We are not certified financial professionals. For more information about us please read our Disclaimer.

I must admit I haven’t had the mind for money blogging since the world got turned upside down with the global COVID-19 outbreak earlier this year. But now that we’ve settled into Flagstaff for at least three months and collected my mom from her retirement community in Tempe, I’m feeling much more grounded and ready to run off into the weeds playing Money Crush.

The topic of Roth conversions has been on my mind quite a bit lately. We aren’t active traders, we don’t have new sources of income to invest, and we aren’t trying to time the market when we do get into our portfolio. But we do want to pull the leavers that will improve the health and potential longterm growth of our portfolio. Our money management tasks during our early retirement years include making Roth conversions in addition to annual portfolio rebalancing.

In 2019 we built a plan to do annual Roth conversions to reduce our future tax obligations. Roth conversions are taxed at ordinary income rates and since our annual spending budget is well under the top of the 12% tax bracket plus our personal deduction, there’s room to move our pretax contributions over to our Roth accounts for some uninterrupted tax-free growth while our retirement sources of income (dividends, interest, and capital gains) are lower and highly fungible.

The other reason we’re looking at Roth conversions early in our retirement is so we can control the size and frequency of withdrawals from our IRAs. We don’t want to be compelled to take required minimum distributions (RMD) by the IRS after we turn 72 years old. Our original pretax contributions need to be taxed at some point, but I would rather not have it happen on someone else’s schedule. I want to be the one turning on and off the withdrawals on our accounts, based on our hopes and dreams and on our timeline. So in our situation, Roth conversions seem to be a great avenue for more control. Except that we also have to factor in the reality that our current nomad lifestyle is being impacted by the worldwide COVID-19 pandemic.

How so you might ask? When we realized we might be better off back in the US as countries around the globe started to close their borders to nomads like us, it hit us that our nomad lifestyle might be coming to an early end. We started to examine the spectrum of what could happen next, including returning to the US for good. And if that was the case, we would need to change our health insurance plan. If we need to be in the US full time then we probably need to be on the Affordable Care Act (ACA) or another type of American health insurance option. But if we do get an ACA health insurance plan our total income will be a big factor in our health care premiums.

One Lump or Two?

In 2019 I converted $62k from our IRAs to our Roths in one lump in early December. But at that time I still didn’t have an accurate idea of what our total dividend income would really look like by late December. In the end, I should have converted a bit less since we really pushed the limit on the 12% tax bracket when our dividend income and capital gains income ended up being higher than I had estimated.

After that lesson, my plan for 2020 was to convert a total of $60k to our Roths in two batches using our final actual income from 2019 as an estimate. In March of 2020 when the market was down and there was a lot of uncertainty about COVID-19 around the world, I did the first half of our Roth conversions. The down market netted us a conversion of more shares for the same target dollar value. And by only converting $30k, our total taxable income at that point would come in right under the ACA premium subsidy cliff. If we were just $1 over 400% of the poverty income level, our premiums could jump as much as $570 a month if we did need to get on the ACA in the next year. In December I plan to do one more Roth conversion of around the same amount, but we’ll be waiting for our final dividends and capital gains first.

Related post: Don’t Let Market Downturns Take You Down

To stay on top of the potential issues we might face with the ACA cliff we have plugged our numbers into the Washington Health Plan Finder site each year for the past three years, so we have a clear idea of what our premiums would be on the ACA when we return to living full time in the Seattle area again. We looked at the Kaiser Permanente “Core Bronze HSA – 20” plan and a $5,000 Individual / $10,000 Family deductible. For this plan, if our income is $67,600 we would have to pay $341.39 a month in premiums. But if our income is $67,700 the premium jumps up to $913.79 a month for the two of us. That’s a BIG difference proving that our income level is something to pay close attention to if we do get on the ACA.

Once I finished the $30k Roth conversion in March we paused. We needed to focus on what to do with our travel plans for the rest of 2020. We actually have to know how much we will be inside the USA because that has a huge impact on our health insurance needs. The first thing was to decide how to spend the summer since we knew we couldn’t travel to Ireland, Scotland, and England for the summer with my 81 year old mom as we had originally planned. As of this week we have been able to cancel all of our flights and car reservations for our summer trip, and all but one of our accommodations in Scotland. We might have to accept a zero cancelation policy for our month long stay in Scotland unfortunately. But sunk costs have a place in our budget and we feel lucky that’s the only part of our plans we might not be able to get refunded.

