Every year in May we review our portfolio and take care of any major rebalancing that’s needed including changing, adding, or dropping funds. During our first full calendar year in retirement as May rolled around and it was time to rebalance we couldn’t find tools that worked the way we wanted without buying a subscription. So we gave ourselves a couple of retirement years to let our process evolve and we developed our own rebalancing tools. Now that we’re in our fourth year of early retirement and we’ve completed our annual rebalancing for 2021 we are officially comfortable with our system and ready to share a bit of how we handle this important aspect of managing our portfolio.

As many people have noticed and also commented on, we love to write dense posts and this one is a doozy, which is why we’re breaking it down into multiple parts. And from my perspective you really do need to have a handle on all of these steps to allocate and rebalance your portfolio.

- Part 1: Money Jobs and Budgeting

- Part 2: Picking an Equity to Bond Ratio

- Part 3: Buckets for Withdrawals

- Part 4: Tax efficient fund placement

- Part 5: Allocation and rebalancing

When I started working on this post I kept singing that creepy kids song that goes, “There Was an Old Lady Who Swallowed a Fly.” That song is really nightmarish if you think too much about it, but it reminds me of how one thing leads to another with our money. Personal finance topics can be linked like a sequence of events and it can really help to understand their dependency. In some cases you need to see the big picture of your entire personal finance strategy in order to effectively manage your portfolio. In our case we wouldn’t be talking about portfolio allocation strategies now if we hadn’t figured out how to talk about Money Jobs first, then bucket strategies, and finally portfolio allocation and rebalancing. And don’t worry, you don’t have to swallow a fly to make this all work!

We are not certified financial professionals. This post contains affiliate links. For more information please read our Disclaimer.

So here we go, let’s talk about Money Jobs…

Why Do We Need Money Jobs?

In our financial coaching sessions we’ve learned that budgeting is really a four letter word for many people. Lots of people have an aversion to budgeting and they’ll do just about anything to avoid using a budget. I confess that was me until 2014 when we found the FIRE (financial independence, retire early) movement. Reading about the different ways other people handled budgeting really made it hit home that we needed to find a way to track our spending too, so we could figure out how much money we needed to retire and plan the timing of our escape from full time work.

As much as we love all things personal finance, we don’t have CPA brains and tracking budget categories used to put us to sleep. We know there are other terms and phrases out there for the same types of budgeting concepts, but everyone is different and we all need to find the routine and process that works for us. If you have an aversion to budgeting the simple solution is to find a way to make the process fun for you. We didn’t want to build a budget but we did want to retire early so we needed a way of budgeting that gave us a clear picture of how our money could work for us so we could stop working and quit our jobs. That’s when we came up with the idea of Money Jobs!

It took us two years to identify all of our existing Money Jobs and then create our comprehensive retirement budget including post retirement costs for things we weren’t used to paying for out of pocket, like health insurance and taxes. Money Jobs gave us a way to track our spending, which led to outlining the budget we used while we were employed, which led to detailing our retirement budget, which helped us figure out our FIRE number, which led to the decision to retire early and finally to our resignations. That was our version of swallowing the FIREfly!

First, Keep it Simple

In the beginning we started a very simple routine of tracking our total spending every month by depositing a set amount into our checking account and then seeing how much money we had left after we paid all of our bills, including paying off our credit cards in full. We didn’t move on until we had a handle on this basic inflow and outflow of our funds, and it took about six months to wrap our brains around all of that.

Then we started reviewing our spending in more detail so we could be more aware of what we were doing with our money. We became more and more mindful about our spending every month as we built out our Money Jobs process. Instead of doing something dramatic we incrementally changed our spending, planned for more expensive months in advance, and built an evolving list of Money Jobs that helped us focus on our goal to retire early.

