Over the years I’ve read a lot of articles about the idea of building a bucket strategy for withdrawals from your various accounts after you retire. Even though I had read every article on this topic that I could get my hands on, I didn’t find a clear step-by-step roadmap that showed how we might set up our own bucket strategy, partly because the advice out there didn’t seem geared for us. Some articles were focused on 2 buckets for people starting retirement at age 65 or older (that wasn’t us). Other articles were focused on people retiring with extreme wealth and extra buckets for additional asset types we don’t hold (that wasn’t us either).

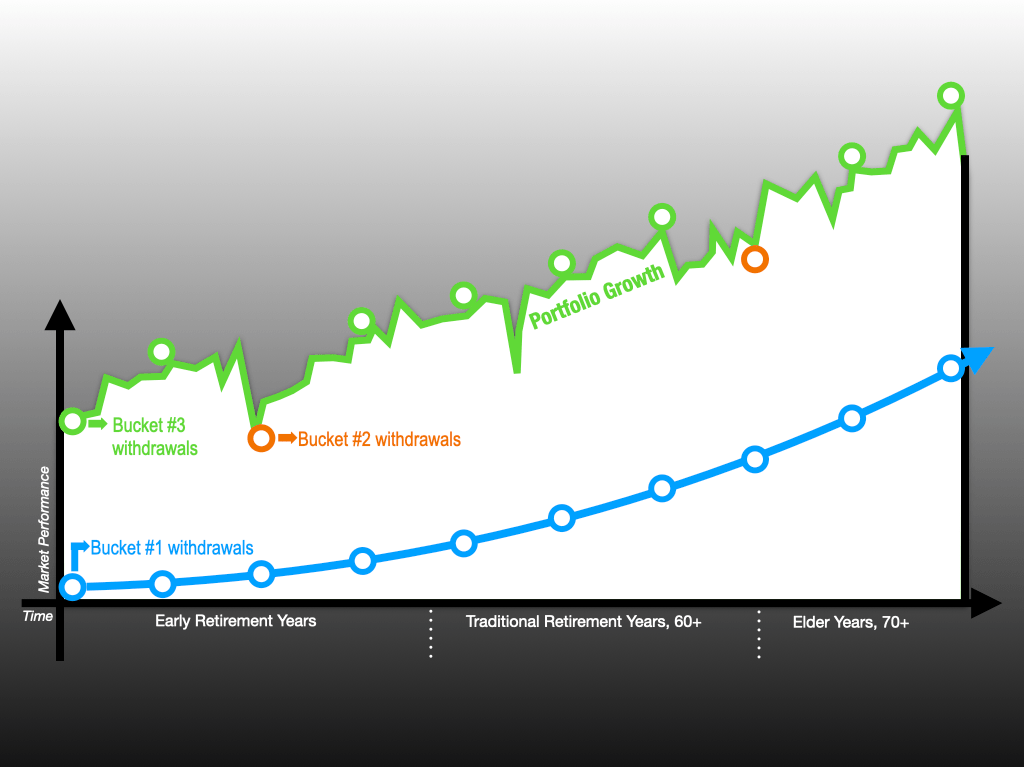

As we prepared for our own retirement in 2018 we knew we needed money to live on in early retirement during our 40’s and 50’s. We also knew we needed to save and grow enough money to cover our late retirement years during our 70’s and 80’s and beyond. But what about all the years in between? We wanted to set our bucket strategy to ensure our portfolio would outlast Ali’s life expectancy since she’s 10 years younger than I am. How would our buckets work starting from Ali’s 40’s all the way until her 90’s and beyond? What would our annual withdrawals look like over a 60 year retirement timeframe? And which accounts would our money come from at each stage in our lives? The best way for us to figure all of that out was to dive into the process of building our own personal bucket strategy.

We are not certified financial professionals. For more information please read our Disclaimer.

Bucket Strategy Basics

Since finance professionals sometimes use terms the rest of us don’t normally use, we like that the bucket strategy term makes drawdown concepts more relatable and approachable. Basically, building a bucket strategy means identifying where the cash you’ll need over time would come from given all your accounts and your age. The goal is to intentionally position your accounts so your money is available when you need it, for whatever you might need it for. That includes current and near term living expenses, planned larger expenses like a car or home purchase, unexpected costs during emergencies, and more. Your bucket strategy can also help you identify where you should keep your equities for long term growth.

