Now that 2021 is behind us we’ve had some time to review our portfolio performance along with the decisions we made relating to our portfolio last year. That review process is a great way for us to make sure we know what our portfolio has been up to and figure out if there were any positive or negative impacts from our decisions. Our portfolio review also helps us figure out if there are any changes we want to make in the following year.

This year we wanted a bigger review and look back not just at 2021, but all the way back to 2018 when we retired. Last year was our third full year of early retirement since Alison quit her job in April of 2018 and my last day was a few months later in September. So this January we were ready for a health checkup on our early retirement so far, including everything from allocations to sequence of returns risk (SORR).

We are not certified financial professionals. For more information read our Disclaimer.

2021 Market Craziness

2021 was an odd year for us and a bad year for many people since the US and world economies were still rather unhealthy and the Covid pandemic was (and still is) severe. Unemployment numbers dropped but inflation soared, supply chains broke down, and prices for everything from food to lumber went way up.

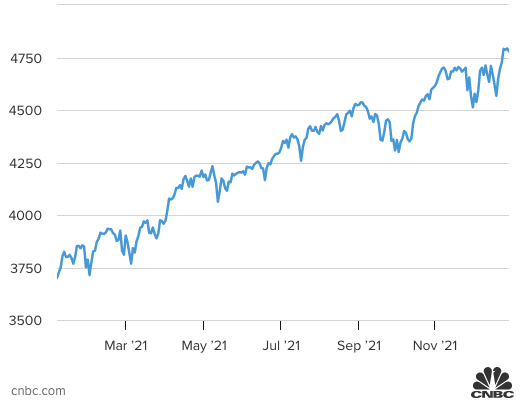

Despite the economic woes and various market selloffs last year, stock market growth was strong once again. 2021 gave us one more year of data proving the overall historical direction of the market is up! By the end of 2021 the S&P 500 had gained a whopping 26.9%. Which was good news if you were invested in equities, and the reason our portfolio had a great year.

Our Retirement Strategy

When we retired in 2018 we planned for our brokerage account to last for 15 years so we could avoid any early withdrawals from our traditional retirement accounts. Once our brokerage account was depleted Alison would be well over age 60 so we could switch to her IRA for our income needs until that account was also depleted. Then we would switch to my IRA once I was over 60 years old. But that’s not what we see happening now.

At the end of 2018 when we left Seattle our condo sale was in process and we were anxiously waiting to add some condo money to our brokerage account. When the condo finally closed in January of 2019 we put half of those funds in our brokerage account and set the other half aside for a future real estate purchase. That condo sale completed our personal safe retirement strategy so we could move on to a new life as international nomads. Our goal in retirement was to never work for income again and that seemed realistic since we had 33x our annual spending budget safely tucked away in our portfolio and a 3% safe withdrawal rate.

We did worry about SORR and tried to plan for various market corrections and black swan events in our early retirement years. We built a cushion for ourselves by having lots of cash to start with and bond funds in our brokerage account. And then we thought the Covid Crash in 2020 might be the start of a big and long lasting market correction but that drop turned out to be brief. But the Covid pandemic did bring major change to our lives since it inspired us to pull over from nomad life and buy a home base in Arizona near Alison’s mom. Now we’re happily enjoying retirement in the USA which means giving much of our time and energy to our family and friends.

We’re grateful to Vicki Robin for reminding us not to limit ourselves by just being money rats. There’s much more to life than just money!

So Far So Good!

After three full years of early retirement we’ve reached a new level of trust in the magic of compounding growth. We’ve watched our Roth accounts grow as we make annual Roth conversions from our IRA’s, and seen how our IRA’s react to those transfers without dropping much in value. Most of all we’ve been fascinated to see our brokerage account react to sizable chunks of cash being withdrawn each year to cover our spending needs. We wondered how the overall value of our early retirement account might change due to withdrawals and how growth might be diminished, but we only have good news to report so far. I think we’re doing a pretty good job of managing our money but that growth isn’t because of us, it’s luck!