Second, Add Some Detail

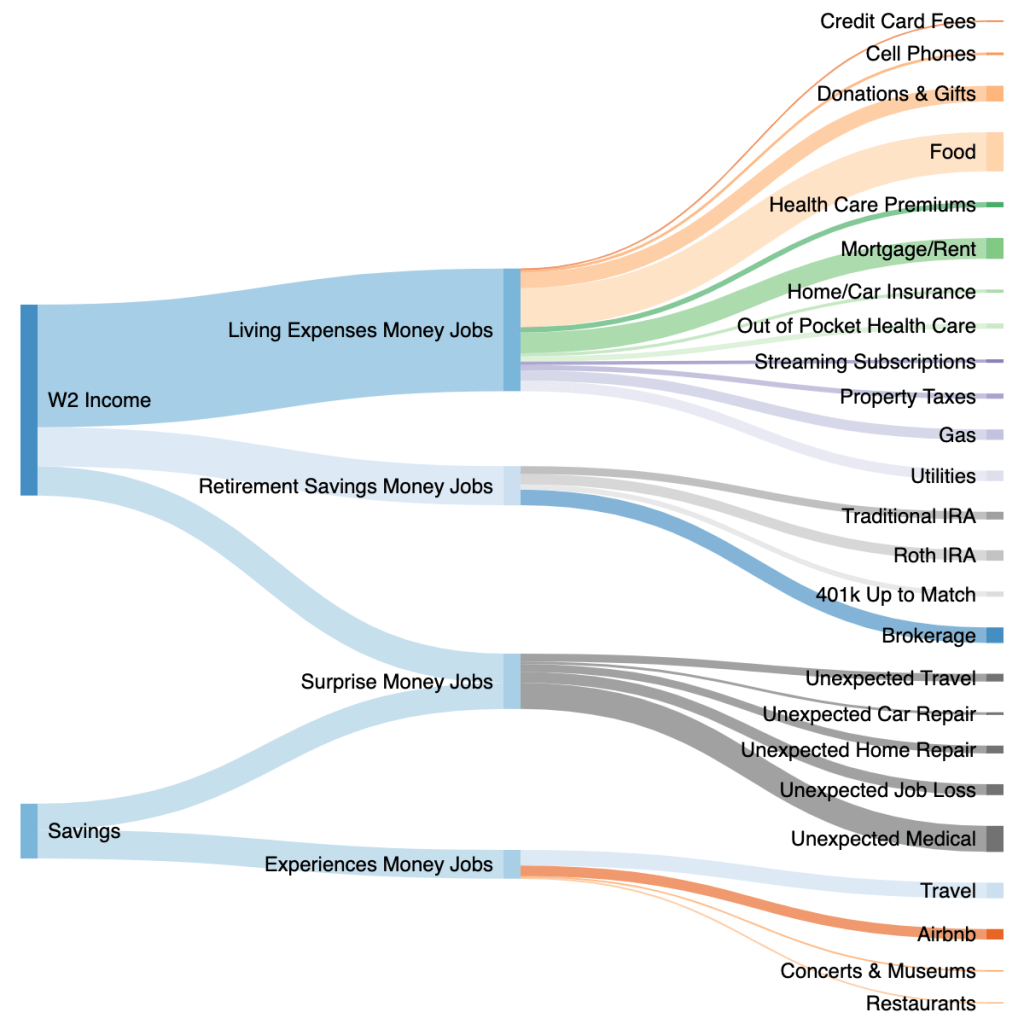

The next step in figuring out our Money Jobs was to add in more detail about our spending. We had four main categories for our Money Jobs and they were living expenses, retirement, surprises or emergencies, and experiences like travel. We looked closely at every account we had and each of our credit cards to figure out how all of our Money Jobs would be assigned.

- Our checking account was covering our recurring monthly bills and credit cards.

- We had a savings account to cover our travel plans.

- We had a second savings account for surprise expenses and emergencies.

- We had a third savings account for surprise expenses and emergencies in our rental properties.

- Our brokerage account was growing funds to cover our early retirement.

- Our 401k’s, IRA’s, and Roth IRA’s were growing funds to cover our traditional retirement years.

Third, Add Much More Detail

The next step in figuring out our Money Jobs was to add in much, much more detail by adding every single expense we could identify after a full year of tracking our spending. Leave no stone unturned and no dollar unassigned. Most of our spending fit under the Living Expenses Money Job category, including credit card fees, food, and housing.