The standard thinking on bucket strategies today seems to be that most people would have 3 buckets…

- Bucket #1 = Cash (maybe 2 years of living expenses in a savings or brokerage account)

- Bucket #2 = Fixed income (maybe 3 years of living expenses in bonds, or CD’s, or other low growth but highly safe and accessible options)

- Bucket #3 = Growth (the rest of your portfolio in high growth investments)

…or something similar. You can find a baseline to start with and then make it yours!

Make it Yours!

If you like trying to read everything out there related to personal finance like we do you’ll find plenty of articles about 2, 3, or 4 bucket strategies. There are lots of variations out there and that’s a good thing, because what matters most is not following standard advice from others but instead figuring out what you need specifically. Buckets really are just a way to describe the accessibility of your money. The basic bucket strategy is very simplistic but the concept becomes more practical and useful if you overlay your account types, allocation plans, and timeline with your bucket strategy.

Our bucket strategy is nothing more or less than a description of our portfolio’s liquidity. Most of the bucket strategy examples we found were set based on timing, though there are ideas out there for setting up buckets based on other criteria. Our bucket strategy is arranged by time as a baseline (near, medium, and long term), but we aren’t overly focused on using a set schedule for our buckets. There’s no penalty for using our buckets out of order, as long as we aren’t disrupting essential long term growth. Our focus is on trying to be realistic about making safe withdrawals over an unknown period of time during market fluctuations we can’t predict or control.

We recognize the emotional aspects of our money so we also wanted a withdrawal plan that would make us feel safe by providing a roadmap for organizing our money, while also helping us manage our fear of not having enough. We know there will be bear market years during our long retirement as well as bull market years, so we wanted to serve up a bucket of financial success with a side of emotional benefits.

Our bucket strategy is a tool that helps us:

- Avoid selling funds during a down market,

- Maintain enough near term liquidity to fund five years of living expenses plus other cash needs as outlined in our Money Jobs,

- And most importantly, grow our portfolio over time so it will cover us when we’re elderly old ladies with more complex and expensive care needs.

How Do You Eat a Whole Cow?

First we organized our Money Jobs to include funding schedules whenever possible and grouped them into near term, medium term, and long term needs.

Then we looked at how accessible our accounts would be in relation to our ages over time. Knowing the order of accessibility of our personal accounts helped us start to build a framework for withdrawals from our 5 accounts (1 joint brokerage, 2 IRA’s, and 2 Roth IRA’s).

Since we retired at 44 and 54 years old our bucket strategy taps our savings and brokerage accounts first because they are 100% accessible now and always. We also did our best to make sure we had enough money in the brokerage and savings accounts to cover us at least until I’m 60, knowing at that point we will be able to also tap into my IRA. Without enough funds in our savings and brokerage accounts to cover those early retirement years we could have looked at one of several ways to access a 401k or IRA early.

But we are sticking with the plan that was simplest for us. We’re tapping our savings and brokerage accounts first, then we’ll turn on the spigot for my IRA when I’m 60, then we’ll add in Ali’s IRA when she’s 60, eventually we’ll dig into my Roth, and last we’ll get into Ali’s Roth as well.

Everyone has different account types, account balances, and their own age and health considerations. And everyone has their own goals, hopes, and dreams. Your bucket strategy WILL and SHOULD look different from ours or anyone else’s.

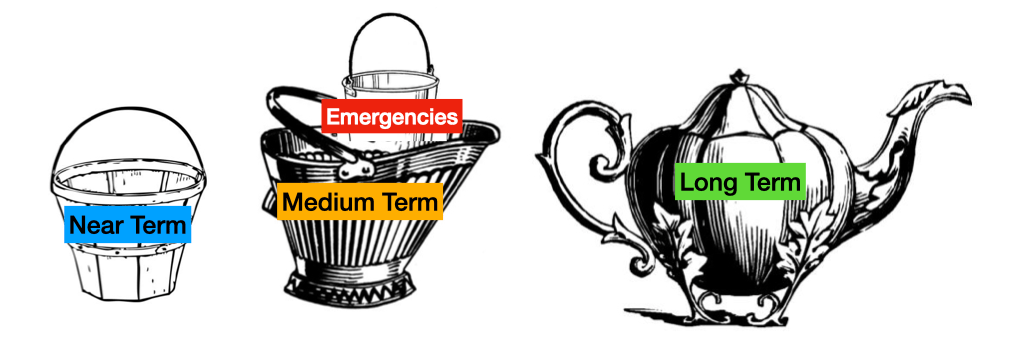

The AOC Bucket Strategy

The AOC strategy includes 3 buckets, though I always picture 3.5 buckets because we think of our emergency fund as completely separate from everything else. But technically our emergency bucket is tucked safely inside our 2nd bucket.

