We are not certified professionals. For more information about us please read our Disclaimer.

Remember – Your Net Worth is Not Your Self Worth

We all have money baggage.

Knowing all of the intimate details of your own money can put you in a vulnerable place. And it can be exponentially more scary if you’re in a relationship, because you are exposing all of your fears to someone else. We worry about what other people will think about us if we confess we have big consumer debt. It’s also hard to confess if we leased that sweet car parked in the driveway because we were showing off a bit, but couldn’t really afford the downpayment. And it’s also stressful and frightening if we have more money than someone else and worry they will think that means life is not a struggle for us in other ways. Many aspects of money are fraught with judgement, or with our needs for status or ego, or used as a measuring stick against someone else’s standards of success. People worry about whether they have the right job, or if your job pays more or less than your friend’s job, or if you can’t afford to pay for college. Money can seem like a barometer exposing our sense of personal inadequacies to the world.

My Money Baggage

I grew up with a very quiet CPA dad. He did not like to talk to us about money, but he would talk about money with us kids if my mom encouraged him. Whenever he did talk to us about money he would say, “now don’t talk to anyone else about this.” In other words, this conversation is a SECRET! I grew up thinking that money was a private topic you would only discuss when it was really important, like when someone died. The message was that it was not polite to talk about money. I don’t know if that was because money was something my dad felt bad about or ashamed of, and I didn’t ask for clarification. I do know my dad felt judged by his parents because they didn’t think he was successful. His survival technique during visits with his parents was to stay quiet. Heartbreakingly, I can remember one visit when it only took my grandparents 45 minutes to let my dad know all their judgments and criticisms of him and his job. His discomfort was palpable.

After I grew up and started making my own way in the world, I learned more of the money stories in my family. I found out about the uncle that ran off with money from a family member’s store, disappeared for years, and left that family company in terrible shape. Later that same uncle worked overseas, made some not-so-good investments, and was supported financially by his son at the end of his life. And then there was my Papa (my dad’s father), who was one of 12 kids. He rode the railroads from Georgia to California with not much more than the shirt on his back in the 1920s. Then he started an auto body shop with my grandmother that supported them and some extended family, and even allowed them to retire on a golf course with a modest retirement nest egg.

Over time I also learned more about my aunt who was an inspiring novelist starting in the 1960s. She would teach English at a university one year and save as much as she could, then take the following year off to write. In time she was published but never made a ton of money. Her side gig was loaning the money she inherited from her two grandmothers to members of her small community. She helped people buy their first homes and start small businesses. And occasionally she made emergency loans to folks so they could pay their property taxes or monthly bills just so they could make it to the next month. Her loan business made her more money than it lost for her, and even though she asked me to run it and close it out for her after her death she really avoided talking to me about it until a month before she died.

Why Couldn’t We Talk About Money?

My close relatives all had their own experiences with money, but no one ever sat me down and said, “I’m going to teach you about money.” If they had done that of course many of their lessons would have been skewed by their own personal experiences, class, judgements, and beliefs, but that’s exactly the introduction I needed.

My aunt and my dad are both gone now, and my grandparents are all long gone, so I won’t be able to learn more than I already have from them about their financial experiences. But with hindsight and a mom that is a natural family historian and story teller, I can still learn some new lessons and carry them with me. My aunt created a career path for herself that allowed her to focus on her passions and become a novelist. She did make her dreams come true. And my hobo Papa created a business that set his family up to find their own successes in the world. I know I could have learned more from my family elders if I had only asked more questions, but I didn’t because I was taught that money is private. I wish I had the chance to learn more from my dad and my aunt about the options they had and the choices they made, along with their personal money values and priorities. Truth be told, my aunt was a little scary to talk to. But from now on, I will talk about money with the people I care about.

I can see now how starved I was for information about money when I was a younger person. This is one of the main reasons now that I want to have conversations about money with everyone we know and care about. I want all of my friends and family to know that money is not a measure of your self worth. It really is a tool to make your hopes and dreams come true.