Our brokerage account had a good start in retirement since we pumped it full of cash in January of 2019 and took no withdrawals as the S&P 500 grew by 28.9% that year. That was a relief since 2018 was a correction year for the market and the S&P was down by 6.24% during our last year of employment.

At this point it seems clear that our simple withdrawal strategy, combined with our ETF investing fund choices, and the market growth we’ve experienced so far have fit together more than just nicely (is perfectly too strong a word?). Our annual spending has climbed along with home ownership and inflation, but our portfolio yield has been more than high enough to support all of our spending needs. Can you hear Alison’s loud sigh of relief?

Below is a screen shot of my crazy retirement portfolio bar chart. The dollar amounts are removed here for privacy and I’ve added a few captions for explanation. This chart helps us see how our accounts react to things like market performance, annual withdrawals, and Roth conversions over time. What’s most interesting in this chart is seeing how stable our brokerage account has been during three years of annual living expense withdrawals. Because the market has been so strong that account balance has stayed relatively level.

2021 Brokerage Account Activity

All of our living expenses and other spending money comes from our brokerage account for now. Our living expenses are made up of remaining cash from the prior year (if there is any), plus dividends (our brokerage account produces around $20K in dividends each year), plus contributions to the Compound from our housemate (which covers our monthly utilities and some maintenance), plus proceeds from selling equities.

So far our withdrawal strategy has been to sell the oldest lots in our brokerage account first considering their total value, cost basis, and capital gains. Every annual withdrawal has been unique since every year the stock market behaves differently and we start out with a unique set of dividends, interest, and capital gains. Our spending has also varied each year which means even when we had the same budget amount we didn’t pull out the same amount of cash from our brokerage account each year. For example, at the end of 2020 we had $5k in cash left to rollover for our next year’s spending needs so we subtracted that amount from our 2021 withdrawal.

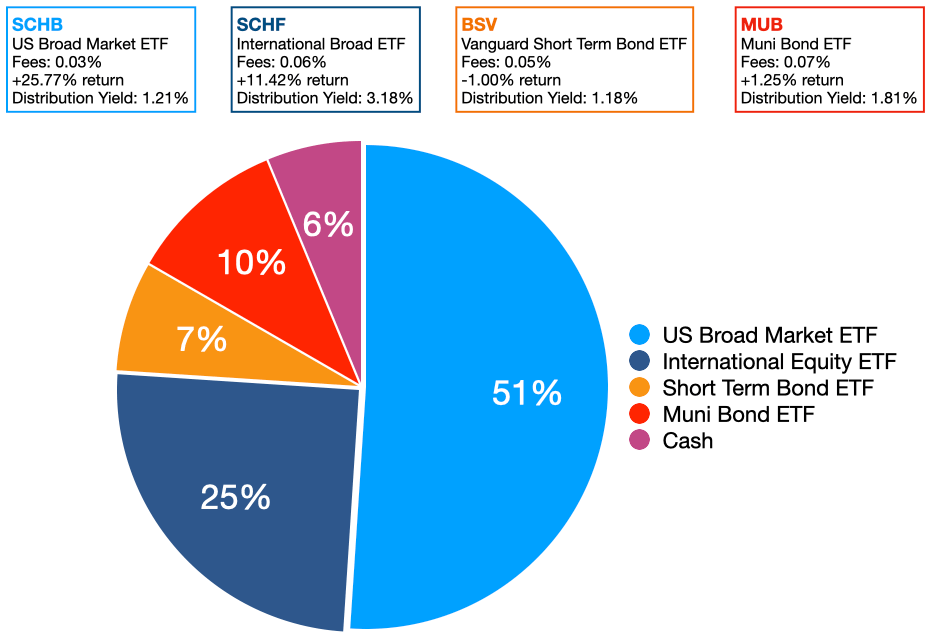

In 2021 our withdrawal was quite different because it came almost entirely from a single fund. The actual breakdown of our withdrawal for 2021 included a few of the oldest lots (first in, first out) of our International Broad ETF which made up 94% of our total withdrawal, plus a single lot of our US Broad Market ETF to make up the other 6%. That withdrawal meant our capital gains were very low at only $8,250 last year. Being able to target how much we’ll have in realized gains while also keeping an eye on our overall allocation is critical to our process, and knowing our goals for taxes and health insurance premiums helps inform our choices.

