When we decided to retire early we took the opportunity to look closely at our housing options moving forward. We took a deep dive into both our personal needs regarding a home of our own, and also into what we could afford on our retirement budget. What we discovered about ourselves and our new retirement mindset was surprising. Going through that process helped us design clear parameters for our housing choices moving forward.

It became clear to us during that planning process that when we make decisions about housing, there are two main aspects to fully consider — emotional and financial. Most people have an emotional attachment to their home, and for many people their home actually feeds their sense of self worth. Our home also impacts our ability to feel grounded as well as our sense of being safe.

Understanding what you personally get from your sense of home and how that might link to your health and happiness is liberating. Having that emotional element figured out can also make it easier to understand how your sense of home can affect your housing budget. As social beings we want a home we can use for sharing time with family and friends. Many people also want a home they can feel proud of which might add an emotional attachment to the look of your home, even at the expense of your financial wellbeing.

Last year we sold our personal residence. It was a place we truly loved, but we decided to put the proceeds to work in our index fund investments which allowed us to quit our jobs. We wanted to stop working, and to stop working we had to sell our home. That process included separating our home from our ideas about quality of life and from our personal sense of happiness. One year later we are still glad we made that decision. At this point in our lives we don’t need a home of our own to be happy, because for us right now our sense of home is not the same as our housing.

What is Home?

As I write this, I’ve just come back from walking Brassy the dog since we are pet sitting for a month in Boquete, Panama. I’m out on the patio drinking a cup of coffee made from local beans and typing away on this post with a view of the backyard, feeling the breeze that blows up the valley from the Pacific. The sun has been up for about an hour, the birds are singing, and the hummingbirds are swarming the feeders. Soon I’ll make scones from a recipe I found in Scotland when we were traveling there with my mom last summer. Ali and I have a routine here in this house that revolves in large part around Brassy and her needs as well as our own habits. We each have our favorite spots to work or read in. We each enjoy doing our favorite household chores here. We feel grounded and happy. And we’ll be leaving this house in 2 weeks. For us this is Home right now.

In the Beginning

Ali and I are both originally from California. We grew up in different parts of the state and lived there until we were each in our 20s. Once California stopped feeling like home we both found our own ways to Seattle a decade apart. I moved to Seattle because it was close to where my favorite aunt lived and I wanted to be close to her. Ali moved to Seattle because she was ready to move away from her childhood home and once she found her dream job they gave her the opportunity to move and continue to thrive in her role in a new location.

When we met we were both focused on our careers and entrenched in the ideas of what we “should” do to achieve the American Dream and keep up with the accomplishments of our friends and family. For us that meant we had to have good jobs, be in a supportive and loving relationship, own a nice home in a good community, climb the ladder at work, buy a weekend home, and travel. We were determined to do it all. Luckily, we were also determined to save every penny we could and invest as much as possible in our retirement accounts, otherwise we wouldn’t be where we are today.

After 14 years together we had gotten a couple of promotions, bought our condo and paid it off, owned and sold a weekend home, and lost interest in climbing the ladder at work and in comparing ourselves with others. We felt exhausted, stressed out, and unsatisfied. During our last 5 years in Seattle we also took three trips to Europe. Those vacations were an excellent getaway from our intense lives in Seattle and increased our happiness, but those trips weren’t frequent enough to be the change we needed.

When is it Time to Move?

We’ve all played that game, “What would you do if you won the Lotto?” We had fun playing that game to make sure there were no rules when we brainstormed our dream life after retirement. Once we decided to sell our condo we wanted to map out as many new ideas as possible for where we might go next. Once again we turned to our family mantra, All Options Considered, and went back to the white board.

In that moment we didn’t consider buying a new home since our FIRE number was dependent on selling our condo and investing that money. One option we considered was renting somewhere other than Seattle but still within Washington State with a lower cost of living, such as Vancouver or Port Angeles. We also considered moving to a different state with a lower cost of living since we had friends that had done that including our buddy Fred who moved from Seattle to Arkansas, and our friends Kay and George who moved from Seattle to Missouri. The third option we talked about was NOT picking one new place to live, and instead traveling full time.