Bucket #1: This is our near term bucket. It covers our daily lives and includes most of our Money Jobs like groceries, water and electricity at our house, cell phone service, and credit card purchases. We also hold our Experience Money Job funds in bucket #1, for things like planned road trips to visit friends and family this year. Funds for this bucket live in our savings account, and we used this bucket exclusively in our first year of retirement.

Bucket #2: This is our medium term bucket. We set this bucket up to cover the Money Jobs we’re committed to paying for over the next 2 years, including a month long trip to Europe with our niece next summer, some remodel projects for the house we’ll be paying for over the next two years, and the new-to-us used car we bought earlier this year. This bucket also holds enough bonds and cash equivalents to cover 2 full years of living expenses in case the market is down when we want to pull out our living expenses at the start of a new year. These funds all live in our brokerage account and are currently invested in muni bonds and money market mutual funds. We were lucky enough to have strong return rates on CD’s for our first year of retirement but that changed so now we’re using bonds and money market funds.

Bucket #2.5: Don’t forget the all important emergency fund! We want to feel prepared for unforeseen emergencies that can come out of nowhere. Since we don’t have a crystal ball we can’t say exactly what future emergencies might occur, but we’re ready if a family member asks us to help them deal with an illness or other drama in their life (we tell all 6 of our nieces and nephews if they ever need us just call and we’ll drop everything to help them!). Or maybe a fire would force us to evacuate our home and live in an Airbnb for an extended period, or an accident could total our car. We definitely do have lots of wealth insurance in the forms of health, home, car, and umbrella insurance, but that doesn’t mean we are covered. In a best case emergency scenario we’d still need to pay for our needs up front during an emergency, and then later we’d likely be up to our ears filing claims and working with an insurance agent in hopes of reimbursements to cover whatever we were dealing with. Having “just in case” emergency money helps us sleep at night.

Bucket #3: This is the easy one! Our 3rd bucket holds the bulk of our investment portfolio. All of our looooong term equities live in this bucket, invested in a US Broad Market Index ETF and an International Index ETF. These 2 index funds keep us in diversified growth that will hopefully keep our portfolio compounding enough to cover all of our spending needs for another 60 years or so. This bucket does not represent one single account since the equities asset class is held across ALL our accounts. We’ll need to access different accounts at different times during our retirement so we want equities in all of our accounts. And yes we definitely have tapped some of our equities already because the market has been way up during our first few years of retirement. Sing it with me now, “If the market is up we’ll fund our annual expenses from equities!”

Getting Practical with Bucket #1

It might seem confusing at first but it’s a good thing that buckets can include funds from multiple accounts, and each of your real life accounts can fund multiple buckets. Buckets aren’t formal in the same way accounts are, they’re really just another way to visualize your money and your plans.

Bucket #1 is our busiest bucket because we use it every month, starting in January when we fund our savings account for the year from our Schwab brokerage account. And like our withdrawal song goes, we are ready for the market to be bullish or bearish at withdrawal time. We can fund our savings account when times our tough using our muni bonds and their tax free dividends. Or we can fund our savings account with equities when times are good using our US Broad Market Index ETF or our International Index ETF. We have both of those Index ETF options because we want to be diversified beyond the US. So far we have been lucky enough to make our retirement withdrawals during strong bull markets but our plan is ready for downturns.

After we withdraw our annual living expenses from our brokerage account we hold that one year of living expenses in our savings account, and chip away at it throughout the year. On the first of each month we transfer cash from our savings into our checking account to cover a full month of living expenses and we do all of our spending and bill paying from there.

We’re prepared to do some rebalancing during withdrawals if our allocation ratio is off by 5% or more than our current target equity ratio of 75%. And even though we set a general rule to pull money from bonds in a bear market and from equities in a bull market, we also have to know… how far up does a bull market have to be, and how far down does a bear market have to be, in order to really impact our withdrawal plans? We’ll talk more about our withdrawal strategies during bear and bull markets in a later post.

Why Do Some People Hate Bucket Strategies?