Once you identify all of your Money Jobs it’s important to understand how you’ll fund them and where that cash will come from. If you’re still working you’ll probably fund your daily living needs, surprise or emergency needs, and retirement goals all from your W2 or other employee earnings. If you’re retired, those funds will have to come from a combination of accounts, depending on the types of accounts you have and how old you are.

Our Employment Phase Money Jobs

Our Post Retirement Money Jobs

Fourth, Some Money Jobs Need a Timeline

It also helps to give Money Jobs a due date or timeline if that’s appropriate. Some Money Jobs need to be funded by the start of the new year, others need to be funded by midyear, or once every few years. And if the Money Job is for retirement, like our 401k’s that’s especially interesting to give a timeline and a due date.

Assigning due dates or timelines to your Money Jobs will help you prioritize funding them. If you plan to buy a car and save the funds in advance, the deadline for that Money Job will coincide with the timing of your car purchase and then you probably can close that Money Job. If you plan to save for a trip every year it’s possible the timeline for that Money Job will change annually to fit the cost of that year’s trip and your schedule as well since one year you might travel in May and then next year you might travel in October. And you might always have a streaming subscription for movies and shows, but one year you might add Netflix and Hulu and drop Amazon Prime Video. You get the idea, Money Jobs can be as flexible as you need them to be to keep track of your goals and priorities.

Money Jobs Baseline

It does take self control, delayed gratification, and gamification to find an approach that works to track your spending and help you understand where your money goes every month. For some people like us it will take a little trial and error with different concepts, and for others just using something like Mint or YNAB will do the trick. Most importantly, don’t give up because there are a million options out there so each person can find a system that fits their own personal style and needs.

When we were still employed and had incoming cash we assigned Money Jobs to every dollar. Back then our Money Jobs included paying our utilities and other bills, building a sinking fund for surprises, building a vacation fund, and of course saving to replace our W2 income in retirement. Money Jobs helped us shift our mindset and get comfortable with budgeting and now we call everything we do with our dollars a Money Job.

To build your list of Money Jobs:

- Outline your recurring monthly expenses for basic needs like food, housing, and transportation.

- Add infrequent expenses for any bills you pay quarterly or annually such as IRS taxes, car insurance, or property taxes.

- Add your “optional” monthly or one time expenses for things like music and movie subscriptions, restaurant meals, charitable donations, admissions to parks and museums, etc.

And boom, those are your baseline Money Jobs. Once you create that baseline you can observe your spending over time and figure out what other details you need to track. It really did take us two full years of observing our spending habits to understand our expenses and outline our retirement budget. Remember that beating yourself up doesn’t help and try not to judge your spending. You can always change your spending habits and make improvements to your budget as you go. One thing to look for is if your credit cards have a higher balance than you can pay off each month. If that’s the case it’s really time to make some adjustments to your spending. As we watched our spending we made small adjustments to our habits like packing lunches for workdays and decreasing how often we bought restaurant meals. The goal is to stay out of debt and save extra cash each month that you can deploy for more productive Money Jobs.