None of us has a crystal ball and we all have a unique set of numbers along with our own risk tolerance. So build your own unique personal finance strategy!

For comparison earlier this month in January we withdrew our 2022 living expenses and the breakdown was very different. This time we sold one and a half lots of our International Broad ETF plus a portion of the oldest remaining lot of our US Broad Market ETF to cover a total withdrawal of $50k. The breakdown this time was made up of only 34% of the International Broad ETF and 66% of the US Broad Market ETF. Our total capital gains from our withdrawal this year doubled from last year and totaled $17,578.

We assume our capital gains will go up again next year in 2023 because we’ve run out of holdings with lower unrealized capital gains. That will make it harder to modify our income to make it appear lower for tax and Affordable Care Act purposes. At this point we still have three big lots of International Broad ETF funds and six big lots of US Broad Market ETF funds left in our brokerage account. Those remaining lots are all so large that each one is worth more than one year’s living expenses and the biggest lot is more than seven times larger than our newly inflated annual living expenses. That means we won’t be able to clear lots in the same simple way moving forward, but the bottom line is very good news. After pulling our living expenses from our brokerage account four years in a row, and increasing our budget by 11% over our 2019 budget, we still have 18 years of living expenses in our brokerage account (*knock on wood!).

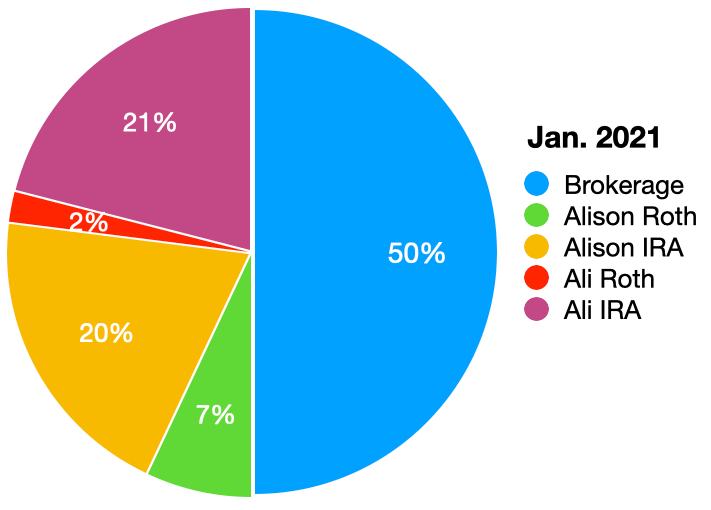

The pie chart below shows our brokerage account allocation as of January 2021, with clarification on exactly which funds we invest in.

IRA and Roth Activity

In 2021 we opened a new HSA account at Fidelity for Alison with an early withdrawal from her IRA. Alison made a tax free, once in a lifetime Qualified HSA Funding Distribution (QHFD) of $7,200 for our family of two plus a $1,000 catchup contribution since she’s now over age 55. That QHFD trick is nifty! I actually just opened my new HSA account last week (one year later than Alison so we could each take advantage of the family sized withdrawal) and made my own QHFD from my IRA for $7,300 for our family of two.

But the main activity in our IRA’s is making annual Roth conversions. Every year we have decisions to make about Roth conversions including deciding how much we’re willing to pay in federal income taxes and whether we’re converting from only Alison’s IRA, or only mine, or both. Our strategy for Roth conversions has changed every year to match our lifestyle changes and to match our latest thinking on this complicated topic. Like everything else in personal finance our Roth conversions are personal!