Keep Your Net Worth Separate From Your Self Worth

Ali and I talk about our money in real dollars and cents. We were able to do that from day one of our relationship, and we believe that’s one of the secrets to our success in our relationship after 15 years together. We shared all the in’s and out’s of every account we had, every asset we had, and also every credit card balance or loan we had. We carried that openness about money through the new debts and assets we took on together, and when we had mortgages we talked a lot about how much the balances were and how much interest we were paying a year. It took us years and lot’s of effort to get to the point where we didn’t always bring our baggage to our money conversations, but we got there by making space for each other’s fears and old beliefs. Today, we have shared goals and values. And we know the more we check in with each other about our progress in our new life as FIRE’ed world nomads, the more on-track we will continue to become.

Money is a Tool

So what’s the point of this post? Twofold I suppose. First, it took me a long time to learn that money is a tool that can help us make our dreams come true. I also learned that money can be like an open flame and if you aren’t careful you can get burned. But with some careful management, money can do amazing things for us. Second, the amount of money you have has nothing to do with whether you are a good or successful human being. Your self worth has nothing to do with your net worth.

Money is just a tool. And you can be a good person no matter what the balance is in your bank account. Period. I know money can be scary. I know a lot of people judge us based on how much money we have or don’t have, what job we have or don’t have, how nice our home is or if we rent instead of own, and so on. But that’s just them, it’s not us. What’s amazing is that every person gets to be the steward of their own life, their dreams and money. After all, money is just a tool. So let’s put it to work!

Where to Start? Calculate Your Net Worth!

What is net worth any way and why should I know what mine is?

Knowing your net worth is like finding the “you are here” spot on a map. Once you are oriented with this bit of your financial information, tackling bigger financial questions or challenges becomes easier. Having your bigger picture clear in front of you will help you determine your priorities. Knowing your net worth is a step towards making your hopes and dreams come true.

No matter where you think you are on the financial spectrum, whether you are racing to catch up or way out in front of the pack, the best way to get a handle on your money is to start with understanding your net worth. It wasn’t until I brought all the elements of our net worth together, all of our assets minus all of our debts, that I really got the full picture of how we were actually doing with our money. The size of your loans and how much you’re contributing to your 401k are two very different aspects of your money, and it’s true that they do tug and pull on each other just like a teeter-totter. The less you are weighed down by debt the more your net worth can rise.

No Money Judgement

The process of looking at your net worth can be scary. One thing that Ali and I did during this process was to repeatedly say to each other, “there is no judgement” during the process. When we put it all on the table we had some student loan debt, car loan debt, credit card debt, gifted money from grandparents, a mortgage under water, a stagnant career path, and a more competitive career path. Whenever we felt like we identified a bad financial choice that resulted in some kind of debt we had to deal with, we had to give ourselves credit for pulling the blinders off and adding that to our net worth. It was a process of gathering facts, data, and information. No more and no less, and no judgement! See our Visualizing Your Money post where we talk about our money decisions timeline graphic.

Step 1 – Make Two Lists

Just like the Vietnamese woman pictured above, we had to fill two baskets to build the picture of our net worth. The first basket holds all of our assets, and the second one holds all of our debt. This first step doesn’t have to be any more complicated than that. You just need to create two simple lists. One with the assets and accounts that add to your net worth, and another with the loans and credit card balances that reduce your net worth.

You can create your two lists with only the individual items named and their corresponding balances. You don’t have to add up all the things you own in your home. Just start with the big accounts or items. If you want to add in more detail later you can. For now, you don’t need to add them up yet, just make the lists because for most of us that’s enough of a task. Then stop and take a break. You can go for a walk, or take a hot bath, or take a nap, or ask someone for a hug. Because building those two lists is a big accomplishment. When we went through this process together we needed a break after we made our lists!

Step 2 – Do the Math

The second step is to add everything up in your two lists, by totaling your assets and your debts into a single number.