As we searched for articles focused on the mechanics of building a successful bucket strategy we noticed right away that those types of stories were hard to find. Some articles gave a brief overview of bucket strategies and then focused on the idea that this kind of portfolio management strategy alone can expose a portfolio to sequence of return risk (SORR) and the idea that selling equities during a down market is a no-no. Other articles voiced the criticism that some people might set their buckets up and then ignore the importance of annual rebalancing, failing to maintain their intended asset allocation over time. Those risks are not really about the bucket strategy concept but instead point to the risk of people not doing regular portfolio maintenance during retirement. Those risks are important for all of us to learn about and avoid, regardless of whether you use a bucket strategy or not. It’s true that if you fail to rebalance or fail to manage SORR, your portfolio could fail as well.

We can probably find flaws in any of the generic financial rules of thumb, if they don’t adequately consider someone’s unique needs and goals. For example, if you set up a bucket strategy and then spend down your long term growth funds early and run out of money, there’s obviously a flaw in your strategy. Your bucket strategy should not create conflicts with your asset allocation and rebalancing plans. Your bucket strategy can and should be designed to compliment the other important aspects of managing your portfolio.

We love repeating this idea — traditional retirement rules of thumb should all be changed and adapted to work for you, or discarded if they don’t work for you. That includes the 4% rule launched in this 1994 SWR article and re-launched in the 1998 Trinity Study, the 1985 Bucket Strategy concept, rules for what age you should be when you retire, generic allocation rules, and rules for when you should start taking Social Security. The only rule you should follow is this one: You are in charge of your money so set it up to do what works best for you.

Buckets Don’t Replace Rebalancing

Let’s just beat this drum one more time — It’s very important to remember that having a bucket strategy does not replace the need to rebalance your holdings at least once or even several times a year to get back to your target asset allocation. We currently target a 75/25 equity to bond ratio, with enough funds positioned in accessible savings and brokerage accounts to match our schedule for drawing those funds down. Make sure you figure out your ideal equity to bond ratio and stick with your unique plan.

So far we’ve been following the plan we created in our Personal Money Statement (PMS), and we check it often to make sure our plan still works for us today. We mitigate SORR through annual rebalancing on Ali’s birthday in May, and when we withdraw our yearly cash in early January. And we might also do some opportunistic rebalancing in response to a major market drop or spike at some point, but we haven’t so far. Other reasons some people might need to rebalance would be with the arrival of new money, like if you sell your house or receive an inheritance.

The more we can conceptualized the big picture of our portfolio, the easier it will be to manage our money. Understanding the big picture also gives our well managed portfolio a better chance of outlasting us.

A Side Note on Asset Classes

The three most common asset classes are equities (stocks), bonds (fixed income), and cash. Other asset classes include real estate, commodities, and cryptocurrencies.

For a more diversified portfolio we personally hold equities, bonds, cash, and real estate. And there are investment vehicles we aren’t interested in such as things we can’t touch (like cryptocurrencies), and things we shouldn’t touch (like natural resources).

Each asset class has its own baseline for risk and growth, and each will respond differently to market fluctuations. Our ability to continue living off of the growth of our total portfolio over time while funding our lifestyle annually depends on finding the right balance between all of the asset classes we hold. And what works for us might be different for you. The goal is to be well diversified and not handcuffed to the risk profile of one asset class.

Would You Like Your Salad First?

We think of our bucket strategy like it’s a fabulous multi-course dinner, spaced out with the best timing so we can enjoy every bite. Nothing should come out of the kitchen before we’re ready for it, and of course everything should be served at the right temperature for the dish. Our bucket strategy helps us line up our money in order of need so our accounts aren’t being emptied ahead of schedule.

Money Jobs help us determine timing, timing helps us determine which accounts to tap when, those accounts and their timing help us determine which asset types to hold, and checking our actual allocation at the moment of withdrawal helps us determine which funds to withdraw.

A Dash of Spreadsheet

We don’t need a ton of spreadsheet action in this post, but all of our Money Crush posts need at least a hint of spreadsheets! For the rest of this post we’ll be sharing examples from Jane Roe’s spreadsheet, just like we did in our last post in this series about Picking an Equity to Bond Ratio.

