pocket medical expenses from her HSA last year.

Tax Spending

There were plenty of changes in our tax related spending in 2021. First, we started paying property taxes again since we bought a home in Arizona. We were glad our property taxes are very low in our current location, compared to how shockingly high they were when we lived in Seattle.

We also bought a used SUV last year, which means we have to pay a Vehicle License Tax (VLT) within our annual vehicle registration fees. And then some neighbors gave us their old landscaping trailer, which we nicknamed Jed Clampett, when they upgraded to a new trailer so we had an additional VLT and annual vehicle registration fees. Of course VLT’s are relatively small tax amounts but everything adds up.

And last but not least, our income taxes went up! We moved our residency from Washington State to Arizona in 2021, which means we went from a state with no income tax to a state that taxes income. That’s part of the reason we were in favor of reducing our Roth conversion last year, and the ACA subsidies I mentioned above were the other reason. However, in Q4 last year we decided to increase our Roth conversion which basically meant we had underpaid with our early quarterly federal tax payments and we had to tidy up our taxes with our 4th quarter payment. That change stressed us out a bit but then we found an awesome new CPA to help us with tax planning advice and now we have more information and confidence regarding our post retirement taxes.

Goodbye 2021!

That’s it! 2021 was a year of continuing to talk about how we manage our money together, learning more about taxes, and making better spending decisions together. It was also a year of trying not to obsess about how much we were spending, and repeatedly learning that there are tons of things we can’t control. In other words same old, same old!

We could have made more of an effort to spend less while we were setting up our house and replacing things we had given away before we left Seattle. But at the same time, we had the cash we needed and we did not make any spending decisions that we regret. But one thing is for sure, there will be plenty of changes to our spending in 2022.

Hi Ali,

Very nice graphs, so visually it looks very appealing. I was kind of hoping to see real amounts posted, not percentages, since we all spend green cash and not percentages :-). Is there something you can divulge in that respect? This is an unusual year indeed and your housing was a huge spending category which is hopefully one-time, but also an investment at the same time. Maybe some items can be removed or trimmed/inflated so it doesn’t really need to be accurate to a dollar or give a range of spending without the house. Or if no real dollars can be revealed at all, maybe you can tell how the 2021 spending compares to the WR against the total portfolio value. Anyway, sorry for being nosy, I just found percentages a bit unrelatable.

Also, so your goal is to spend down taxable accounts before touching anything in the IRA (or 401k in case you haven’t moved this account to your IRA yet)? I sometimes wonder if it’s fine to withdraw some money from the IRA for living expenses too. I know that a lot of people want to convert to Roth IRA as much as possible from the tax perspective, but not spend and let the balances grow. But wouldn’t spending the IRA down also help to reduce future RMD’s? Well, so many tricky questions here to answer for each person’s or a couple’s financial situation. Boys and gals in Washington ain’t that stupid when these plans were created for people…Uncle Sam will get us to pay our fair or unfair share of taxes one way or another, LOL.

The graph shows one withdrawal. What happens to the money if it’s too much? Do you increase giving/charity or do you withdraw less money the following January?

I’d love to hear the steps you take to figure out your quarterly tax payments. Do you perform a simple calculation on a napkin or run a dummy tax report on Turbo Tax or something similar?

Thanks! And happy new year! Let’s hope 2022 is incrementally better.

LikeLiked by 1 person

Thanks for the comment! And for giving me a reason to talk about privacy and numbers again. We’re probably due for a whole post on this topic…

I get that you and others are curious since I’m a very nosy and curious person. But personal finance is too often treated like a competitive sport and we are definitely not interested in playing that game. We do not want to “feed the comparison beast” as our buddy Tanja Hester says. Also, some people think it’s safe to duplicate number goals and we absolutely do not think that’s a safe way to manage your finances since we are all unique.

We’re blogging to share experiences and ideas, not numbers. With a post like this one which is focused on our spending, we’re simply interested in encouraging others to budget and pay attention to spending. We want to talk about the fact that we have a budget, and real people like us don’t always hit the target. I think percentages do help tell that story, and that reality is much more important to us than sharing numbers.

About our housing costs, a lot of that has been one-time spending. Thank goodness! We won’t need a new couch anytime soon and we certainly don’t plan to build any additional “apartments” here beyond the one we built for our housemate. Basically, we moved cash from a money market account into a real estate investment which increased our portfolio diversity, and we are happy we bought the house. We’re in a crazy local real estate market and our investment has already increased in value almost 25% since we bought it. Stay tuned for another post in the allocation series that will talk a bit more about that.

About our account types, we moved our 401k’s to IRA’s when we retired. We intentionally built up our brokerage account to cover all of our spending until Alison is 60. Yes early IRA withdrawals would help avoid RMD’s but that would come with the cost of either penalties or lost growth or both. We were not open to accessing IRA funds early because that growth is very important for our later retirement years so we chose to build up the brokerage and reserve the IRA’s for later years. But we absolutely do plan to start making withdrawals from Alison’s IRA once she has full access to that account (and we’ll make withdrawals from my IRA when I’m 60). We have high enough IRA balances in conjunction with a low enough budget that after we add inflation to our original 3.3% withdrawal rate, we‘ll have BIG RMD’s when we each turn 72. And that’s why we are doing annual Roth conversions now, up to the level of tax and ACA premiums we are willing to accept in a year. We’re more comfortable paying taxes on those conversions now, rather than dealign with all of those taxes from RMD’s when we’re old ladies. So we’ll start pulling some of our expense money from our IRA’s after we turn 59.5 and continue chipping away at those balances in our later years.

About taxes, we try not to look at taxes as fair or unfair. We’re happy to live in a world where we contribute to the social contract we have chosen to live in, and taxes are just one part of that social contract. We focus on understanding the current tax codes so we can do our best to build a withdrawal strategy that works for our specific accounts and associated tax brackets as well as our need for income over time. This is a puzzle we try not to struggle against because we have other goals that need our energy and attention.

About our annual withdrawals in January, if we don’t spend all of that cash and there’s still some left in December, we carry that balance over for the next year which means we can make a slightly smaller withdrawal for the next year. We have ended up with something extra since we were under budget at the end of 2020, and we had extra cushion left over when we went over budget at the end of 2021. Both times we had around $5k left in cash for our living expenses — there’s a real number for you so I hope enjoy that!

About quarterly tax payments, when we review our spending and portfolio growth in December, we run calculations on each of our income types. That includes realized gains and associated taxes with each account. We then estimate the types of income we’ll have over the next year, including estimated percentages of capital gains. We then work with our CPA to build our estimated tax payments and make sure we aren’t creating tax penalties for ourselves, to make sure we comply with safe harbor rules, etc. There are free online calculators and DIY tax programs that can help you do that as well.

So there you have it! If anyone reads our posts and feels comfortable engaging in the conversation our time is well spent. So thank you for reading and commenting!

LikeLike

[…] behaves differently and we start out with a unique set of dividends, interest, and capital gains. Our spending has also varied each year which means even when we had the same budget amount we didn’t pull out […]

LikeLike

[…] The early retired duo behind All Options Considered also took a look at last year’s numbers. Like the post above, we don’t get all the numbers, but we do get their insights and a detailed breakdown by percentages. A 2021 Spending Review. […]

LikeLike