We are not certified professionals. For more information about us please read our Disclaimer.

Personally, we had a great year of travel in 2019. And even with surprise medical costs, our 2019 spending proved that our budget was a good fit. We also learned how to be very happy and grounded being Home Free. But, how did our portfolio do last year?

The first thing to note, which was totally new and different for us, is that we lived 100% off cash in 2019. We did not sell any equities in 2019 to cover our living expenses. We set cash aside for 2019 as part of our departure plan from Seattle at the end of 2018, using the proceeds from selling our car and condo.

The second thing to note, is that 2019 was the first year that our portfolio had all of the necessary ingredients to sit and bake in its current form. We simplified and consolidated the various investment accounts we had opened during our employment years, so that we would each have one rollover IRA and one Roth. We also consolidated the balance of our condo proceeds into our brokerage account. 2019 was a very important growth year for our portfolio during our first year of retirement.

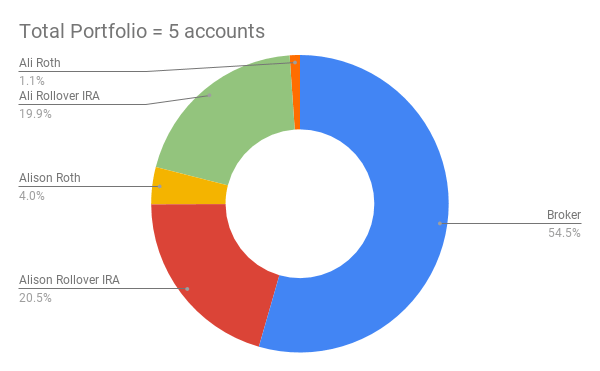

Our Five Account Portfolio

We currently have five accounts in our portfolio (not counting our regular checking and savings accounts) that we use to support our FIRE plan. We intend to use these five accounts as our own laddered safe withdrawal plan.

- Our joint brokerage account (taxable)

- My rollover IRA account (tax-deferred)

- Ali’s rollover IRA account (tax-deferred)

- My Roth account (tax-free)

- Ali’s Roth account (tax-free)

Currently, 54.5% of our total portfolio is in our taxable brokerage account, and the great health of that account is thanks in large part to the condo we sold in 2018. As of today our two rollover IRAs each have about 20% of our portfolio in them. Only about 5% of our portfolio is in our Roth accounts at this point, but that will change this year if all goes according to plan.