The idea of full time travel seemed the most far fetched but it came together pretty easily because we had a lot of inspiration to work with. We had been gathering travel ideas for our next vacation from folks who traveled full time themselves including Debbie and Michael from the Senior Nomads, Kristy and Bryce from the Millennial Revolution, Billy and Akaisha from Retire Early Lifestyle, and Jeremy and Winnie from Go Curry Cracker. Ironically, around that same time one of our condo friends Deborah handed us a book she had just read called “Home Sweet Anywhere” by Lynne Martin, which tells the story of a couple who was traveling full time. And in a flash we had a new focus.

Pretty quickly we decided to hit the road as renters living all over the world. Ali started researching and building itineraries in different regions, and I started crunching the numbers to build our new budget. By the time we were ready to sell our amazing little condo and leave Seattle we had a solid plan in place for living home-free.

Becoming Home-Free

There were clear emotional reasons that motivated us to make such a drastic change away from living in the condo we owned in Seattle to living home-free. As we reexamined our housing needs we acknowledged that our lifestyle in Seattle included feelings of status and ego based on our condo and its location in the South Lake Union neighborhood surrounded by the amazon.com headquarters. We also acknowledged to one another how we felt while living in our condo about trying to keep up with our friends in terms of their homes and financial choices when we really couldn’t afford to mimic them. Realizing those things motivated us to make a big change and shed our old ideas about what we “should” be doing. We asked each other what we wanted for ourselves, and in the process we figured out what our values are for housing at this time in our lives.

In the past I was interested in living in a set location for various reasons such as:

- I wanted to live near family

- I had a pet

- I had a job

- I was afraid to move away from what was familiar

- I owned a house and I wanted to keep it

- I had friends and a community I was deeply connected to

My current preference for living home-free works for me because:

- I don’t have a job

- I don’t have a pet

- I have very few belongings

- I don’t have a house to maintain

- My relationships with family and friends can endure being separated by distance and time

- My wife and I both enjoy exploring a new location, culture, and climate every few months

Right now, this is what home means to us (we can do this anywhere):

- Being anywhere together

- Being able to cook for ourselves

- Getting outside everyday to explore our surroundings

- Spending time online and in real life with new friends, old friends, and family

- Showing up in person when friends and family need us

- Learning about the history, culture, and people around us

This year I’ve learned how to feel grounded no matter where we are, which is partly because my sense of home is fulfilled. My life is finally focused on my relationships and personal connections.

Housing Costs

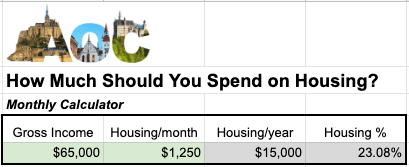

Housing is expensive, and for most families it’s the single most expensive part of their budget. For some context, according to the US Department of Housing and Urban Development (HUD) paying more than 30% of a family’s income on housing creates a cost burden that could make it difficult to pay for things like food and medical care. HUD estimates 12 million US households are spending over 50% of their incomes on housing.

My dad used to say we should keep our housing costs at 25% or less than our total budget, which seemed like a good baseline for “All In” renting or buying. In 2009 we bought our condo in Seattle and at that time we were spending 30% of our income on housing. Amazingly, if we were still living in our condo today we would be paying almost 30% of our retirement income on housing with just HOAs, taxes, insurance, and utilities combined, and our mortgage paid off. After a year as home-free travelers we are on target to spend about 23% of our post-FIRE income on housing while we are traveling full time in 2019, and that works great for us right now.

Remember, it doesn’t help to start with judgements like buying a home is a bad investment, or renting a home is throwing money away. Your housing decisions are your own, and they are deeply personal.