Related post: The Sunk Cost Fallacy, in Travel and in Life

Flagging Some Burning Questions

2019 was our first full year of retirement so we are still learning. We are trying not to over manage our portfolio or our day-to-day finances. Last month in June we had a midyear planning party here in Flagstaff. Even though we had just had a big planning party in April in Mexico, which we called our San Miguel Summit, we were ready for another one since things are constantly changing.

Related post: It’s April – Now What Are We Gonna Do?

We’ve been scheduling these planning meetings ever since our Seabrook Summit in 2017 because we believe talking about everything with your partner, especially money, is very important in a relationship. Our Seabrook Summit was when we started working on our Personal Money Statement. These planning parties are crucial to our ability to schedule and plan for the goals we care most about.

Related post: Outline Your Goals in a Personal Money Statement

This month’s planning session was complicated because it’s difficult to plan ahead with COVID-19 surging in the USA, and though it seems to have calmed down a bit in some other countries COVID is still active all over the world. If we stay in the USA longterm we want to avoid that darn ACA cliff. So we made a list of all of the important topics we needed to discuss, and noticed how similar it was to our agenda list back at the Seabrook Summit.

Insurance and Travel

The first topic on the agenda was insurance. Ali dug back into our current IMG international health plan and reminded us that we can only be in the USA for 180 days a year. That means we do have to find a way to get back out of the country for a couple more months this year so we don’t disqualify ourselves from our existing health insurance. We agreed that we both still have longterm desires to keep traveling, if at all possible, for more than 6 months a year for the foreseeable future. And if we can make that happen getting on the ACA is less of a concern right now. If we need to stay in the USA for the rest of the year though, we’ll lose our IMG health insurance and we’ll need to find something else very quickly so there’s no gap in our coverage.

Cash Has a Job

We also revisited the topic of emergency funds. Our current plan is to make sure we have at least three years of living expenses on hand and accessible for emergencies. Some of that is in a money market fund and some is in higher yielding CDs. And if we really get in a pinch, we can always access the other equities or bonds in our brokerage account.

Gathering Our Living Expense Cash

At the end of 2019 we set aside cash for our living expenses in our “current year savings account” to cover our total budgeted living expenses for 2020. Our budgeted living expenses are $65,000. The first bit of that cash was our little surplus of leftover cash from 2019 since we didn’t fully deplete our living expenses last year. The next chunk of cash for this year came from a CD that was set to become available in December of 2019 for the purposes of 2020 cash. And the rest of our cash came from dividends in 2019.

We also really needed to clarify our plan and process for exactly how we expect to gather our living expense cash for the next few years. If the market is up at the end of each year when we accumulate these funds for the following year, we will liquidate equities in our brokerage account rather than draw from our cash. Selling just enough of an equity position that has a capital gain will be preferable so we can work to keep those gains in the 0% tax bracket. But if the market is down at the end of the year when we accumulate our living expenses for the following year, we will use our CDs and actual cash from our three year living expense reserve to avoid selling down equities.

Buying Real Estate

Another topic we revisited is housing. With the realization that economies around the world are down, it’s starting to feel a bit like 2008 again. One of the things I said to Ali back when we started this adventure was that if the US housing market has another dip like in 2008, which was when we bought the condo we used to own in Seattle, we should come back to the USA to look for real estate pronto. Even though we originally planned to live without a home of our own for at least five years and only one year has passed, it feels like it might be time to carve out some additional cash for a potential home purchase in 2021.

Eventually we do want to have a home again, which does not mean we will stop traveling. As COVID-19 sends most people home to stay safe we feel like we should figure out how we can be prepared to “go home” more easily in the future. And as we sit here in my sister’s rental house in Flagstaff for at least three months, we are talking about how much we do want to have a little home and garden of our own someday. So we’re starting to set money aside for a potential home purchase in 2021 now.

Related post: Home is More Than Just Housing

Roth Conversions

When Ali and I were still employed and maxing out our 401Ks we were in the Married Filing Jointly (MFJ) 25% marginal tax bracket. But we also were able to lower our tax obligation because we had 401K related tax deductions in those years before we retired which was really helpful. Since we consistently saved as much as possible in our 401Ks and benefitted from the bull market that started in 2009, the level of RMDs we will be compelled to take after we each turn 72 years old will push us back up into similar high tax brackets in the future. We revisited this topic again in our latest planning party, and our goal is still to avoid those RMDs if we can. One way to manage our income and tax brackets in the future is through Roth conversions now.