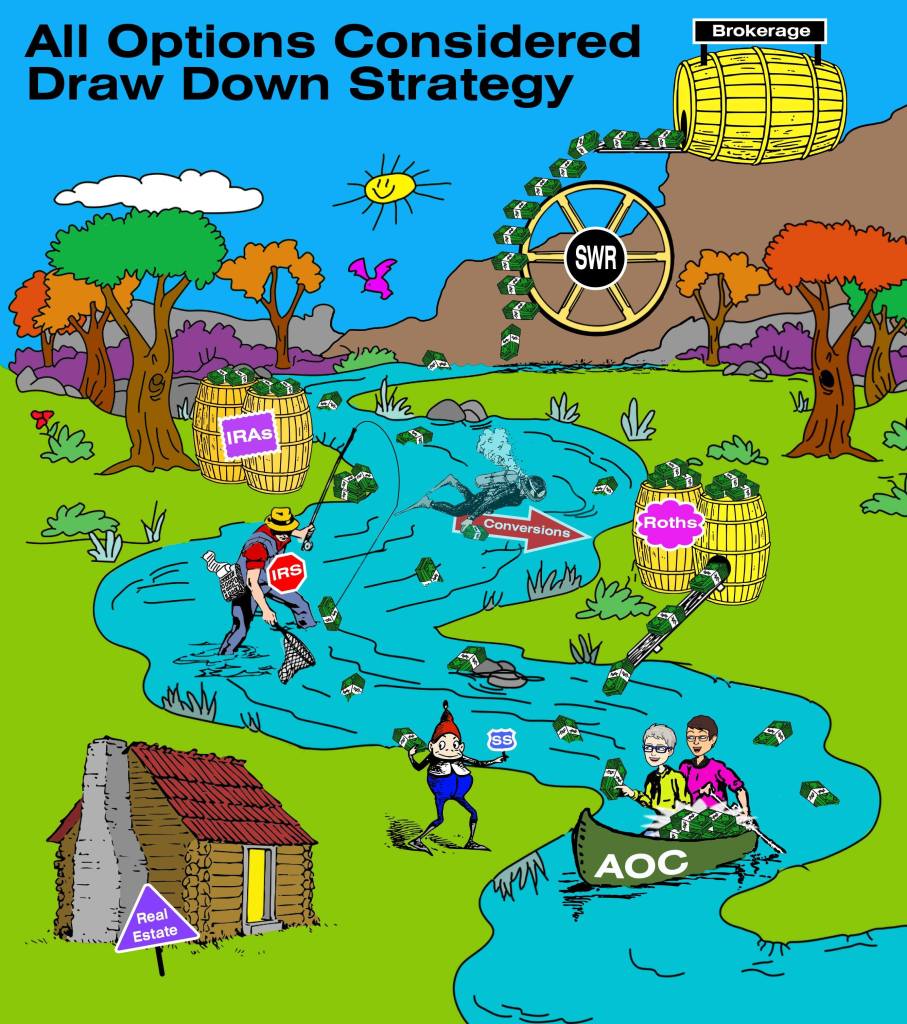

The AOC Safe Withdrawal Plan

Brokerage Account First

Our goal is to use only our brokerage account for the next few years, to cover all of our living expenses until that first account is completely empty. Based on predicted market conditions, we would like to estimate that our brokerage account could fund our current living expenses for another 15 years if we use the same budget we have now with inflation increases. But we all know you cannot predict the market. We assume we will keep traveling full-time for at least a few more years. But it’s also possible that we will want to have a home in one location again at some point.

The Housing Question

If we decide to buy a home in the near future we would likely liquidate a significant portion of our brokerage account to give ourselves money for an all cash housing purchase. That would quicken the pace of emptying our brokerage account and require us to start tapping into other accounts sooner. Though we are also very open to the idea of renting or ongoing slow travel instead of owning a home again. Housing is for sure an area for us where All Options Are Considered.

Roth Conversions

We actually do not plan to use our rollover IRA accounts for our living expenses. We plan to consolidate our rollover IRAs into our Roth accounts. We started making Roth conversions in 2019, and at this point we intend to make additional conversions each year until the rollover IRAs are empty or close to it. Our goal is to reduce the size of RMDs we would be forced to take on the IRSs schedule, and also reduce the amount of taxes the IRS would be forcing us to pay based on the government’s RMD schedule.

Once our brokerage account has been depleted, we assume we would use our Roth accounts to cover our living expenses. After I reach age 59.5 we can start making withdrawals from my Roth account without penalties to help cover our expenses, and continue using that account until it is depleted. And 10 years later when Ali is age 59.5 (since I am 10 years older than Ali) we can start making withdrawals from her Roth account without penalties to help cover our expenses as well.

Social Security

As for Social Security, there are a lot of scenarios in my spreadsheets where I could possibly start taking Social Security as early as 62 years of age to protect from sequence of return risk, or during a prolonged under-performing market, or other possible scenarios. At this point it’s impossible to say for sure if I would take Social Security early or delay taking it until I’m 70. I’m happy to have multiple scenarios to work with on my spreadsheets!

Distilling Our Draw Drown Strategy

We are starting to look at our draw down strategy like it’s a recipe for creating a fabulous Scotch whisky. We have the right ingredients from our years as salaried employees. The malting, mashing, and fermenting is done (we do not plan to have jobs again in the future). As much as we love a good single malt, we are working on a blended whisky and we are happy to have a bunch of different investment barrels to work with (diversity in all things is important to us). And now we definitely have to let our investments age in their barrels as long as possible. Scotch whisky must be matured for at least 3 years and we certainly want every barrel in our portfolio to mature longer than that. Since we’re working on a blended whisky, each barrel will be allowed to mature to a different age. We know that if we take too much money out too quickly, we’ll end up with some unsatisfying beer that could have been a fabulous Scotch. We also know the IRS will definitely take its angel share of our brew, and we do want to do our share and pay our taxes to help support common resources back in the US. But like any responsible investor we also want to maximize the share of whisky and money we get to enjoy ourselves.