We originally set our 2021 income as low as possible to allow for a tiny $6k Roth conversion, maximized ACA health plan subsidies, and zero cost premiums for our ACA health insurance. And then we changed our minds. We decided we’d rather prioritize Roth conversions over near term lower taxes and lower premiums so we changed our plan to allow for a total of $40k in Roth conversions in 2021, from my IRA to my Roth. The goal now is to put our minds to managing our life time tax obligation. Consequently, that Roth conversion strategy change increased our income and pushed our health care premiums back up from zero to $276.71 per month. We hope in the future we won’t change our decision midyear but that change helped us learn an important personal finance lesson — we don’t have to optimize everything. Our top priorities include decreasing my IRA balance to avoid outrageous RMD’s later on, and increasing my Roth balance as much as possible during early retirement to allow for growth to cover my life care costs when I’m elderly.

As for the timing of our Roth conversions, we now start with an initial conversion in January that’s typically no more than half of our total target conversion for the year. We do that because we assume the market will continue to go up, which means we assume the market will be lower in January compared to December. That also allows us the chance to make an opportunistic conversion midyear if there’s a market drop, which we were able to do in 2020 during the Corona Crash. In 2021, we started with a tiny conversion in January that was half of our original target amount and then converted another $36k in late December. The final conversion is always set for later in December after we receive our last round of dividends, interest, and capital gains for the year just incase we need to make further adjustments.

Moving forward our strategy is for all Roth conversions to be made in my accounts. Alison opened her Roth back in 2009 and it already holds more than our goal for covering her estimated life care costs. Again, thank you compounding growth! Since I’m almost 11 years younger and I didn’t open a Roth until 2019 after we retired, I have a lot of Roth growth to make up for. I want to convert at least enough funds to cover my estimated life care costs from my Roth so I’ll be prepared for my old lady years way off in the distant future.

Portfolio Review for SORR

We started retirement with five years of cash and bonds ready, which funded our first year of retirement and helped with our construction here at The Compound last year as well. By January of 2022 we still have close to 3 years of living expenses ready for use if the market is down when we make our annual withdrawal, so we can avoid selling equities at a loss in a down market. We haven’t seen a lasting down market during our retirement yet (thank goodness!), so the real job of that part of our portfolio has been to just sit there and reassure us that we could weather an unforeseen market storm.

We originally set up our retirement portfolio with all ETF’s and we’re still happy with our fund choices and the diversity they provide. We’re especially happy that our average portfolio fees are very low at 0.04%, with individual fund fees ranging from 0.03% to 0.07%.

As a side note, some friends who invest in mutual funds instead of ETF’s explained their frustration last year about their mutual funds forcibly paying off dividends in their brokerage account which dropped their share value. They were able to reinvest the dividends to restore the total value of their mutual fund holdings but the dividends were taxable events which they didn’t need to live on but had to pay taxes on nonetheless. So choose carefully where you hold mutual funds if you need to closely manage your taxable income.

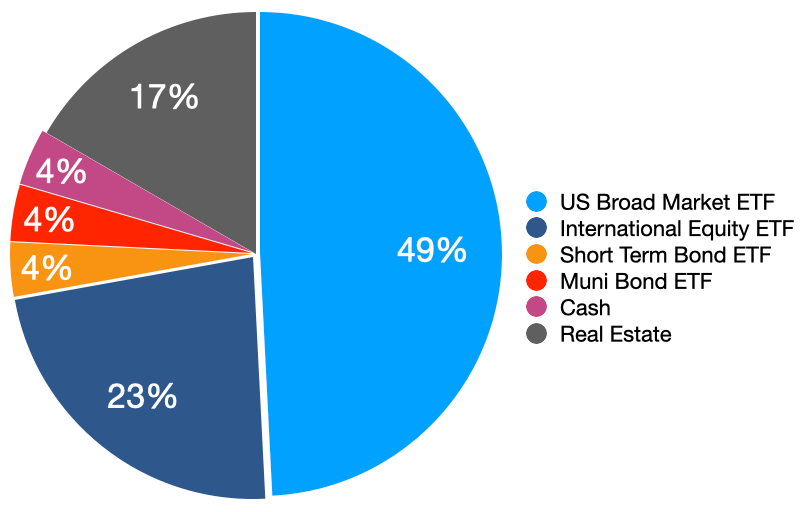

The main reason we’re in such a strong position at the moment is that we started our first year of retirement with 33x our living expenses, which gave us a 3% withdrawal rate. As of January 1, 2022 our budget is 11% higher and our total portfolio holds 45.83x of our newly elevated living expenses (not including the value of our home/real estate).