Assets – debt = net worth

If there is more debt than assets, the result is a negative net worth. Conversely, if the assets outweigh the debt, the net worth will be positive. The higher your net worth is, the more easily your money can work for you. And the higher your net worth is, the more you can avoid consumer debt, the better your credit rate becomes, and the lower your interest rates will be for things like a mortgage. With a higher net worth you can weather financial challenges more easily. You can also build an emergency fund (check out our Pools of Possibilities blog post on emergency funds) more quickly for obstacles that come your way, such as needing to replace a leaky roof or wanting to quit a job and then take some time to look for a better one.

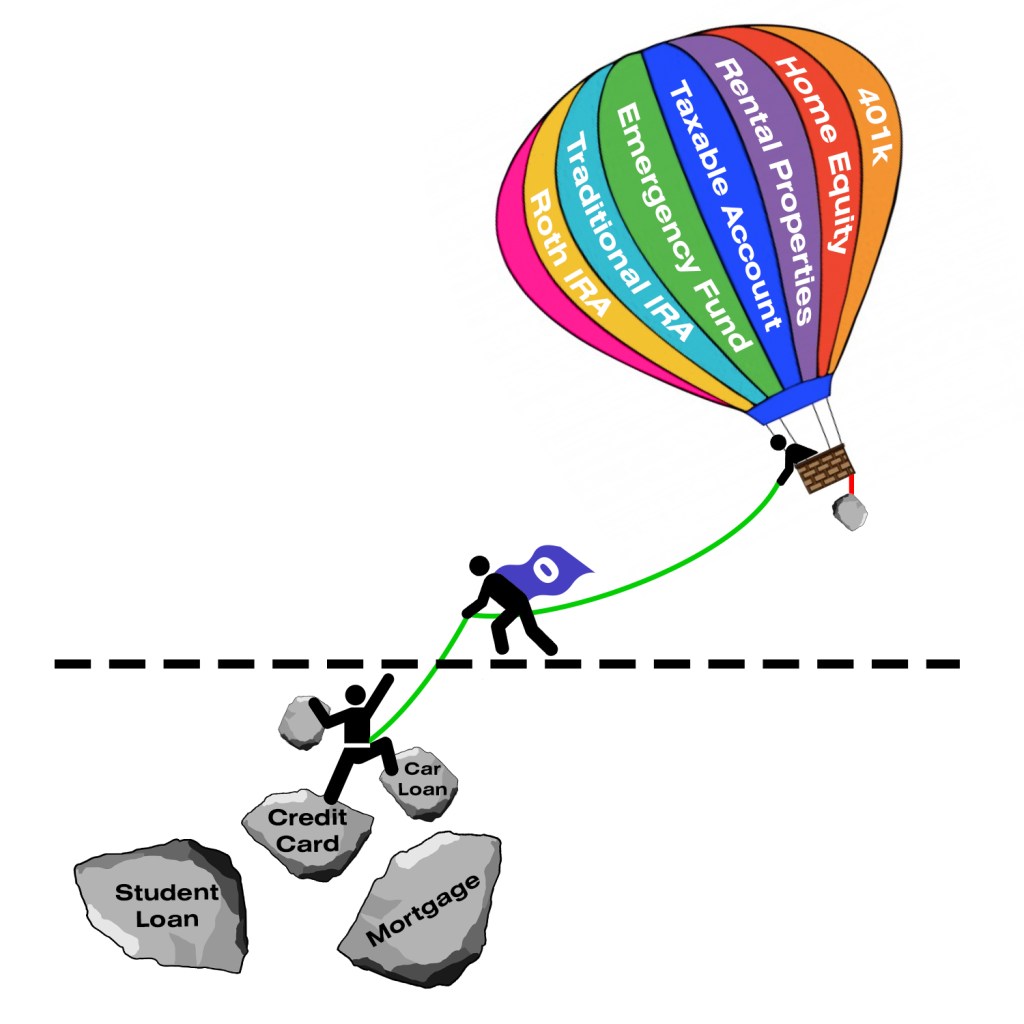

My Heroes are Zero Heroes

When it comes to paying off debt and increasing your net worth, if you have zero debt you can jump up to the “zero” line and be on your way to accumulation! And as you pay off more and more debt, you get closer to being a Zero Hero. In terms of debt reduction it is NOT a slight to be a “zero.” It’s an amazing accomplishment! One thing I am most enjoying right now is coaching my friends and family through debt reduction and reaching “zero.” I love to celebrate other peoples’s Zero Hero moments, and share in the excitement and joy people experience when they pay off their student loan debt or mortgage debt for example.