We love creating fun and wacky visuals when we have planning sessions about money and life. We also think creating graphics like these for visualizing your money, can make financial conversations more interesting and successful for people. These exercises can be especially useful for couples so you’re not just having a left brain negotiation about money, you’re also working on a fun right brain project that is designed to help you communicate more clearly. The latest visual we created when we were talking about our draw down strategy for 2020 is below. We had a great time working on this, though we were clearly craving some good Scotch whisky at the time!

Our Current Allocations

In 2019 we had an equity to bond allocation of 75/25, and that’s about where our allocation is still. We were comfortable with that allocation since we had cash to cover our living expenses last year, and there was a continued bull market in 2019. The bond portion of our portfolio is important because it holds bonds as well as cash and CDs that we will draw from over the next few years as a way to protect ourselves from sequence of return risk (SORR).

Planned Allocation Changes

I reallocate our portfolio every year in May to push the balances back into equilibrium, whether the market is high or low. Planned rebalancing on Ali’s birthday ever year helps remind me to take action on the same date annually and focus on longterm growth, instead of waiting for the market to change and worrying about short-term market fluctuations.

In addition to annual rebalancing, we have cash and bonds available to deploy if there is a very significant down market. And we all know that something like a 10-15% market drop (or more) is a real possibility in the next few years. Since we plan to enjoy a longer retirement period of over 50 years, we’ve decided our current 75% equities balance is a little lower than we’d like to have in our portfolio at this point. A higher equity allocation should help us leverage longterm market growth, so we are looking at an equity glide path using more cash now during our early retirement years, while also shifting more of our bond holdings into equities during down markets if they come. But for sure incrementally those shifts will happen every year during our May rebalancing.

To be specific, if we decide to own our own home again we will likely push our equities up to 90% over time. It can be argued that owning real estate is more like holding bonds as a longterm inflation hedging investment. However, if we continue as full-time travelers or rent in one location, we would still want to consider diversifying with real estate by owning a rental property again. In either case, we will be pushing our equities higher over the next 5-7 years.

2019 Portfolio Activity

We did sell some equities for tax-gain harvesting in 2019, since our investment income was low enough that we could leverage some of the 0% tax bracket for capital gains last year. The proceeds from selling equities were immediately reinvested into our ETF portfolio to rebalance our equity to bond percentages. We plan to do the same type of capital gains harvesting again in 2020.

We did one round of Roth conversions in 2019, and now I know a lot more about the Roth conversion balancing act than I did a few months ago. I might have converted a little too much in 2019, since our dividend income turned out to be higher than expected. The larger return on dividends was a surprise, but I can’t really complain about our investments turning out more dividends than expected! That’s all part of the learning process since we are managing our own money. No matter what, I’m excited to have started the Roth conversion process and we will keep it going in 2020.

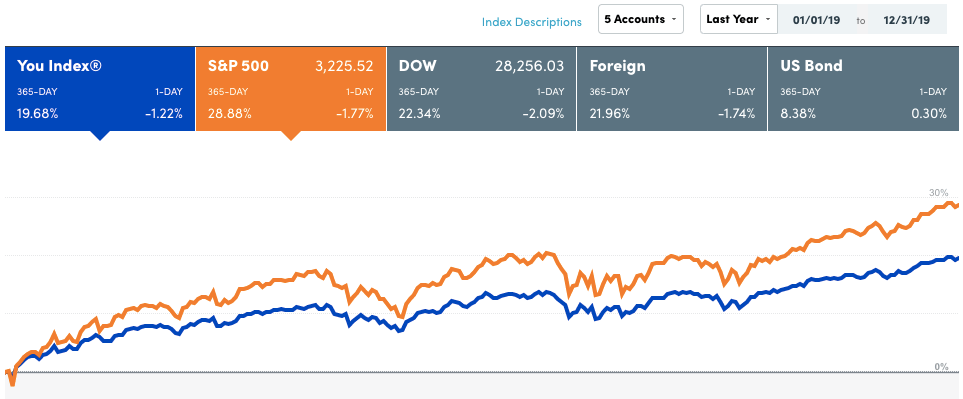

2019 Bull Market Results

The market had a fabulous year in 2019. And thankfully, so did our portfolio. The S&P gained a whopping 28.88% in 2019. And our portfolio gained 19.68% last year. I’m very happy with that return!