We aren’t confident that we’ve passed the hurdle of SORR yet, but after our big review we know we’re essentially there now. Since we still don’t have a crystal ball and we only have three years of retirement under our belts we’ve decided to remain conservative about SORR a bit longer. We’ll review our portfolio again for sequence risk next January and if we have another strong market year we might focus less on SORR after that. But we’ll probably give ourselves two more years before we consider changing our strategy for holding so much cash.

There’s no such thing as a one size fits all strategy for personal finance, so you do you!

Market Correction Anxiety

As I write this post the market is down and though it’s still January we know a lot of people are anxiously wondering if this year will bring that major longterm market drop we’ve been wondering about. Alison and I won’t allow that kind of fear to capture us because we know market corrections are not uncommon. Just looking at the market between 2000 and 2019 there was at least a 10% decline in the market in 11 of those years, which means significant market corrections in 55% of those years. That’s why we believe we’re due for a sizable market correction during our early retirement. Here’s how we’re looking at that possibility now…

If we see a market crash that causes our portfolio value to drop anywhere near to 25x our annual living expenses, whether that’s this year or any year before I reach age 60, we’d preemptively start making significant changes before we drop to 25x. We’d stop all major projects that cost money and reduce our spending budget to something back in the frugal range. And if we needed to we would look for part time jobs or side hustles to cover our living expenses in full or in part. That’s not a concrete plan but it’s a starting point.

To be more specific about the size of market correction that would cause a big problem for us we’ve outlined a sort of worst case scenario plan. Based on our current portfolio size if there was a 40% drop in the market over the next 2-3 years that would drop our portfolio down to only 27.5x our current living expenses, and red lights would be flashing. Definitely not the end of the world but since we waited to retire until we had 33x our old living expenses we see 27x as too risky for us. Since we’ve spent some time calculating how a significant crash would impact our portfolio I think we have our market correction anxiety under control for now, which is key if you’re going to self manage your portfolio.