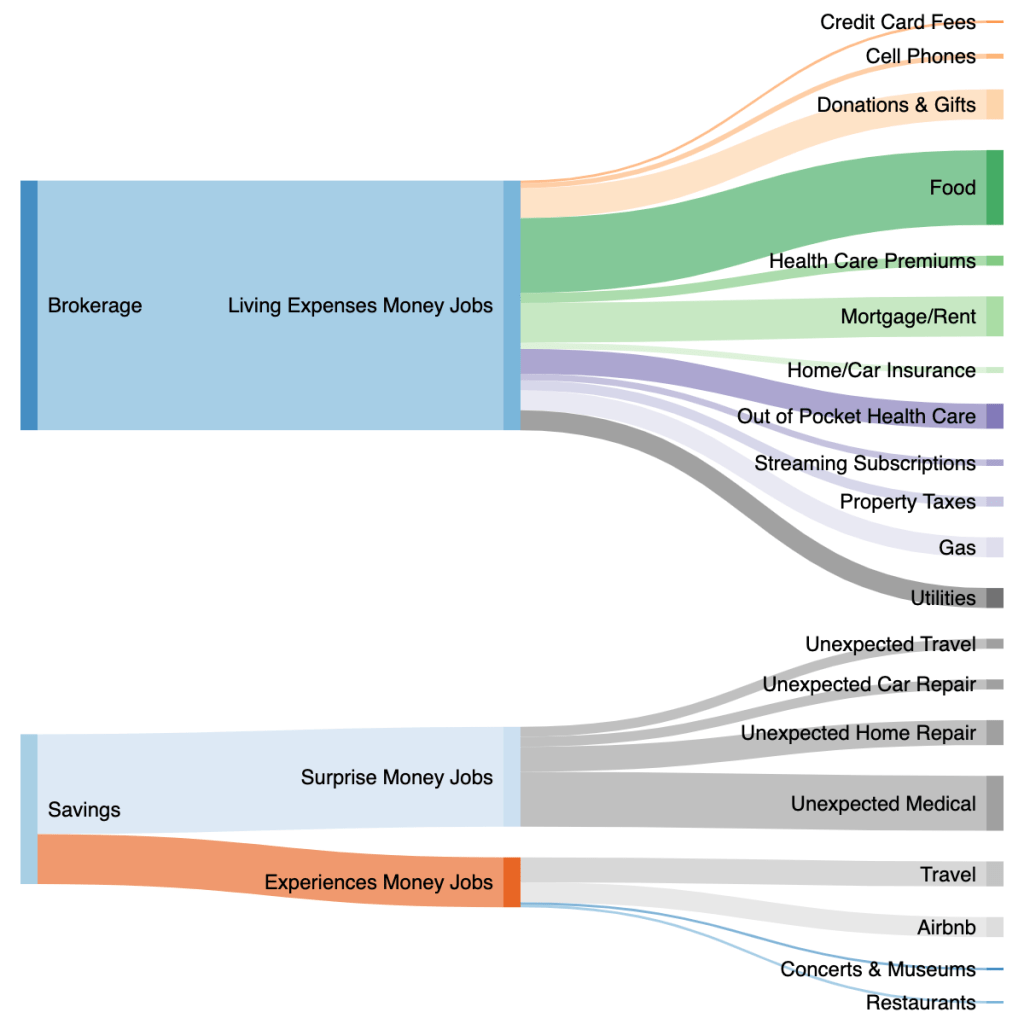

Surprise Money Jobs

As soon as you have your baseline Money Jobs covered it’s time to build emergency funds to cover things like a short-term job loss, an illness, repairs for your car, or a new roof. Those types of expenses are things we’d all rather not spend money on but if you do have to put a surprise or an emergency on a credit card things will be easier if you actually have that money ready in the bank when you need it.

Knowing you have money available for Surprise Money Jobs is a lot like knowing there’s a fire station just around the corner from your house. You hope you’ll never have to call them but you feel better knowing they’re there.

We kept funds for Surprise Money Jobs in a separate savings accounts so we could tell exactly how much we had available for each type of expense category. Sometimes we used extra cash from our paychecks and other times we were able to use bigger chunks of money from an employee bonus to top up our Surprise Money Jobs. It all depended on how urgent things felt and what our target dollar goal was.

Retirement Savings Money Jobs

Our favorite Money jobs were setting up the funds specifically for replacing our W2 income so we could stop working and retire. Putting a dollar amount on that kind of Money Job felt like a moving target because it was hard to know how much money we needed to continue generating enough income for us to live on in retirement. The amount of money we made during our careers fluctuated and it wasn’t always increasing since we sometimes had stagnant income amounts and even salary decreases to deal with. We knew the amount of money we would need in retirement would also fluctuate and we were especially concerned about being ready for increases in health care related spending as we age. Regardless of how much money you make we encourage you to avoid targeting a percent of your income to save and instead target a dollar amount because percents don’t always tell the full story of what’s needed or what’s allowed for each kind of account. Target an annual dollar amount to contribute each year that’s as close as possible to the limit for the account type you’re using.