Do Your Own Math

I’ve been working on several calculators to both track and compare the costs associated with each of our housing choices – rent, home-free, and buy. The link to my Rent vs Buy spreadsheet with those calculators is included here. Feel free to download, make a copy, and enter your REAL numbers so you can build out a dream that works with your personal budget and hopefully meets your emotional needs as well.

Rent vs Home-Free vs Buy

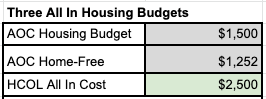

In most cases housing starts with the question, “Should we rent or should we buy?” When we explored that question last year the obvious answer for us was to rent, but not in the traditional sense since we decided we wanted to travel for the foreseeable future. We took the typical Rent vs Buy equation and added a new category called “Home-Free” which is a modified version of renting. Each of these three categories comes with a different budget based on its permanence in our lives.

Renting

For me renting means not having 100% control over the four walls we’re living in. If you’re someone who walks into a place and immediately starts thinking about tearing out a wall or remodeling the kitchen or bathroom, renting can be a challenge. There are major advantages to renting though, because it comes with a lot of other types of freedom such as lower maintenance and the ability to change locations more easily. I can get a shorter lease or a longer lease, and find a rental price that suits me and our budget. And if we’re not happy with our place we can move.

Ali and I were each renting when we met, and then we decided to buy a 1,700 sq ft home together at the northern edge of Seattle. When that house and location didn’t fit us anymore we decided to downsize away from that three bedroom home and start minimizing our lives. We moved into a 750 sq ft apartment in walking distance from my office and a short bus ride to Ali’s office. We had all the space we needed and the freedom to close the door and take off for the weekend. We enjoyed renting because if the water pipes froze and broke while we were gone, the property manager had to deal with it. We didn’t have to mow the lawn, trim the hedges, fix the roof, repair the shower, or have any trees cut down. We were happy to clean the floors, kitchen, and bathroom, and be done. We loved it.

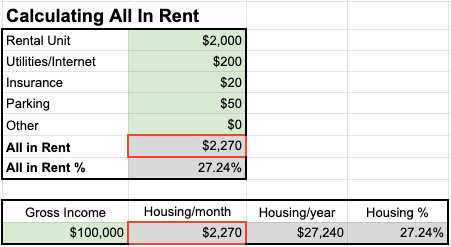

We chose our rental based on our budget and proximity to work. Our “All In” rent number included the actual rent, our rental insurance, and utilities. Renting that place cut our commutes way down, saved us a ton of money, and improved our quality of life for sure. Once in a while one of our neighbors was noisy but we didn’t mind too much since we could move if we didn’t like it there anymore. We were happy to give up the feeling of having total control over our home so we could have control over our location, and even more control over our budget. It was liberating.

Home-Free

In order to be home-free renters we had to get real with ourselves about our budget. Once we quit our jobs and decided to live off our investments, it cut our disposable income in half. That meant our housing situation had to change and we were 100% comfortable with that. Our new budget and housing situation needed to fit with our FIRE number and what our investments can generate in a year. Since this is our first year after FIRE and getting there was attached to selling our home, we were definitely not ready to commit to a new housing situation with permanence. We had the urge to create a life that felt more flexible and spontaneous, and with a lot more freedom so that’s how we ended up living home-free in 2019.

Right now we don’t have a home base and we move every 1-6 weeks. Sometimes we move from one city to another in the same country, sometimes we move from one home to another in the same town, and other times we move from one country to another. We’ve been doing this for 14 months now, and we love it! Living home-free gives us a huge amount of control over our housing budget. Every location has it’s own cost of living, and we can choose to upgrade or downgrade on costs as we move from one location to another, and create balance by staying in different kinds of places. We can even drop our housing expenses down to zero for some periods by housesitting here and there as opportunities arise.