A few reminders about Jane:

- She is 45 years old, has no children, and is single by choice

- She was a high income earner during her career

- She reached financial independence in 2020, and plans to start early retirement in 2022

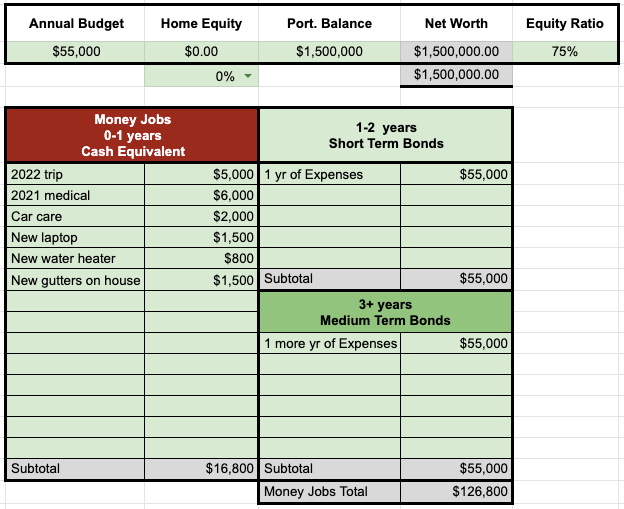

- Her post-retirement budget for annual living expenses (including taxes and health insurance) is $55,000

- She has $126,800 set aside in cash and cash equivalents to cover all of her surprise and experience Money Jobs for her first few retirement years

- Her total portfolio value is currently $1,500,000

- Her safe withdrawal rate (SWR) is 3.67%

- She saved 27.27 times her annual expenses before retiring

I plugged Jane’s numbers into our handy dandy spreadsheet to see how her buckets might need to look, how much money Jane needs in each bucket, and where asset classes need to live, based on her Money Jobs and her retirement timeline.

And since our bucket system is designed to function over a full calendar year, we’re pretending today is January 1. Jane’s plan is similar to our plan, to start each year with all of the funds she’ll need for the entire year in either cash or in whichever cash equivalents are hot at the moment such as money market funds, CD’s, or short term bond funds. These types of funds go up and down just like the market.

Ok so seriously, how did we build our bucket strategy?

Step 1: Calculate the Basics

Note your budget, portfolio balance, equity ratio, and the timing of your Money Jobs. Some people also consider home equity when building out their strategy but we don’t and Jane won’t in this example since Jane has no plans to sell her home at this point. At this point we’re focused on connecting Jane’s Money Jobs with her retirement timeline in the table below in order to identify the right accounts and asset types for her to invest in to maximize tax efficiency as well as accessibility.

The screenshot below shows the part of our spreadsheet where we entered Jane’s annual budget, portfolio size, and target equity ratio for allocation. This also maps out all of her Money Jobs with their separate timing in various locations. This step and this table are basic and simple by design. Jane’s goal is to make it as easy as possible to make a reasonable plan for when she’ll access her money. Jane knows she’s not handcuffed to these initial choices, they’re just giving her a place to start.

Step 2: Check Your Timeline

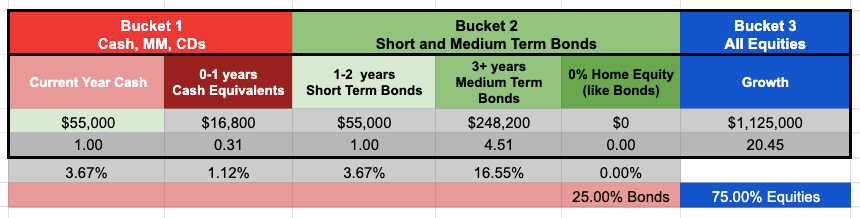

This step is more fun because it gets us into the magic of spreadsheet formulas. In the following table I entered Jane’s current year cash needs for living expenses. Then based on the placement of her Money Jobs in the Step 1 table above, along with her equity allocation, our spreadsheet divvies up Jane’s portfolio with the correct ratios in the correct buckets.

And boom! Below we see the beginning picture of how Jane’s buckets need to be set up based on her timeline, account types, and asset classes.

Bucket #1 is the simplest bucket. It holds cash and cash equivalents like mutual funds for the current year’s living expenses. This bucket also holds the additional cash needed for Jane’s near term Money Jobs like that trip to see her mom in November.

Bucket #2 holds bonds and bond-like funds that she might need to pull from should equities be down the next time she needs to fund Bucket #1 with cash for the year. This bucket actually holds all of her bonds and bond-like funds to meet her allocation goal for her total portfolio.

Bucket #3 holds all of Jane’s equities. This money is held in the form of low cost index fund ETF’s geared towards passively managed broad market growth.