If your employer doesn’t offer a 401k or similar option, as long as you have earned income and you’re under age 72 you can still save to a Traditional IRA, and as long as your earned income is under the IRS income limit you can still save to a Roth IRA. Double check the income and contribution limits for those types of accounts along with your eligibility based on your salary, and if a Traditional IRA or Roth IRA (or both) are right for you then do your best to max out at least one of those types of accounts each year.

If you do have a 401k through your employer find out whether your company matches your contributions. If that’s the case do the math to see the actual dollar amount your employer would match based on your salary, then do your best to contribute enough to get the full match each year. Beyond the match you can decide if it’s best to contribute more to your 401k or if your money will be able to work harder for you in a different account. Depending on how close or far away you are to retirement and depending on how old you’ll be when you retire, you might want to focus on trying to max out a Roth IRA since they are amazing vehicles for tax-free growth. So once you’ve hit your 401k match you can consider circling back to max out a Roth IRA.

The other option you have for your Retirement Savings Money Jobs is a brokerage account. We love our brokerage account because it’s so easy to use. There’s no limit to how much you can save, no limit to when you can contribute, and no restrictions for when you can access your money. And if your brokerage account investments have been held for over 12 months the gains are taxed at a more favorable capital gains tax rate.

Experiences Money Jobs

After all of the important Money Jobs are taken care of you can consider setting money aside for experiences. Maybe you want a new set of hiking boots and a trip to Spain so you can walk a portion of the El Camino de Santiago. It’s important to save time and money for experiences that will improve your life including spending time with friends and family, attending special events, traveling around your home country, and visiting other parts of the world.

Back in 2012, Ali and I agreed that we wanted to take a 3-4 week trip every two years so we created an account for Experiences Money Jobs and gave ourselves two years to save the money we needed for bigger trips to Europe. When we had the money ready for our first trip in 2014 we traveled for four weeks in England, France, Italy, and Scotland. After that we replenished our Experiences Money Jobs account and took a three week trip to France in 2016 so we could see different parts of that country. And after that we replenished our Experiences Money Jobs account again and right away we booked a three week trip to Germany, Austria, and Switzerland for early 2018. Each of those trips was amazing and we met new friends along the way. We also gained a greater appreciation for the world on those trips which led to our decision to become full time nomads when we retired.

Whatever your passion is, feed it, plan for it, and look forward to it by making it a Money Job.

Paying Bills

As we developed our list of Money Jobs we were also able to simplify our bill paying process. Since we had already decided how much of our salary we wanted to save in our retirement accounts we knew exactly how much take home pay we had left to work with each month. Our goals were to live within our means and also find more money to save in our Retirement Savings Money Jobs including traditional retirement accounts and our brokerage account.

To help simplify things we:

- Paid as many bills as possible with one credit card using autopay if possible. We also paid for things like gas and groceries with the same card. By consolidating most of our bills in one place it felt like we really only had one bill to pay. Using one credit card, Ali’s Chase Sapphire Reserve card, also helped us earn travel points to fund future travel plans. Depending on the size of our monthly credit card bill we sometimes had to transfer extra funds from our main savings account, but as our spending came down to fit our new budget, this was less and less necessary.

