2020 was weird. Writing about personal spending and portfolio growth after such a problematic year feels less interesting than it has in the past. But there are good reasons why these are among the most typical topics in the FIRE (financial independence / retire early) community. Despite how tough last year was for many people and how awkward it feels to talk about money now, it’s still just as important to normalize money conversations and promote financial education. And even though we all track and spend money in unique ways we can learn a lot from each other. Besides all that Alison and I enjoy taking the time to analyze our spending and our portfolio as part of our normal process for closing the books on last year and discussing what we might do differently with our personal finances next year.

2020 Spending

Our spending and expenses have been relatively simple to track and manage since we reached FIRE in 2018 because we were nomads without a home of our own or very many bills to pay.

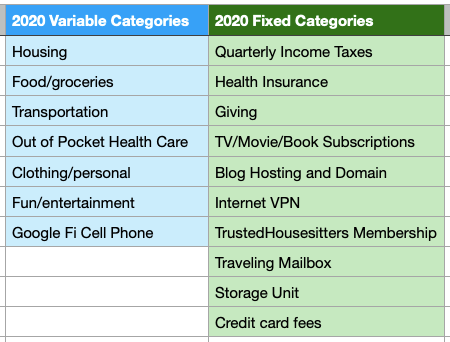

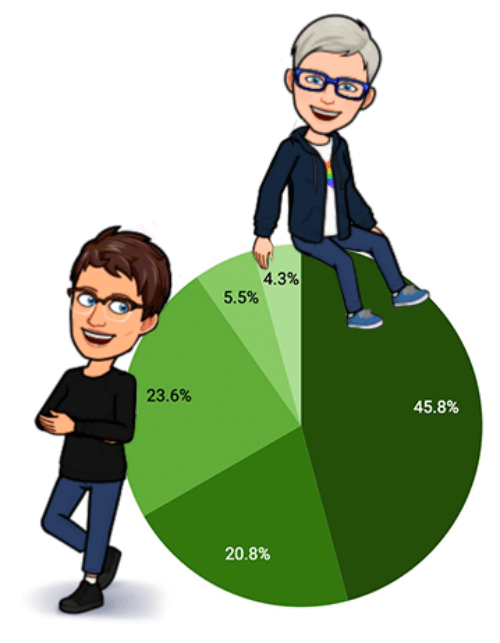

The graphic below shows our spending on fixed expenses along with the four major categories we were tracking within our variable expenses (food, housing, transportation, and fun). Our fixed expenses included our health insurance premiums with IMG, our little storage unit in Seattle, our audio book and TV/movie streaming subscriptions, plus the quarterly income taxes we paid to the IRS. Our fixed expenses also included a generous budget for giving money to our six nieces and nephews, political and charitable giving, plus monthly bills we paid for my mom’s living expenses.

Our biggest travel hack in 2019 was housesitting in three countries resulting in 68 free nights and a significant savings in housing expenses. We didn’t do much travel hacking in 2020 because of Covid. We only had a single 22-night housesit in Mexico in January and then cancelations for two additional month-long housesits and finally a 10-night housesit that was just canceled in December. We had booked United Excursionist Fare flights for our 2020 summer travel plans with Alison’s mom but we had to cancel that trip due to Covid.

People still ask us for travel hacking tips and we are happy to share what we’ve learned so far through credit card rewards, airline miles, housesitting, and more. We’re still paying for our membership with TrustedHousessiters, because we love that organization and everyone we’ve met through it and we intend to keep housesitting when we can. It’s possible that 2021 will include some great travel hacks for us with a new credit card or a couple of housesits. But the truth is at this point travel hacking just doesn’t have as much appeal for us.