Once You Know Your Net Worth…

So that’s it – now go put your lists together and find out what your net worth is. Knowing your net worth is a momentous hurdle that many people are afraid to uncover. But you can do it, and once you do the path forward will become more clear!

Additionally, there are sites that offer budgeting and retirement planning tools that will be helpful in calculating your net worth and help you along the way to the next step, which is making a Personal Money Statement (check out our PMS blog post, haha). Your PMS document will help you plan for reaching your hopes and dreams. I encourage people who are going through this process to consider signing up for a free account on an aggregator site like Mint or Personal Capital. Of course you can do the calculation by hand but at some point you might find it less stressful to have this tracking done automatically. Personally, I find Personal Capital to be incredibly useful for tracking our net worth.

Blog posts we have written relating to building a financial plan

Hi Alison,

I understand what you’re saying about your Dad not offering a money education but sometimes it’s better

they say nothing and do no harm than talk and send you in a not so great direction. Mine used to influence

me considerably growing up on car ownership, a mantra he still follows today in his mid 70’s as he blasts through his mothers inheritance on his latest new 4 wheel depreciation drain.

Since that day I figured out that cars were pretty much obliterating my net worth more than anything else I’ve

been back with him to see if he fancied a revisit about his opinion and to also ask about why he’s never invested in income-producing stocks or assets. I wasn’t gloating my knowledge though, just curious.

The response? He would never invest in any of those because he doesn’t want to lose money…

You couldn’t make it up..

Have fun in Japan!

DN

LikeLiked by 2 people

You are pretty patient and forgiving of your dad when it comes down to it! We hate hearing how hard he is on you. The cars thing is kind of funny though. It does sound like he is at least giving you a good lesson in what not to do!

Enjoy your cold weather at home. We are looking forward to hearing how it goes when you hit the road again!

~Ali

LikeLiked by 1 person

My dad loved all things money. He was good at managing it and made some good commercial real estate investments in the early ’80’s that 100% covered my parents retirement when dad was run out of the savings and loan industry at 55yo. He FIRE’d at 55 but not by choice. Then he had a stroke at 58 and couldn’t run their money anymore. I just wish he had been talking to me about that all along the way. Now that he’s gone, I help mom manage her money. Dad did a great job setting her up and all I have to do are make slight adjustments for her.

I want to encourage folks to talk to each other about money. I love that you share your experience in dividend investments. And I appreciate your DIY message. Thank you for your encouragement on this topic!

Alison

LikeLike

I totally relate to this as money was also not something talked about in our house either growing up. It’s really been about self discovery for me, including lots of mistakes. I’m determined to share more with my kids. Ultimately they can decide what to take on board or not but at least they won’t be starting from scratch. Great blog post and love your writing style. Thanks for sharing

LikeLiked by 2 people

Thanks for all your comments and feedback. It sounds like your kids are going to have a great start with your help. I’m new to blogging and can tell how much of my life experience is influenced by my upbringing. And I find I really want to mentor rather than stand on a soap box or appear to be an expert. My wife and I like to say “its just us,” warts and all.

My real financial education came much later. And I sure don’t know everything but am so curious about money and love to have conversations with friends and family. Most of my posts are inspired by conversations we’ve had so I appreciate the chance to expand on a topic a bit.

Thanks again.

LikeLiked by 1 person

The hot air balloon graphic is great! It really does feel like rock climbing to get back to being a zero hero. It’s great that a rock is included on the hot air balloon. In my case, that rock is a mortgage. It makes more sense to grow the balloon than eliminate that rock to prevent tying too much of the portfolio to a single real estate property.

LikeLiked by 1 person

And your money might grow faster if you add it to what will really “lift” your net worth. Additionally, if your mortgage rate is low you could do better by investing in other places. Having money tied up in an illiquid asset is a very personal choice. But if you are down to just a mortgage, congratulations!

LikeLike