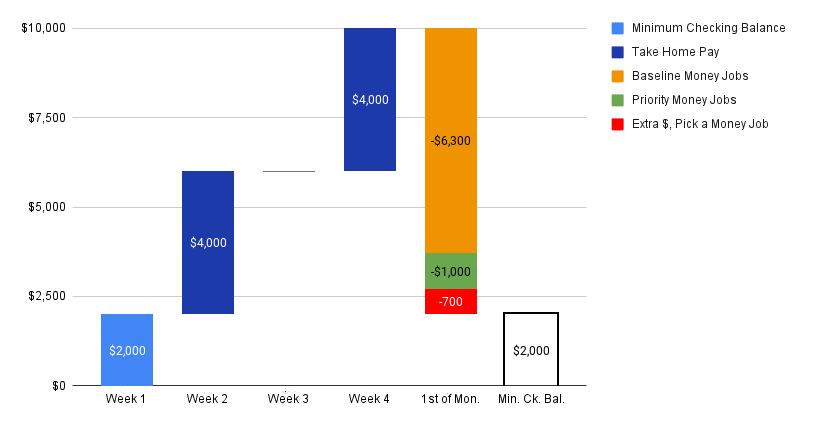

- Kept a predictable balance in our checking account, with an additional buffer. For the most part our paychecks were predictable and we didn’t get a ton of bonuses. But we always kept a minimum of $2,000 in our checking account to cover unexpected checks or expenses, and also give us peace of mind that we were not risking overdraft issues or fees.

- Paid any and all credit card balances in full on the 1st of the month. We started paying our credit cards on the first of the month in full which meant we never had late fees and we could manage when we wanted to make our payments instead of running on the schedule suggested by the credit card company.

- Tracked all of our bills and their timing, including less frequent bills. This allowed us to then transfer over funds from our main savings account to cover those payments since we had been putting funds aside for those Money Jobs ahead of time.

- Save the extras. After we paid off our credit cards and other bills we checked to see if there were any remaining funds in the checking account. If there were extra funds beyond the minimum balance we had agreed to carry in our checking account, which was $2,000, any bonus funds went towards our savings or investments.

Every month we let our checking balance build up from our W2 incomes. We paid ourselves first through payroll deductions right into our 401k’s and Traditional IRA’s. Then on the first day of each month we paid all of our Baseline Money Jobs and covered our living expenses, followed by some money going to our Surprise Money Jobs until those accounts were topped up in case of emergencies. Then we moved some money over to our Experiences Money Jobs to pay for the next trip. Lastly, everything left in our checking account above our $2,000 minimum balance moved to our Retirement Savings Money Jobs in our brokerage account.

Some people call this a Zero Balance budget where you subtract all of your expenses or Money Jobs from your income and the remainder should be zero. We assigned every dollar coming into our accounts with a Money Job and had zero dollars left unassigned. I loved paying the bills every month because our Money Jobs concept took the stress out of the process and also allowed us to find more and more money to save for retirement.

No matter what you call it, this way of approaching your bills can be really helpful. It can take several months to set your system up depending on the bills you have and the available savings you have as well. But you can also just leave extra money in your checking account until you build up the target minimum you calculated.

Nurture Your Plan

Our Money Jobs are still doing the hard work for us now that we’re retired, just like our little food garden in the backyard. We had fun getting a glimpse of how simple our finances could be while we were traveling full time with almost no bills to pay for two years. And now that we’re homeowners again and living in one location we’re back to a version of budgeting and bill paying that looks a lot like when we were still employed, though things are different since our only income comes from our portfolio.

Regardless of what you call it, Money Jobs or a budget or something else, managing your life and your money will serve you well over time.

Pick the approach that works for you and especially pick the approach you know you can stick with. And if you’re not able to follow your first plan don’t give yourself a hard time, just reevaluate things and make some small changes that help you keep trying. Be patient and surround yourself with information and people that support your goals. It will take time because a good plan always does but, the more you learn and understand about how to make your money work for you the better your life will be, now and in the future. You can do this!

The next post in this Portfolio Allocation series will focus on risk vs growth and how that relates to picking an equity to Bond Ratio.

(hope this doesn’t show up twice, WP is being a little funky)

I really like the way your combined brains work! I am also very grateful you’re doing three posts on this (eventual) topic because there is a LOT to ponder here.

I’ve tracked my expenses for 14 years but in a lot of ways it’s still very slushy. For example I’m about to get a root canal (you’re envious, I know) and have the money to pay for it, but haven’t decided if I’m pulling it from the bills account (the most appropriate, but the one that runs a little lean) or from a different account that is technically dedicated to other future spending, but in reality often covers some ready cash situations like this. Since I’m one person/one income, I don’t get TOO fussed about account accuracy, but maybe I should think about money jobs more in-depth.