Post-FIRE Portfolio Growth

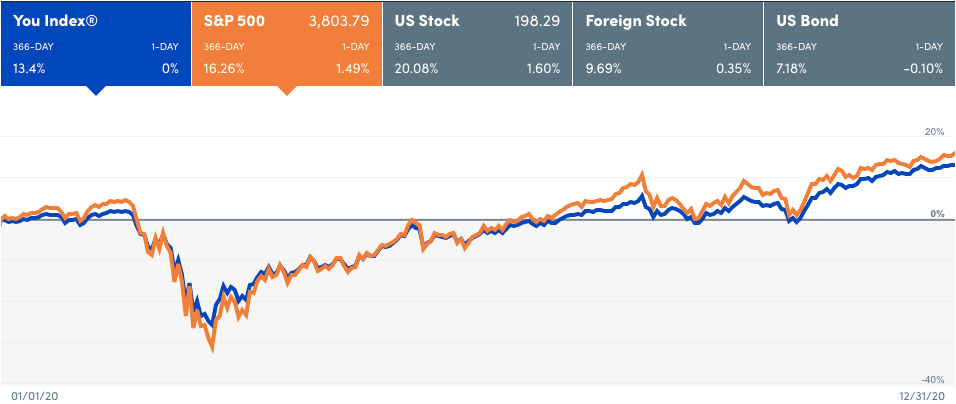

The economy was a wreck in 2020 both in the USA and across the world, and things haven’t improved yet. Meanwhile, market growth was strong last year even though the Covid Crash caused markets to suffer a series of massive drops. Our portfolio lost almost 28% of its value during the Covid Crash and yet our overall portfolio growth in 2020 was 13.4%. Because our allocation is 75% equities and 25% bonds, our portfolio didn’t drop as far as the overall market during the Covid Crash but our recovery was still strong. Many of us are benefiting from a strong market while the economy is in turmoil and other people are suffering financially. This is a great reminder for us to give back to people in need.

Post-FIRE Portfolio Maintenance

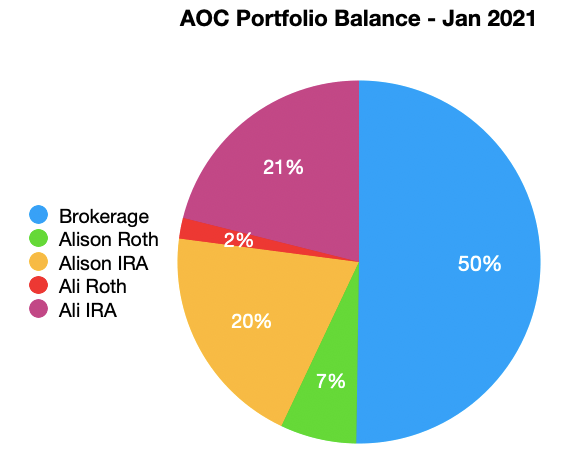

Since we reached FIRE we don’t have paychecks or other forms of new income to save or invest. It’s amazing to see how much our portfolio continues to grow, even without new income and with market downturns. We make two types of proactive moves in our portfolio every year, the first one is a scheduled rebalancing in May and the second one is annual Roth conversions.

Rebalancing: Our rule for rebalancing is that our allocation ratio must be at least 5% off from our allocation target in order for us to do anything. Having that 5% rule in our Personal Money Statement helps us remember that rebalancing is about correcting our equity to bond ratio, it’s not just an opportunity to play the market. The Covid Crash tossed our allocation out of balance so our scheduled rebalancing in May was perfect timing for reinvesting dividends and returning our portfolio to 75% equities and 25% bonds. When we set up our cash for the coming year in January, which we just did for 2021, we review our allocation before selling any holdings and then make sure the withdrawals we make for our living expenses allow us to adjust allocations again.

Roth conversions: Our total Roth conversions last year were $58,000 from our IRA’s to our Roth accounts. We made a $29,000 Roth conversion during the Covid Crash and moved half of that money from my IRA to my Roth and the other half of that money from Alison’s IRA to her Roth. We made a second Roth conversion for 2020 a couple of weeks ago in December moving another $29,000 from Alison’s IRA to her Roth. We decided to focus that second conversion on Alison’s accounts since she’s 10 years older than me and we have less time to convert her pre-tax dollars to her tax free Roth before IRA required minimum distributions begin.

Tracking Regular Spending

Our variable expenses were the simple part of our spending since we were living as nomads in 2020. Our variable expenses included our housing costs in the form of Airbnb rent in Mexico, Canada, and the USA. Our other variable expenses included transportation, food, any personal items or clothing we needed, and fun extras like admission prices to botanical gardens or cooking classes. Our fixed expenses in 2020 basically included everything outside of our daily living costs like our health insurance premiums, quarterly income tax payments, and our giving budget items.

Tracking Major One-Time Expenses

We track major one-time expenses separate from regular spending on our living expenses. We also kept that major one-time expense money separate from our living expense cash and we even tracked it separate from our portfolio and didn’t calculate it with our investments. In 2020 our big one-time spend was our home purchase. We had planned and budgeted for our home purchase back when we sold our condo at the end of 2018. We agreed back then that if we wanted to buy a new home our budget for that purchase should be around 50% of the selling price of our condo, and we stuck to that plan.