Looking at these positive results in our portfolio gives me a chance to take a bigger picture look as well. At the end of 2018 we reported a negative return of -5.34%, as compared to the S&P’s return of -6.24% in 2018. I was happy to beat the market in 2018, but of course we were not thrilled with the negative return and we were hoping to do much better in 2019. Since 2019 was so strong that gives us a much better average with a positive gain of 7.17% over two years. And with our 2.7% safe withdrawal rate our portfolio is right on target as we move through the first quarter of 2020.

What’s Next for 2020?

We will start paying quarterly estimated taxes in 2020, which we didn’t need to do in 2019 since we had a big tax credit from 2018 when we finished working and hit the early retirement button.

We will do more Roth conversions since that’s our plan to reduce or avoid RMDs in the future. If equities are down we can move a higher number of shares for the same dollar amount we’re targeting for the conversion. We will do multiple Roth conversions for each account during the year, rather than a single large conversion. I’ll need to track dividends, capital gains, and total Roth conversions very closely during the year to stay under that pesky 12% tax bracket.

When I do our portfolio rebalancing in May, we might want to combine that process with capital gains harvesting. That will help us finish migrating our taxable portfolio over to all ETFs and sell the last few individual stocks we still own. We will need to pay attention to how that changes our allocation and taxes as well.

Lastly, if we experience a more significant market correction or a prolonged down market in 2020, we will not panic!! Especially me – I promise not to panic. We will be going back into our fabulous Personal Money Statement (PMS) in the first quarter, so we can make a few updates and also make sure we keep a clear head about our originally stated investment goals. Even though I will get to enjoy buying at a discount if there are any major down days this year, Ali and I will have to stay on top of my nerves if that happens. I will busy myself with tracking our daily spending, and keeping an eye out for any spending creep or lifestyle inflation. No matter what, we will also have lots of fun together this year!

I love reading this even though it makes my eyes glaze over a bit. I’m several-to-many years out from pulling the trigger so it’s great timing for me to follow along and think about all the things I don’t know about managing money when I no longer have an income! I hope I’ll understand more and more as time goes by.

LikeLiked by 2 people

Keep reading everything you can. I am for sure NOT an expert but I read and learn every day. In fact, I’m working on a rental cash flow project with a friend right now (crazy me) and the conversation I had with my Dad just before he passed in 2012 about how to value a property using the “cap rate” just clicked. Keep reading!

LikeLike

Love this post for so many reasons. You’re clearly ON TOP of your finances, love the visual drawing, love the whisky comparison, and love the PMS. Congrats on 1 year down of no income!

LikeLiked by 2 people

Ali and I had so much fun brainstorming that info graphic. We laughed and laughed when I added the social security troll. Who said money isn’t fun!

LikeLike

Thanks for sharing!

I’m still slowly building the skeleton of our planned retirement income and we’re still (what feels like) lightyears away so I have time but I really appreciate absorbing how all y’all adventurers are setting up their plans, why, and figuring out how it might figure into our plans in the future.

I’m sure you’ve mentioned this in the past and I’ve just missed it, but for the purpose of this annual review, how are you handling health care?

LikeLiked by 1 person

Good question. We do have IMG for global catastrophic health care needs. Everything else we pay for out of pocket. We have a post on that coming in the next month or so. But for now have a look at this post were we really went into depth. Good luck! https://alloptionsconsidered.com/2019/03/26/expat-medical-insurance-and-medical-tourism/

LikeLike

Thanks for sharing AOC – the 75/25 allocation is a validation for my own 80/20.

I came here from FireDrill podcast. Now to follow 🙂

LikeLiked by 1 person

Welcome! We’ve been glad that during our early retirement years we are not at a higher allocation given the emotion in the market right now. Over time we will look a using at glide path to increase our allocation. For now, we are thankful to our cash as it has a job to protect us for sequence of return risk. Cheers!

LikeLike