Reality check!! If Jane needs to use Bucket #2 to fund Bucket #1 in a down market and replenish her current year living expenses, she will eventually have to replenish Bucket #1 AND Bucket #2 using equities from Bucket #3. And of course the plan would be to do that at a time when equities are up.

We have been lucky that equities were up at the end of each year in our real life retirement so far, and we know that trend won’t last forever. We also started our retirement years by selling our condo in Seattle, which gave us the cash we needed to fund our first two years of living expenses without selling any portfolio funds. Selling our condo actually helped us fund Bucket #1 and Bucket #2, including our emergency fund. If you’re able to start your retirement with enough cash to cover you for a few years without selling anything in the beginning, that’s a great way (a very safe way) to get the retirement ball rolling!

Now here’s the important part about Bucket #3, which is also the part that people like to argue about when they critique the basic bucket strategy concept… Our 3rd bucket doesn’t have a set timeline attached to it and it doesn’t need to, regardless of what some generic rules of thumb say. We’re not pretending we know what the future holds for us and we definitely can’t predict exactly what the market will do during our long retirement. Bucket #3 does not need to be sequestered for our use only after 10 years of retirement, or only after I’m 70 years old, or only when we believe we’re finally in the “no-go years” of retirement. Equities are a long term growth tool, but they must and will also supply current year living expenses throughout our retirement. Bucket #3 is organized for growth and it’s intended as a resource to refill the other buckets.

Step 3: Check Your Allocation

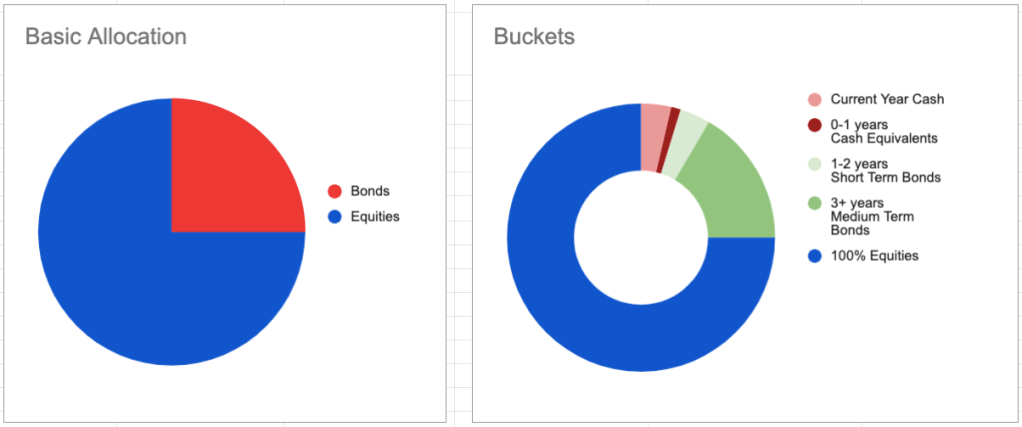

With a 75% equity ratio Jane’s basic portfolio allocation looks like the pie chart on the left below. Super simple!!! She’s holding 75% in equities for growth and 25% in bonds, cash, or money markets for stability.

The pie chart on the right helps us visualize her bucket strategy. Now we can see her funds teeing-up based on the timeline for her Money Job needs and the general asset classes she chose to invest in.

That’s it for now!

Designing a bucket strategy that meets your current, medium, and long term needs gets you in the ballpark to start dividing up your funds across all of your accounts. Analyzing your Money Jobs and the timing of your spending needs will help you pick the correct account and asset classes as you move through your retirement years.

Like any good plan, your bucket strategy needs to be flexible enough to change and adapt to real market fluctuations and your real life money needs. Your bucket strategy will need to change over time so it fits every phase of your actual life. Creating the right bucket strategy for you will bring financial and emotional stability. But, establishing and maintaining your bucket strategy does not need to be a difficult or time consuming task.

Please use Jane’s example as only an example, and be open to changing things to meet your needs. Maybe your Bucket #1 will hold 2 or 3 years of cash, and your Bucket #2 will hold 5 years of bonds. Your bucket strategy can be whatever you need it to be, because it’s YOURS!

In the next post we’ll look at how to pick funds from different institutions, how you might disperse your funds across your different accounts, and how you can use your buckets to build a wholistic portfolio allocation that meets your retirement needs.

I so enjoy your posts!