Changes/Plans for 2022

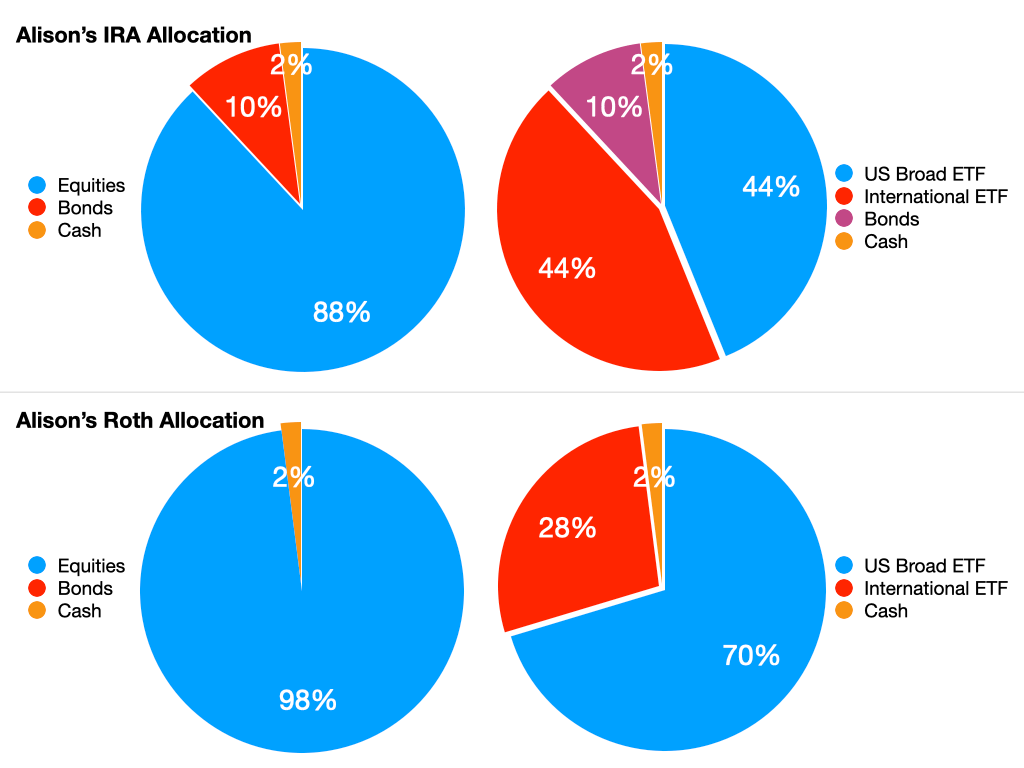

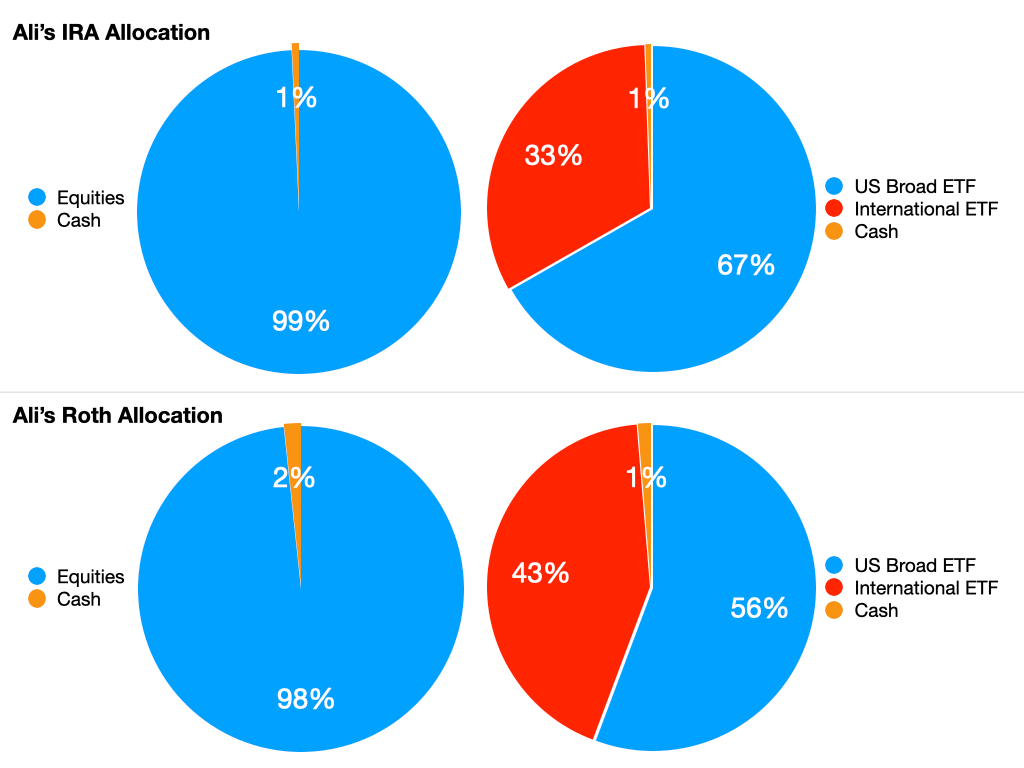

The only change we’ve made to our portfolio this year (so far) is in our allocation. As of now we’ve rebalanced to a new and more aggressive allocation of 80/20. We aren’t making that change because we’re suddenly less risk adverse but since we own real estate again we’re comfortable switching to 80/20 instead of 75/25 in our market investments.

Without our Compound, the idea of holding 80% equities seemed high to us. But we see our real estate like it’s one gigantic bond fund tipping our total portfolio allocation. And with that in mind our new 80/20 equity balance seems just right. Though to be clear, we would not be willing to sell our Compound in reaction to a major market drop, it’s just part of being comfortably diversified for now.

So far we have no other plans to make changes to our portfolio or our overall retirement strategy this year. We know the market is high even with the selloffs this month, and we might even be in the midst of a correction year. But we feel organized and prepared for whatever may come this year so we’ll stick to our PMS, keep learning, continue to pay attention to tax changes on the horizon, and try to control our normal concerns for market risk and our fear of running out of money some day. That’s right, we’re human too.