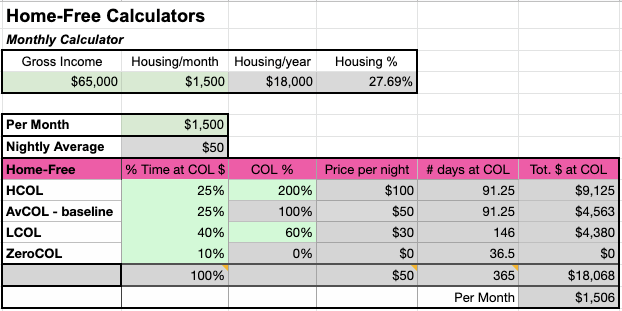

We still have a set budget for home-free housing during the year, and it’s critical that we meet it. Our all in home-free housing costs are really just the total costs of our stays in the apartments and hotels we rent, plus the annual membership fee of $119 that we pay to TrustedHousesitters. Our housing budget is $50 per night, or about $18,000 for the year. Our housing costs are the most critical element in our overall budget followed by healthcare, food, and transportation. As home-free renters Ali and I choose an area we want to visit and then the next step is to look for housesits that might fit, since that often requires us to adjust our travel dates to fit those arrangements. We fill in the gaps around housesits with apartment rentals, and then for shorter stays we look at hotels. We also travel back to the US to stay with family a couple times a year. All of those housing options and their wildly ranging costs just need to average out to hit our yearly housing budget. As of today we are on target to keep our 2019 housing costs at 23% of our total budget. We are under our housing budget for the year, and we’re thrilled to see our home-free plan is working.

Geoliberated. Our buddies John and David over at The Debt Free Guys and the Queer Money Podcast call their home-free lifestyle being geoliberated. We love that term and we whole heartedly agree with the philosophy. By not locking ourselves into a set housing payment for the year we can modify our housing costs each week and month, which frees up some cash for other things, like attending a Chautauqua retreat in Ecuador or taking Spanish lessons in Boquete, Panama.

Buying

Before buying it’s helpful to understand why you want to purchase a home since buying a personal residence is often more of an emotional choice rather than a practical one. In our case we have owned three homes together and in each case we had a really hard time figuring out the emotional aspects of purchasing or selling those places. Though we tried to convince ourselves that we were being wise and practical about our financial decisions for each of those homes, we definitely learned that our home ownership choices have been emotional and deeply personal. And everyone knows choices made from an emotional place don’t always neatly fit into budgets or support your financial health.

People often tell themselves buying a home is also an investment, and in some cases that can be true. But it can be hard to make a real profit when selling a personal residence, partly because of all of the maintenance costs for a home and also because you can’t control how locations change and real estate cycles go up and down over time. In our case two of our homes were money pits, but our condo did turn out to be a good investment. Regardless, from my perspective it doesn’t usually make sense to think of a personal residence as an investment since the decision to buy a home is so emotional.

Buying a home can theoretically be a stable housing expense since there are fixed numbers to work with. Once you set the purchase price for a home along with your down payment, that helps you calculate your monthly mortgage payments. We had a budget for the first house we bought together, but we definitely did not have a realistic understanding of our “All In” costs for that home which included the closing costs, our mortgage payment, home owner’s insurance, property taxes, utilities, and a heck of a lot more in maintenance costs than we could have imagined. We weren’t prepared for the bad seal in the shower that required a massive fix before selling. We also weren’t prepared for the winter storm that brought down a huge cedar tree and smashed our fence and our neighbor’s hedges. We had to hire someone to come cut the tree into pieces and remove it just so we could get our cars out of the driveways (thank goodness the tree didn’t hit our house or our neighbor’s house). By the time we were ready to sell we also had another set of real estate fees and closing costs to pay to let that place go.