I think a key difference between your bucket strategy and the “bucket strategy” that is criticized by some is that the latter holds the first bucket of cash (and sometimes a second bucket of bonds) as separate from calculating the equity ratio. Doing so can mean that instead of having a 75/25 ratio, the unaccounted year(s) of cash skew the portfolio towards an unintended smaller amount of equities that can be a hazardous drag on long term growth (e.g. 75/25 with 3 years of cash might actually be 55/45 when the cash is accounted for in the calculations).

My understanding is that your way of looking at it puts that 75/25 allocation first, and distributes that “25” portion between cash in your savings account and bonds in your other (multiple) accounts, yes? That’s how I visualize my own portfolio now, and why a couple of my smaller old rollover IRAs are actually 90/10; because my large taxable account is 80/20 and I have a “short term” taxable account that’s 20/80 (equalling about 18 months of expenses), and I have about 9 months of cash. Individual accounts would give pause when not looked at in context, but when I add EVERYTHING up my net worth (like Jane, excluding my paid off house) is around 75/25, and that works for me.

One question that I have is regarding your annual January withdrawal. Could you explain your thought process around taking out a single withdrawal at that time, and then whittling away at it over the year, versus making monthly or quarterly rolling withdrawals and maintaining around 12 months cash in your savings account…? I’m thinking that also would allow for periodic rebalancing with each withdrawal?

If you may have covered this in a prior post my apologies! I’m not fully FI yet but getting there, and learn so much from your posts and how you detail your decision making process.

LikeLiked by 1 person

You are interpreting how we account for our cash correctly. It is part of our 25% bonds/cash. Regarding why we pull all the funds out for a whole year around the first week of January, for us it feels safer. We know that no mater what, we have our money for the upcoming year. It also means that we don’t “fuss” with our accounts as often. We have a total of 4 reasons to consider rebalancing: 1. Pulling out our year’s cash, 2. Ali’s birthday in May for general rebalancing, 3. If there’s a large swing in the market resulting in a +/- 5% shift in our E/B ratio, and 4. Any new cash. But since we look 2-3 years out regarding our plans, we set aside funds for larger goals or projects way ahead of time as part of our bond or cash holdings. It works for us. But thats not to say that someone else’s approach isn’t equally functional.

LikeLike

Thank you for explaining how you came to that decision! I too am firmly in the camp of doing what feels right and allowing yourself to sleep at night.

I think I would begin to get nervous towards the end of the year if I had just a month or two of cash remaining, but it sounds like your next outer ring of buckets handles that concern, too.

LikeLiked by 1 person

I wouldn’t say we get nervous towards the end of the year, but rather we start to feel like we’re “getting ready” to fund our next year. Right now we’re starting to think about what size of Roth conversion we can make for this year, and we’ll do that later in December before 12/31. Then on 1/1 we’ll determine how much we’ll be selling in equities or pulling from bonds to set us up for the coming year in 2022. It’s a chess game for sure.

LikeLike

Hello AOC,

I’ll jump in here. Thanks, first, for all your content. I’ve discovered you via the Plutus awards. The award is well deserved. Enjoy reading about your real world fire experiences. I fire’d myself in 2019. Learning as I go.

As far as the annual withdraw versus monthly or quarterly…timing the transfer of the money to pay the credit card bill was just a pain. It can be done and you’ll do it until you don’t. If you’re on vacation or with family or whatever it just catches you. I did it for two years, but in the end decided on; once a year, taking the amount I’ll need, minus the dividends that are predicted for that year, and pushing it over into a checking account. The diff between a savings and checking is minimal. I just put it in, checking. No more transferring money over and trying to maximize the amount of return I may get if that money was in the market.

Now if the bank could reach in and rebalance my account and pull out the money they need for my credit card each month…well, then I might go for it.

Great blog, AOC. Thanks for all your contributions.

LikeLiked by 1 person

Hey Steve, thanks for all that. Ya, I like having what I think we’re going to need ready to go throughout the year. I don’t want to have to mess around or worry about realizing I haven’t sold enough or too much. And I like to know what our gains are at the start of the year. Then I can plan around them. Sounds like you have a good strategy in place that’s working well for you. Nice!

LikeLike

Hi Alison- Great reading! Thank you so much for taking the time to write up all this. I guess I have always had a loosely defined bucket strategy between cash and medium and longer term investments but this puts alot more clarity into it. Thanks again for the great read.

LikeLiked by 1 person

Hi Fred and welcome. This has been a topic on my mind for a very long time. Trying to put some logic or structure around it helps us feel more comfortable managing our own portfolio. Our hope is that it helps others put more structure into their plans. Cheers!