Related post: Avoiding the RMD Cliff

Back to the ACA vs Roth Conversion Conundrum

So it’s clear that there is a tug of war between maximizing Roth conversions and qualifying for ACA subsidies. I’m also discussing this with some new friends as I work with them on their numbers. It’s important to be aware of how RMDs, Roth conversions, and ACA subsidies impact retirement plans and future tax obligations. For me the best way to understand this puzzle is to build spreadsheets and graphs. So here we go…

Income Sources

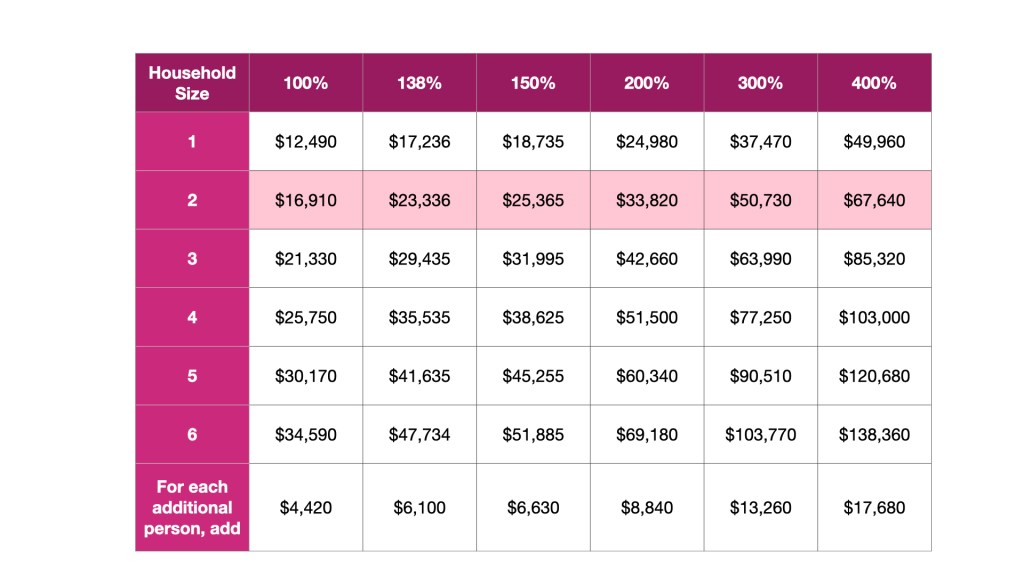

ACA Income Limits

When evaluating if you qualify for ACA subsidies you must add up all of your existing income types. The ACA requirements make it clear that income is income, regardless of the type. In doing research I found the HealthCare.gov site helpful and I also thought UC Berkeley’s Labor Center site was very helpful for understanding ACA income requirements.