When we bought our condo the costs that changed over time were our taxes, utilities, insurance, home maintenance costs, and also our HOAs which were increasing over time. Those are the types of things you have to include to get your “all in” housing number in order to stick to your budget when you buy a home. No matter how fixed your home ownership plan is, there will always be new and ongoing expenses when owning a home. The increasing HOA fees were the biggest surprise there and I’m still kind of shocked today knowing that our all in costs for our condo were at 30% of our current retirement income even with the mortgage completely paid off. In a way, you can become your own landlord as a home owner, but even in that case you still have to pay some kind of housing costs. If we decided to buy again we will definitely have a more complete budget for all in housing costs to work with.

The other aspect that’s often overlooked when selling is that it can sometimes take a while to find the right buyer. When a home sale drags on for more than a couple of weeks there could potentially be unexpected expenses you didn’t originally include in the equation of selling. We staged and moved out then listed our condo for sale November 1st, 2018 but it didn’t close until mid January 2019. This meant we had to arrange for other housing until we left Seattle for good. Additionally, having the sale carry over until January meant we had to arrange to sign the closing documents online since we were in Singapore when it finally closed. Thankfully this time, we had prepared for both variables and had planned for it in our budget for selling the condo.

Housing Money Crush

Someday we will probably want to stop traveling full time, and when that happens we will stick to our new process of focusing on the two most important aspects of choosing were we want to live by looking at our emotional needs and our budget. In fact, writing this post made me consider renting and it also made me consider buying again back in the US, which is why it took me so long to write this post! But after reviewing all of our options we are excited to spend next year living home-free again. When we settle down somewhere more permanent we will make sure we understand the emotional aspects of our housing needs at that point in our lives, and set a real budget that fits our financial resources as well as our personal goals.

Housing Emotions

When we decided we were ready to let go of our emotional attachment to our condo in Seattle, the whole world opened up to us. When looking at housing it’s important to make sure you prioritize what’s important in the moment and also think about how that might impact your options in the future. In our case, we know what we want right now and we acknowledge that could change at anytime. In your case you might ask yourself if you are moving to a new home for a job, or because your family is growing, or because you want to be closer to family? Are you downsizing to help facilitate other financial goals like retirement? Are you fulfilling a longterm dream to build your own home from the ground up on land you picked out with an amazing view that you love? It doesn’t matter what your specific emotional needs are around your housing choices, it only matters that you are open and honest with yourself about what your housing needs are.

Housing Budget

We love our current home-free life, but we will keep talking about the idea of living in one location and what our housing needs might be at that time. At this point whenever we discuss our hopes and dreams we consider whether we want to continue to be home-free, or whether we want a more traditional rent or buy scenario. We have budget plans for each one of those options, because I love to play Money Crush and because we want to be free to change our minds whenever we are ready. Knowing those budgets helps us look into the future as we set our 1-year, 3-year, and 5-year plans. It helps us dream more openly and be realistic about our budget. And we acknowledge that if it doesn’t work in our budget that would put too much emotional strain on us and we know we would have to start the planning process all over again.

If we decide to rent in one location, we will have regular payments that could increase each time we sign a new lease, as well as utilities, and renters insurance. If we choose to continue living home-free, we have to actively make choices regarding location and duration of stay that fit within our annual housing budget. If we decide to buy another home we know there will be a big cash outlay to make that happen, which will have a huge impact on our investments. If we can buy without a mortgage we know there will be continued costs associated with maintenance, taxes, insurance, and utilities. We also know that home would appreciate in value based on its location, which can be hugely variable. And we know there could be lost opportunity costs with the money we commit to personal real estate verses other types of investments. There’s a lot to consider!

There’s No Place Like Home

For now, Ali and I are having a great time being home-free. We think we’re going to be doing this for 3-5 years at this point and we have the first year basically completed as I write this. But things could change at any time. When we dream about settling down somewhere we often talk about the idea of going back to the Pacific Northwest. And when we think about the kind of home we want there are a bunch of scenarios we keep considering, which range from a fixer-upper to a small modular place. We also talk about having a tiny home on land with enough space to live communally with friends. No matter what we choose we would love to have room to spend time in our home with family and friends.