We don’t know what 2022 will bring in terms of the stock market, inflation, the Covid pandemic, or anything else. But we’re grateful we’ve started the year in a good place both financially and emotionally, and we’re excited about all of the plans and fun ideas we’ve set in motion for this year so far!

Very informative, Ali! Mark’s now 1 month from retirement and I’m 4.5 months out. So we need to learn about those HSAs.

LikeLiked by 2 people

Well, we will have lots to chat about when next we see you!!!!

LikeLike

Enjoyed reading this detailed post. I like how you do a portion of your Roth Conversions in January. For the first two years of early retirement we saved our conversions until December. But with the market downturn this January, we did a small 2022 conversion to lock it in at a lower $$ balance. I never thought much about doing it early in the year when balances are generally lower, but will probably consider that going forward. I am usually worried about breaking through a tax bracket, but doing half of a projected full year amount seems like a safe method.

Our accounts are mostly at Schwab as well. I didn’t realize they have Vanguard ETFs with no fees. Will have to keep that in mind for the future!

Dragon Guy

LikeLiked by 2 people

Hey Dragon Guy, thanks for commenting.

Every year we learn about more about the best way for us to do Roth conversions and we were pretty excited when it occurred to us that we should start with a portion in January. In our first year our entire conversion was done in December, in 2020 we started with a midyear conversion at an opportunistic time because of the Covid Crash, then we realized it would make sense to start in January. I’m already looking forward to the next fun idea out there!

And yes there are quite a lot of Vanguard funds available through Schwab. I do love Schwab!

LikeLike

Thanks for sharing detailed information about how withdrawing in retirement can work out. It’s helpful to have practical examples. Personal finance is personal, like you’ve said in many posts. I learned this year that I am more risk averse than I originally thought, and changed my asset allocation to reflect that.

LikeLiked by 1 person

Excellent! It’s all about finding enough data and examples out there to get you thinking about your goals and needs. Then you can design your own strategy and focus on what works best for you!

LikeLike

Thanks so much for sharing your portfolio allocations and withdrawal strategies in such detail! It’s always helpful to have more examples of how real people are doing this early retirement thing. I’m thrilled for you both that your first few years have only increased your multiples and made you feel more comfortable with the decisions you’ve made. Look forward to catching up with you sometime soon! Happy new year 🙂

LikeLiked by 1 person

Thanks friend! I think we started out in 2018 not really understanding what would make the most sense for our withdrawals because we couldn’t find enough examples. Learning by doing is a bit less fun when it’s money! But we were excited to try and talk about withdrawal strategies in more detail.

And congrats on hitting your FIRE number!!!

LikeLike

Such a great post! I read it aloud to the spouse. Thanks for sharing. We do much of the same – but we still have the vagabond life (kinda).

-Ellen (& Theo)

LikeLiked by 2 people

Hey Ellen! Thanks for commenting. It’s interesting/great to hear you two are doing some similar things. And it’s nice to know you’re still vagabonding (kinda). Isn’t it crazy how much things have changed in the past couple of years?! Eventually we’ll bump into you in real life I’m sure. We’re currently figuring out a new and different way to keep traveling ourselves (YAY!!).

We hope you two have a wonderful 2022!

LikeLike

Very nice and informative article

LikeLiked by 1 person

Thank you 🙂

LikeLike

Thanks for sharing your numbers and how you’ve pivoted and prepared for uncertain times. My favorite part of the post was your retirement account strategy: “Once our brokerage account was depleted Alison would be well over age 60 so we could switch to her IRA for our income needs until that account was also depleted. Then we would switch to my IRA once I was over 60 years old. But that’s not what we see happening now.”

LikeLiked by 1 person

So glad you enjoyed this post! We tried to learn everything we could before we retired. But there’s so much we couldn’t plan for in advance so our old strategy has to keep evolving to match what we’re actually doing now in retirement. We’re really enjoying learning as we go!

LikeLike