We’ll have a major one-time expense in 2021 as well since we need to buy a car but thankfully that won’t be anywhere near as expensive as our home purchase. We withdrew extra money for our car purchase when we did our living expense withdrawal last week and set that money aside for use at the end of this month.

When Plans Change Budgets Need to Change

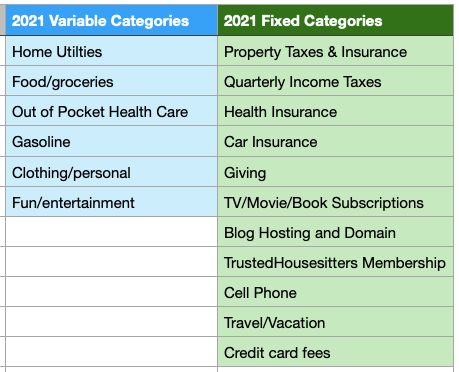

For our spending in 2021 we’ve built a very different looking budget. Almost every part of our spending is changing in 2021 including housing, health insurance, and our taxes. Some things won’t change since our giving budget will be the same at around 10% of our budget. Our fun budget will be the same as well, even if we still want to stay isolated because of Covid. Maybe we’ll buy state park passes and take a couple of online cooking classes. But there are a bunch of individual expenses and budget categories that will change for us in 2021. Including…

- We’ll stop paying for storage unit fees, which were $1,200 in 2020.

- Our health insurance premiums are going down from $302.50/month for global insurance with IMG, to now paying $144.71/month after subsidies for an ACA plan in Arizona.

- Our housing budget will shift from covering rental costs for Airbnb’s, to being property taxes and home owner’s insurance.

- We’ll have new utility bills to pay every month: Water from a private water utility since our house is not on city water, electricity, natural gas, trash and recycling.

- We’ll start keeping a separate emergency fund for home maintenance needs.

- In addition to continuing to pay federal income taxes we’ll also start paying state income taxes for the first time in decades.

- We’ll need to pay for car insurance in 2021.

- We’ve added a category for travel back into our budget since we aren’t nomads anymore.

- We’ll stop paying for the VPN we used for internet security while traveling.

- We’ll stop paying for Traveling Mailbox since we’ll have a real mailbox and a housemate who can check our mail when we aren’t home.

Time to Focus on 2021

We’ve built a very different looking set of budget categories for our spending in 2021 since our spending will be more complex with roughly twice as many bills to pay this year compared to last year. Almost everything about our spending is different including housing, health insurance, and taxes. But our total budget hasn’t changed since 2017, and we appreciate it when we come in under budget. The first few days of 2021 were even more crazy than almost everything we saw in 2020. There are very few things we can control these days, but we can control our post-FIRE spending. We’re still looking forward to a really good year and a whole new kind of normal.

We are not certified financial professionals, this post contains affiliate links. For more information please read our Disclaimer.

Cheers to your continuing happiness. We too are optimistic about a better 2021. Hopefully the new US administration speeds vaccinations. I’ve already had both of mine. A slightly sore arm was my only side effect both times. We may never have our old normal back. But change is part of the beauty of life.

LikeLiked by 1 person

Thanks for keeping being transparent about your spending in 2020!Have you considered doing side by side comparison between 2019 and 2020? I am especially curious to know if you did experience major change in Food/Housing/Transporatoin and Fun compared to last year, due to COVID19.

It is also great to see that even during a pandemic you portolio has been doing extremely well! As for your reballancing, since the market recover unexpectedly well (and I know you aren’t trying to play the market) do you think that rebalance was necessary? In other words, did you add to rebalance on Jan 1st 2021 to adjust to the market performance after your reballancing?

LikeLiked by 1 person

We decided not to do a direct comparison because we had big differences in 2019 to 2020 with the number of housesits we had (2019 = 68 free nights, 2020 = 22 free nights) and the use of travel points between locations. Although we did use points to return from Mexico in May and do our round trip to the UK in October. However, our average housing spend in 2020 was below our target of $50/night because we rented from family for 4 months in the US even with our long stay in the UK at the end of the year. But in general, we did see a drop in Food/Housing/Transportation, though not dramatically so. What was challenging was seeing categories drop to almost zero like Fun. We stayed very isolated and created a family bubble with my mom for the summer. So our entertainment was at home and spending time walking in the neighborhood with mom.

We did perform a rebalance at our usual time in May but by then the market was recovering so there wasn’t much to do. Then in January of 2021 when we pulled out our 2021 living funds out of the portfolio we did consider the current allocation at the time to pick which holdings to sell. We had an additional consideration as we had to pay attention to how much capital gains we would be generating as we have developed a new plan to stay under a target income so we can qualify for ACA subsidies. So it was a bit of a balancing act to be adding to rebalancing considerations.