Now ask yourself: How did you decide to live where you live right now? Do you put more emphasis on buying over renting or vice versa? Did you really consider your emotional needs for housing and how they impact your budget? Do you think your housing needs might change in the future?

Here’s one more easy to find link to my Home-Free vs Rent vs Buy spreadsheet.

Lastly, here are a few other ideas I want to share…

- The NYT Rent vs Buy calculator

- The mortgage calculators I like

- A few of the housing related blog posts I like:

The end, for now.

We are not certified professionals. For more information about us please read our Disclaimer.

Great post, thanks, Alison! You look at a very important question… Having a home is something I thought I could easily do without, but as we are getting closer and closer to our FIRE date, I have started to wonder if I am ready to let go of the comfort and convenience of having a more permanent base. On the other hand, as you mention, the cost of even just HOA fees could fund the better part of rent in a LCL country! Choices choices…

LikeLiked by 2 people

Thanks Valerie. Its so important to really understand your needs and wants when it comes to housing. Then be realistic with how that fits into you budget. Its an active question for us these days. Thankfully, we have the time and space to answer it. ~Best

LikeLike

Thanks for such a great post! I have been playing with some numbers in my head of whether to buy a condo just outside of NYC for retirement, but it is so hard to justify the costs since just taxes and HOA would be over $1000 a month …. and going up every year! Maybe we will just pet sit around the world instead!

LikeLiked by 2 people

Keep playing and running the numbers. You’ll know when and whats right for you. It will hit you like a flash. It did for us when we unlinked our happiness from our condo in Seattle. And now we don’t have to live in just one place. For now, this is amazing! Good luck!

LikeLike

Well without even running the numbers, my body is telling me that maybe we should have a permanent home in a warm, cheaper location, and just airbnb in new york in the summer if we want to visit family. I am planning on checking out warmer locations in two years, and your blog is very helpful!

LikeLiked by 1 person

Thanks! We for sure can tell we do better in slightly cooler places. For example, Panama City was WAY to hot and humid but Boquete is perfect! It cools down at night and doesn’t get much over 78 degrees most days. So we are much better her than in the humidity. And rents and services are much cheeper here. Not as cheep as other places but much better than say Seattle for sure.

LikeLike

Emotionally I am 100% a home base kind of person right now. With a kid and two dogs, I couldn’t begin to imagine wanting to be more nomadic! But that’s this season of life. I don’t know how I’ll feel fifteen years from now when we enter another phase of life, I’m keeping an open mind about that part.

While I’d like to count on money from selling the house, I have no idea what’s going to happen to this housing market between now and then nor do I want our plans to hinge on the value of this property when heck, a quake could swallow it up. (I am a pessimist!)

LikeLiked by 2 people

Sounds like you live on the west coast? We were looking at houses in some communities that are in Tsunami zones. I thought, “thats what insurance is for!” Since we are RNKNP (retired, no kids, no pets) we can be much more flexible. I have to say I do miss a garden and a workshop some times…….

LikeLike

[Hopefully I don’t post this twice – at least I copied my comment before risking the login, since WP seems to hate me lately!]

I lived in Portland for a long time, and then the Bay Area, and was thinking that I might like to try the life of doing lots of travel and working from the road. Then I was on a three-week trip and realized that I did NOT want to travel full-time; I wanted to find a way to get back to Portland.

At the same time, I had a friend starting to contemplate retirement, and as a life-long renter he knew he could either stay in the Bay Area and keep working, OR he could give up his home and quit work and travel/house-sit/be a nomad until he was eligible for social security. (And he did quit/traveled for 3 years, sort of what you two are doing, and is now back in a rental).