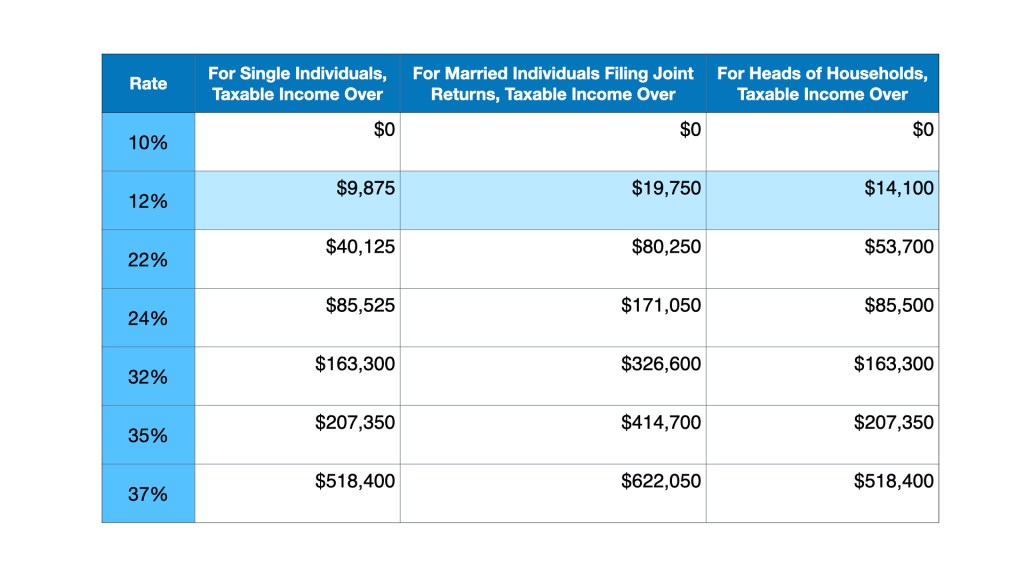

Tax Brackets

Everyone is different so I keep the 2020 IRS tax brackets handy when playing Money Crush with others. Many of us in the FIRE community have a higher tax bracket while we are employed and receiving job related income, and then drop to a lower tax bracket after retirement. For example, while employed in 2017 Ali and I were in the MFJ 25% marginal tax bracket, and this year in 2020 we’re trying to keep our income in the 12% tax bracket.

Testing Income Sources

To answer the Roth vs ACA question, I have built four different examples with a variety of income sources, shown in the following table. I’m keeping the numbers rounded and mostly generic to simplify things in this post. There are lots more income sources in this table below than we actually have available for ourselves, since I built this table for the case studies I’m working on with other people and we have a wide variety of different income sources between us. That’s what makes case studies interesting! But for this post I’m sticking close to real life for me and Ali, so the following four example scenarios only include the income sources Ali and I have in our real life portfolio.

The income types are listed from left to right in the table, in order of what we can control in terms of turning the income on or off. They are also grouped loosely by ordinary income or capital gains income. For example, once you start taking Social Security or a pension, you typically can’t turn that back off. But you can choose how much of a Roth conversion to make every year, or how much of your available cash to use to fund your expenses. The table below also shows the ACA subsidy limit and our MFJ tax filing status.

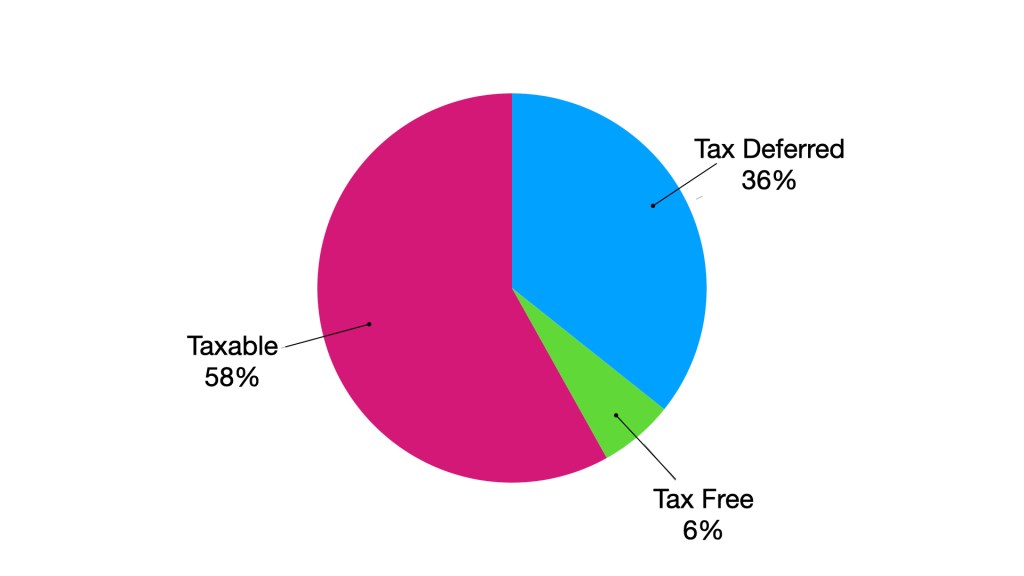

Taxable, Tax-Deferred, and Tax-Free Accounts

In our case we currently have more than half of our total portfolio in a taxable brokerage account. This allows us to access equities that comprise original cost basis and hopefully also capital gains. This is an important component for being able to turn on and off the different elements in our portfolio depending on whether our goal is bigger Roth conversions or qualifying for ACA subsidies as early retirees.