LikeLike

Hi,

I just discovered your blog, so I know little about you, ladies, but I intend to peruse your articles because they seem to have quality as compared to other PF blogs who seem to sell FIRE idea just for the clicks. I like your conservatism with the numbers.

I’m curious though why you’re doing Roth IRA conversions. Is it because you’re sure that you are in the lowest tax bracket than you’ll ever be or because you read here and there that it’s good to do Roth conversions? I’ve been under impression for the longest time that it’s just good to do such conversions, period. Then I came across some serious research that was done by people who are much smarter than me and discovered that Roth IRA conversions have more myth to them than truth. Yes, they are still a valid strategy, but are extremely dependent on case-by-case basis.

We’re still working FT (hence high taxes) and therefore Roth Conversions are not applicable to us, but I’m compiling all the articles about them and will study them once we retire in a few years hopefully.

Can I ask how old you both are now and when you retired? Of course, I might find out while reading your blog further, but I’m curious now :-).

Also, if I understand correctly, you don’t disclose your spending in dollars, do you? I understand that you wouldn’t want to divulge your NW or 401k’s, but knowing expenses would be helpful to put things into perspective… Again, maybe you do, I’m new here.

TIA

LikeLiked by 1 person

Hi Sana, Welcome!

We are currently 46 (Ali) and 57 (Alison). We retired in 2018 at 44 and 54. If you keep reading you will find that we spend between $60-65K a year. One reason its at that level is that we had a commitment to travel during the summers with my mom so our budget was double during those months. But for the last 2 years, even with traveling with mom in 2019 and a summer of COVID in 2020, we came in just over $60K. So due to our family commitments our budget might seem higher than the average budget conscious travelers.

Regarding Roth conversion, depending on your post FIRE drawdown strategy, one could find themselves in a situation where all your retirement streams of income plus your RMDs push you over the 12% bracket and having to allocate a good chunk of your annual budget to taxes. In our case, it was clear the longer we waited to access our IRAs the bigger those RMDs were going to be. And we really wanted to have more control over what money we with drew and when. For some, RMDs wont make that much difference in their overall tax obligation. But in our case, if we waited to access those accounts it would make a big difference. And yes, everyone should try to “estimate” what that might look like. That’s why, you will eventually see if you keep reading, it’s a question we have been working hard on testing in our draw down plan since the beginning.

Keep the questions coming!

~Alison

LikeLike

Forgot another question…

Is it just because of Covid you’re putting traveling on the shelf for a few years (?) or was it always a plan to buy a house in AZ and then travel while leaving the house behind?

I see that you have Aikisha&Billy on your blog, so I’m curious if you borrowed the idea from them (they have a dwelling in AZ, I think, but live in Mexico by housesitting).

LikeLiked by 1 person

We’ve followed Billy and Akaisha for a long time. Just recently we swopped interviews. Its was fun as they were one of our first inspirations.

We “pulled over” from traveling full time 1) because of the unpredictable nature of international travel and COVID. 2) I (Alison) was having a hard time with the idea of being so far away from my mom who happens to live in AZ. Since we couldn’t take her on an international trip last summer, we came back to AZ and kidnapped her out of her retirement home for 4 months and created a COVID bubble. It was a blast. 3) The longer COVID and restrictions on travel have gone on, the more we wanted to create a safe home base for us to wait things out. We also had a longterm plan to eventually set up a home base/ co-living space with an old friend. So we just moved up the timeline of that plan and we all picked Northern AZ for its proximity to destinations in the West and its only 2 hours from my mom. We will travel 1-3 months at a time when COVID is under control and countries start to reopen. But we are thinking it will be a year or so before that happens to a level we are comfortable. ~Alison

LikeLike

I’ve never quite figured out how to allocate funds in a taxable account so that I can live off them for the first 5 years of doing Roth conversions. Do you just keep mostly bonds there while waiting for retirement accounts to become available?

LikeLiked by 1 person

Good question! Our brokerage account has more than 5 years of living expenses in it. But we only have about that much in cash or bonds. If the market is up, we sell equities that don’t have a ton of gains on them so we are only taxed on their capital gains. If the market is down when we need funds, we either use cash or bonds that have not lost or gained much to fund our expenses. Its all about what tax bracket you want to be in that year or what income level you are trying to hit to qualify for ACA subsidies.

LikeLiked by 1 person