Between that story of retirement, and my knowledge I wanted to be back in Portland, I managed to move from California back to Portland and bought in 2013, just as prices were starting to come back up. I looked at a specific condo community, and at a few houses. In the end I went with a house – it had a higher list price but taxes were half compared to the condo, and the house has no HOAs. It was easy to see that once the mortgage was paid, the house would have lower carrying costs, better resale value, and more flexibility in terms of more space/no rules about renting. I determined my price cap and stayed under it; I found a house that is a one-mile walk from friends, has a nice little coffee shop/restaurant area nearby, has few steps (so good for aging in place), and is fairly solid. Sure, things could happen, but overall I’m set up pretty well.

I think I like the idea of being a nomad more than I might like the actuality – my longest trip has been 3 weeks and I feel pretty done by the end, but maybe I need more long-term stays rather than hopping around as I have tended to do. In any case, I’m on track to have my house paid off in 9 or fewer years and should have substantial retirement savings by then (you know..depending on the market).

Best-case scenario is that I’ll quit work in my mid-to-late-50s, pick up some kind of health coverage (another huge if/depends on how we are doing things by then), and be free to do what I want without owing 40 hours per week to an employer. Or maybe I’ll find a dream job and it won’t feel like a sacrifice to spend my time that way!

LikeLiked by 1 person

Sounds like your house is the right fit for you. And the area of Portland you are in sounds fun. We do much better when we slow way way down in our travels. We are finding that doing some Home-free travel is helping us keep our expenses down for the first few years of retirement which is a really good way to protect from some sequence of return risk. It sounds like you are on track!!!!!!

LikeLike

I’m glad I stumbled on to y’alls blog a couple months back. Both of you do such a good job of writing that are easy to read. I have two questions for you. How do you go about finding someone that needs a pet sitter? Do you happen to know of the family from Route to Retire that recently moved to Boquete for a year? If not you might hook up with them in your remaining two weeks.

LikeLiked by 1 person

Glad you found us! We use Trustedhousesitters.com. Do a search on the site for our house sitting post we did a while back. And YES, we have contacted that family. They are traveling away from Boquete right now but we might cross over for a few days around Christmas. Cheers!

LikeLike

Your article is so well written and carefully considered. I like the way you untangle the emotional and financial aspects of owning a home. Being able to articulate that complicated aspect of home ownership is a gift to all of us looking carefully at the choices we make with our living lifestyles and accommodations.

In my case, I sold my family home last year that had been in my family 50 years. An extraordinary home with plenty of land, centrally located and decades of memories. If I was financially independent I would have kept it for the emotional reasons but such was not the case.

There is something also to be said for living in a clutter-free living space where the mind is free to rest, roam and be unobstructed. I have a friend who loves to take business trips because when he enters a motel room there is only a bed, desk, tv and no other personal possessions to consume his thoughts. He equates it to a zen environment.

I moved to Vietnam and have lived here now over 7 years. It is not a panacea and the choice of city that one chooses to live in is VERY important when you consider the people, traffic and nowadays, particularly, the air quality index. Hanoi is now in the top 5 dirtiest air polluted cities in the world. And Saigon is also in the top 20. The cost of living here is SO much lower than the States that when I do go back I’m shocked at the prices of daily items. Ordering a pizza and soft drinks is around $30 plus. A good vegetarian meal in Vietnam is about $1.50. Here, almost everyone is a renter because it is made difficult by the government for foreigners to own land or houses.

But your article got me thinking about the benefits of not being tethered to just Vietnam but also to consider other locales throughout South East Asia. Thank you again for taking the time to share a complicated subject with all of us.