ACA Subsidy Cliff Examples

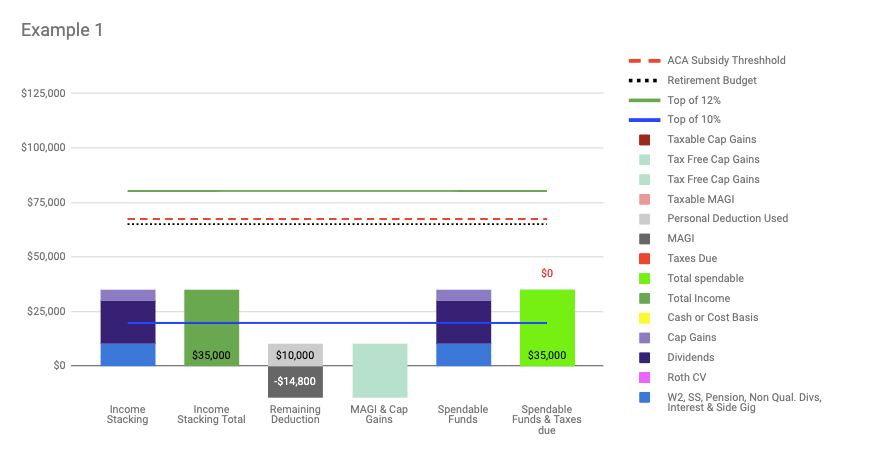

Example 1

For Example 1, I included $10,000 in ordinary income in the form of non-qualifying interest and dividends, as well as $25,000 in qualifying dividends and capital gains, which adds up to $35,000. I subtracted the $24,800 MFJ personal deduction, which makes the $10,000 in ordinary income essentially tax-free. That leaves $14,800 of the personal deduction to apply to qualifying dividends or capital gains when calculating taxes owed. As you can see in the graph below, that makes all capital gains in this example tax-free. And the income adds up to be well under the ACA income limit. But this example falls short in that it does not fully fund the retirement budget.

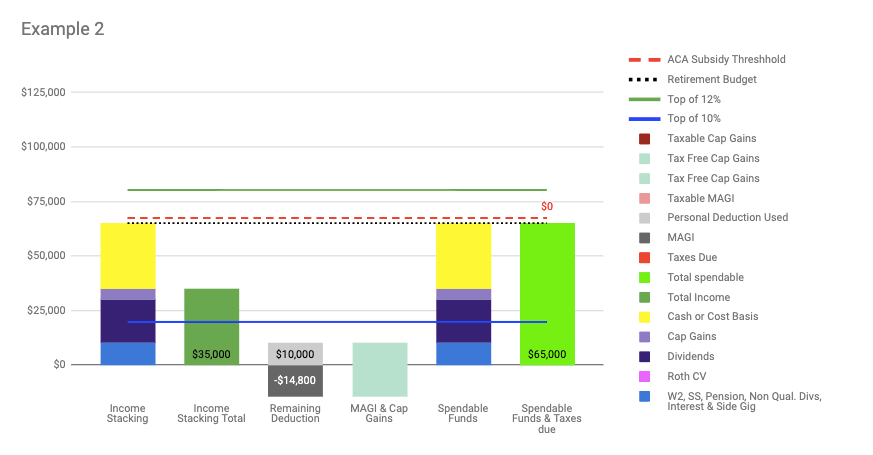

Example 2

Starting with the same incomes listed in Example 1, this time I also add in the cost basis from equities sold, associated with capital gains. The great thing about selling equities held in a brokerage account is capital gains are the only portion that are taxable, not the original cost basis. So if this example is managed correctly the additional $30,000 needed to fund the annual budget is both tax-free and also not counted as income toward the ACA threshold. And since the $65,000 budget is under the $67,400 threshold, the equity cost basis will top up the budget and this household will qualify for subsidies.