LikeLike

This is amazing work! Thanks for the very detailed article, we are trying to calculate how much we need in each bucket to retire in about a year, and it’s a pretty complicated subject. Your explanations really helped.

LikeLiked by 2 people

Oh, thats fun and congratulations on your up coming retirement!!!

LikeLike

Thanks for sharing practical information of how to conceptualize and organize finances in the RE phase! Learning about this many years out takes a lot of the anxiety out of it. When I feel like planning, I add more sections or detail to the PMS that I created as a result of reading your blog. I figure that if I do this while it feels fun, it’ll be ready by the time it’s needed and without the stress of writing it all at once. Thinking to add a section that will plan out rebalancing and contributing income to smoothly transition from 90/10 to 75/25 or even 70/30 when it’s time to come out of the cocoon.

Have you ever taken advantage of tax loss harvesting? This is the first time I’ve been in a position to do it, but afraid of accidentally picking the wrong ETF to switch to and trigger a wash sale classification.

LikeLiked by 1 person

This sounds like a great plan. And working ahead on it will for sure reduce your stress.

LikeLike

I’ll join the other people and say a big THANK YOU for such great articles you write and they reflect more real life than other blogs and I always learn something new.

For example, now your article and Kate’s comment taught me that the ‘bucket’ strategy doesn’t account for the cash in the 1st bucket or ST investments, but AOC’s bucket does. I never knew that!! I admit that I haven’t studied intricacies of the Bucket strategy or what critics say, but I always imagined (or took for granted) that the AA covers all the buckets which comprise the whole portfolio. Of course, I wouldn’t put a pension or SS as part of AA because they are income coming not from your investments but which may allow you to be a bit more aggressive on the equity side in your FIRE portfolio. This is a good caveat for me to keep in mind and pay attention when other people discuss it.

Thanks

LikeLiked by 1 person

When looking at other streams of income like pensions or SS, we just subtract that amount from the amount we need to spend each year and the remainder is what we are want generated from our portfolio to withdraw. So if you spend $60K a year and you get $20K in SS or pensions, the needed income to withdraw would be $40K. We don’t have any pensions and we aren’t getting SS yet. So until we get SS, 100% of our income needs are being generated by our portfolio. And right now all of that is coming from our brokerage account. However, we do look at ALL our accounts when setting up our allocations and asset classes. And we do need to have both equities and some kind of bonds or bond like funds in our brokerage account until we can start tapping into my IRA. It’s a dance for sure!

LikeLike

As ever, so very much food for thought here! I read your posts at least 3-4 times before I feel like I’ve absorbed most of the points (and then revisit because it’s still so much good information).

I’m glad you specifically said that you have a rule about pulling from equities if the market is up, now I’m looking forward to reading how you actually pull your year of money. It also may lead to me re-organizing how I store money in my accounts… or rethinking how I will be pulling from them.

I’m curious about why you have an ETF instead of an index fund – I know they are close cousins, but I looked at them once probably 15 years ago and decided that index funds are for me (VTSAX specifically) so am wondering if I’m missing something. I did recently read that a person who wants to be an ex-pat can’t use Vanguard, but was able to shift index funds into ETFs and then transfer to an ex-pat-friendly company (maybe even Schwab) without causing a huge financial mess. I’m not planning to exit the country permanently, but that was an interesting tidbit to file away. Just in case!

LikeLiked by 1 person

You can get Index style funds as ETFs or mutual funds. They are similar but ETFs trade throughout the day and are a bit more tax efficient if you are holding them in a brokerage account. I’m not sure of the implications if you are moving abroad regarding either. Something else to research.

Stay tuned as we will be going through how we are organizing our fund locations in a future post in this series over the next few months!!!

LikeLike

[…] Part 3: Buckets […]

LikeLike

Love the detailed post…great job as always, thanks for being such a helpful resource for the FIRE community!

LikeLiked by 2 people

Thanks Sabrina! We really had a great time working on this post and we’re excited about the next one. Hope things are going well for you!!

LikeLike

[…] budget organized, you’ve picked your equity to bond ratio, you understand the importance of a bucket strategy, and you’ve outlined efficient fund placements, you’re ready to put all this information into […]

LikeLike

[…] No check out Part 3 in this series! […]

LikeLike

[…] Step 3: Buckets for Withdrawals […]

LikeLike