Sam

LikeLiked by 1 person

Hey Sam, Thanks for such a thoughtful comment. We also had a family home that we had to let go of several years back. It took me almost 10 years to realize it was time to let it go. But the process of doing that really started us on the concept of decoupling the emotion from the reality of our housing needs and budget. We feel so much freer to follow whats best for us. What city do you live in in Vietnam? How did you end up there? Keep us posted on other places you might consider next. We are in Boquete, Panama and would really consider coming back for a more extended stay (3 + months) ~Best, Alison

LikeLike

[…] For housing, I vacillate between my apartment (easy, default); moving in with my aunt in Maryland (cheapest); my family’s not so subtle suggestions that I move to Florida to be nearby for Aunty MERJ (most emotionally demanding); buying a home (less predictable); or moving to the Midwest (geo-arbitrage). There are none that really meet both my emotional and financial needs. […]

LikeLiked by 1 person

[…] In the Wannabe Retiree’s situation accessing their home equity is key to the success of their retirement plan. They have built and maintained some healthy equity in their home over time. Moving their home equity into passive index funds could produce enough income through price appreciation and dividends to more than cover their gap number. My calculations using their home equity moved them from only 10.7x their living expenses to an impressive 50x their living expenses gap number. Additionally, if they aren’t locked into their current home they will have more flexibility to move as their needs change over time. After all, a person’s home is more than just housing. […]

LikeLike

[…] Home is more than just housing (All Options Considered): I tweeted to AOC that what I liked about this post is the principal behind it, one I share, and that we both used it to come to different outcomes. I’m sick of housing being treated in pure financial terms, as if there is no more to it. It’s where you spend most of your non-work time! Whereas I bought a house to ensure a quiet place to rest and recover and do my thing, for AOC they decided on a more nomadic course. Read about their approach in this well-written post. […]

LikeLike

[…] 2019 was our first year of full-time travel. We started the year as complete rookies in our new travel lifestyle and we definitely learned a lot. It took time to learn how to slow down and figure out that we don’t need to see all the sites. We had to get familiar with our ever changing neighborhoods, figure out how to turn each new place into our home, and build a routine that we could adapt to any location so we could settle in and stay grounded. Everyday we looked around whatever place we were in and reminded ourselves that was where we lived for the moment. No matter where we are, we are at home. […]

LikeLike

[…] I’m excited that our first year of retirement and also our first year of full-time travels is in the books! This will sound very cliche, but wow 2019 just flew by! When we left January 3, 2019 from San Francisco to Singapore it felt like an overwhelming adventure had begun. Getting through the first few weeks of constantly switching to new environments was difficult. I definitely had moments where I was thinking, “What the hell are we doing?” And now a year later we are in San Miguel de Allende in Mexico and our lifestyle feels familiar and so much easier than anything else I’ve experienced as an adult. We’re having a blast being Home Free. […]

LikeLike

[…] If we decide to buy a home in the near future we would likely liquidate a significant portion of our brokerage account to give ourselves money for an all cash housing purchase. That would quicken the pace of emptying our brokerage account and require us to start tapping into other accounts sooner. Though we are also very open to the idea of renting or ongoing slow travel instead of owning a home again. Housing is for sure an area for us where All Options Are Considered. […]

LikeLike

[…] Related post: Home is More Than Just Housing […]

LikeLike

[…] us, home is more than just housing. It’s a very emotional and personal decision combined with a complex financial commitment. We […]

LikeLike

“How did you decide to live where you live right now? Do you put more emphasis on buying over renting or vice versa? Did you really consider your emotional needs for housing and how they impact your budget? Do you think your housing needs might change in the future?”

The decision for my current residence was to keep a minimal commute, keep housing costs reasonable while building equity, and be able to have a place of my own. Buying made more sense at the time due to low interest rates and rents were rising. The emotional needs definitely drove the decision, since I had great rent on the room I was staying in, but the time finally came that I felt I needed my own place to live a full life. My housing needs are likely to change greatly depending on if the dream of working abroad pans out or if I have children at some point.

The big question for housing later on is whether to rent out my current place or sell it when it is time to move on. There are a lot of variables that would go into this decision that are likely to be changing constantly, so All Options Considered will be the strategy when I reach that bridge 🙂

LikeLiked by 1 person

Bravo!!!!

LikeLike