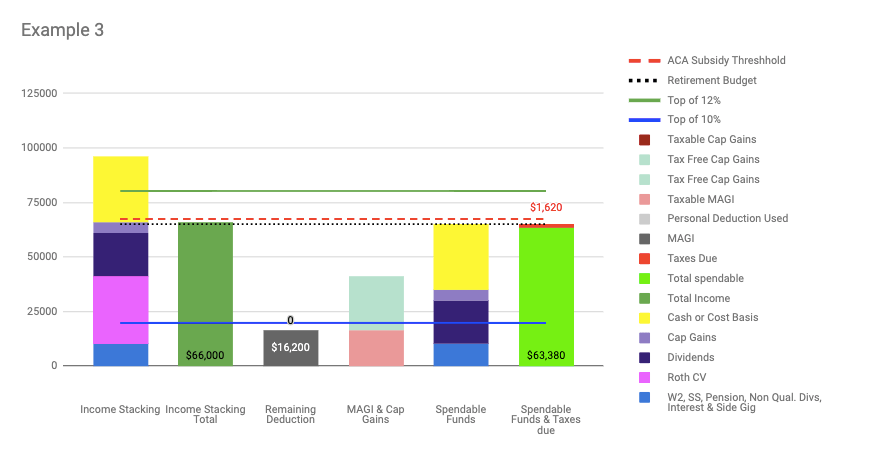

Example 3

In this example I included a $31,000 Roth conversion but still want to stay under the ACA income limit. No worries. Take the $35,000 income from above (not including cost basis) and subtract that from the ACA income limit, which is $67,400 for 2020. The remaining $32,400 is available for a Roth conversion. In this example the personal deduction does not fully wipe out the ordinary income as it did in Example 2. So there is a tax bill of $1,620 on ordinary income. And since the capital gains are under the top of the 0% capital gains tax bracket, there is no tax owed on them.

After layering all of the incomes, cost basis, and the Roth conversion Example 3 gives us a nice little cocktail that fits nicely under the ACA subsidy cliff.

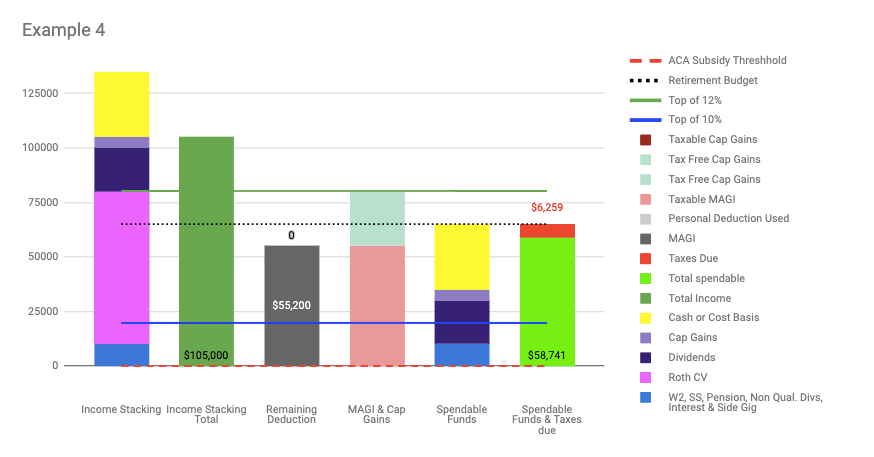

Example 4

In this last example I’m completely ignoring ACA income limits and focusing on staying within the 12% tax bracket, with the goal of maximizing Roth conversions. In the graph below we start with the same amount of ordinary income, dividends, and capital gains as in the previous examples. But this time I included a hefty $70,000 Roth conversion. When added to the other income sources this pushes the total up over the top of the 12% tax bracket. But after subtracting the personal deduction, the MAGI is reduced and the qualified dividends and capital gains fall just under the 0% capital gains rate and are tax free. And with the cost basis from an equity sale, there’s enough fungible funds to meet the retirement budget living expense needs. There are $6,259 in ordinary income taxes due in this example. But we are willing to accept the higher taxes now because $70,000 has been moved over to grow longterm in the tax-free Roth account.

The Latest Lessons Learned

The biggest lesson for me is that there is a huge inverse connection between Roth conversions and ACA income limits. For the near term we know we want to be nomads. And we know now since the COVID-19 pandemic changed the world that we might not be able to control the timing of when we would need to spend more than 180 days in the US. Coming back to the US for longer durations is not what we had planned, but changes in world economies and border closures are obviously not things we can control.

After our latest planning party I can say that it’s possible we’ll decide to buy real estate in the US within the next two years. We want to create a space to use as our personal home as well as a co-living space for members of our chosen family.

Now that we are halfway through 2020, we have a much better understanding for the types of travel restrictions we need to cope with as nomads. We were in Mexico from January 1 to May 3 this year, which means we must be outside of the US for another two months this year in order to make sure we don’t render ourselves ineligible for our existing health insurance plan. If possible, we will continue spending at least six months outside of the US every year for at least the next five years, while we stay on our international health insurance plan. And we will keep doing Roth conversions without having to worry about ACA income limits.

So I will make my second Roth conversion of another $30,000 before the end of this year. When it’s time to get on the ACA we will make the appropriate adjustments to our Roth conversion plan so we can stay well under the ACA income limits. And as always, we will keep referring back to our Personal Money Statement to make sure we are taking all options into consideration and avoiding hasty decisions.

So excited to read this all the way through after work today. I’m getting dangerously close to FI and all of these issues are swirling for me too. On a fun note, I’m just down the hill in New River. Maybe someday we can grab a cup of coffee when I come visit my son in flag. Enjoy reading your posts!

LikeLiked by 1 person

Thanks! Let me know if you have any questions. I learn a lot batting this around with folks. And meeting up for coffee would be fun if it weren’t for this darn COVID. Maybe next time we pass through. Cheers!

LikeLike

I love your Money Crush posts!

I know this may seem a little contrary to the point of this post, but if you have readers who are very adept at harvesting capital losses to balance out capital gains, they may wind up with not enough income to qualify for an ACA subsidy. The lower end is based on whether or not your state has accepted Medicaid expansion, but, for example, because we use rental properties for our retirement income, our MAGI would be very low due to depreciation. We may be in a position where, if we’re going to use an ACA plan in the future, we would need to make Roth conversions just to create enough income to be above the 100% FPL level.

To throw another kink, for those who have earned income, there’s also a saver’s credit cliff to consider when trying to dial in how much to convert: https://www.hullfinancialplanning.com/the-savers-credit-cliff/

LikeLiked by 1 person

This is great info! And thanks for your link. I will be circling back to read up. Thanks!!!!!

LikeLiked by 1 person

This is timely info, as we too are looking at Roth conversion strategies, and we currently are on the ACA. Confirms my understanding on the ACA penalties and Roth conversion limits, as we appear to be very close on your left side numbers. Great insight, thanks for posting and getting me to think more about this.

LikeLiked by 1 person

Sure thing. What state are you in? I try to keep close track of our income and am glad we can do several batches of conversions so we can sneak up on our conversion max. If you want to do both Roth conversions and be on the ACA, staying on top of as much as you can on these topics is really important. Good luck!

LikeLike

Thanks for your thorough explanation of these potentially financially tricky situations. Seems like a lot of us are caught in this same ACA/12% tax conundrum. Your post last year on your Roth conversion plan led me to run my own numbers and I appreciate seeing the ACA addition this year. Best wishes for future travel!

LikeLiked by 1 person

Glad these Roth conversion posts have spurred you on to a deeper dive into your own money. Good luck!

LikeLike

Hey Alison, great post and awesome blog. I’m a budding nomad to be in 2021 if things go correctly. We’ll see. 🙂

With your international health insurance, do you also have to have an ACA plan? I’m trying to familiarize myself with the insurance side and things I will need to consider in 2021. Thanks for the great content and stay safe!

LikeLiked by 1 person

Hey Lisa, Thanks! Regarding also having an ACA plan AND international insurance, it really depends where you’ll be spending more time. If you will have a home base in the US and spend more than 50% of your time there, I would consider being on the ACA. But if you will be out of the US a lot, then an international health care plan is a better idea. You can find plans that will cover you when you come back to the US or buy trip health insurance for the times you are back. We thought about doing that pre COVID. But with all the border restrictions now we’re glad we had international medical insurance that also covered us in the US. It’s a puzzle that can be really fun to figure out. But our international insurance requires us to be out of the US 6+ months a year, so we have to be out again by mid October. We are waiting to see where’s the best place for us to restart our travels and it’s not very clear right now. Cheers!

LikeLike

[…] For tax purposes we are Married Filing Jointly (MFJ) with no dependents. We’re able to qualify for tax credits to help pay for an ACA marketplace plan as long as we can keep our taxable income level below the 400% federal poverty level, which is $68,960 for 2021. Our spendable income is well below the limit, but our taxable income including Roth conversions can easily disqualify us from subsidies if we continue with our previous Roth conversion strategy. […]

LikeLiked by 1 person