I am curious that you only show unexpected car repair, unexpected home repair. I don’t see another bucket for anticipated car/home expenses (like new tires, buying a piece of furniture). Would those fall into the unexpected bucket as well? I am not criticizing, just curious, and wonder if your expenses are a little slushy too. I’m posting this comment after only reading half – I need to pause and come back – so if you answer that lower down, please feel free to not answer, I’ll finish reading the post later today!

LikeLiked by 2 people

We didn’t get into major detail about the categories we use for which expense. The idea is that Money Jobs are highly customizable and you can go as loose or detailed as you’d like. It’s about making a system that works for you and that you can follow and be on top of long term. But in the case of unexpected car issues, we would take money for new tires out of that Job. The unexpected part for us is “when” we would need to get the new tires as we would expect to have to get them at some point. The overarching idea is that everyone should track down all those kinds of items and endeavor to put some money aside regardless. And if we don’t use those funds in a given year, we roll them into the next.

LikeLike

That makes sense! I like the idea of a fund for unexpected-but-will-happen expenses, rather than kind of rummaging around to decide where the money will come from every time something comes up.

LikeLiked by 1 person

Love all the Sankey graphs! I’ve been tracking my own expenses for the last five years and still get surprised sometimes at the data. Example: I had thought my expenses were creeping up each year until checking things out on Mint; since May 2018 my spending’s been consistent except for 5 of those months (or roughly 12% of the time). A lot of folks are money avoidant for a number of reasons, but it really does pay to be mindful about budgeting and giving each dollar a job to do.

LikeLiked by 1 person

Hey Guac! I love those Sankey graphs. It goes with my feeling about how things should “flow”. And when every dollar has a job I can sleep at night. There are so many ways to track our money. And fun to hear you’ve been using Mint for so long. I know someone who’s been tracking with Quicken for 20 yrs. Crazy!!!!!

LikeLike

Great perspective as always! Totally agree about developing a system that works for you. It took us a long while of tracking expenses to get our system down, but now we actually really enjoy the process. Looking forward to the next chapters!

LikeLiked by 1 person

Its nice to hear we weren’t the only ones to whom budgeting didn’t come naturally. The key is to keep trying and don’t give up. Getting a handle on just this one things leads to some much more control in ones life. And with control comes choices. Cheers!

LikeLike

Great post. Thank you for going into details on your budgeting setup. Looking forward to Part 2 and 3.

I have a similar system except for not having dedicated savings account for each money job. I just use a spreadsheet to partition the savings account balance to different money jobs and save for each every month. This way I can have any number of money jobs without having to open multiple savings accounts.

BTW Ally has savings goal feature that sounds somewhat similar.

LikeLiked by 1 person

We only have 2 savings accounts at this point. And each one is doing very specific jobs. One is a catch all for multiple smaller money jobs and one is where we keep our funds for daily living expenses. That way it’s easy and fast to see “how we’re doing” on our spending and our budget. That one account has an auto transfer at the start of the month just like a pay check. The other account holds the funds for say emergency new tires or a new hot water heater. There are lots of institutions that have features to help folks save. We have all our accounts at one place for ease of access at any time. Cheers!

LikeLike

I’d really like to play with Sankey charts at some point, they look so fun!

I manage our money with the same ideas: we save specific dollar amounts through paycheck withholdings first, then set dollar amounts for taxes, and our brokerage. We get to spend what’s left after all the savings but since expenses can and will change (daycare coming up fast), I enjoy the occasional retooling of the tracking process or the numbers to see if I can squeeze a little more savings out. Or let up my reflexive chokehold on the budget 😉

LikeLiked by 1 person

Keep working on finding the balance that works for you and your family!!!!!

LikeLike

[…] It’s clearly time to make an adjustment. We are proud personal finance nerds so we agreed that we needed a new Money Job in our budget specifically for mental health counseling which fits with every other health related Money Job we […]

LikeLike

[…] As we write this post Jane is in the process of figuring out her comfort level with risk so she can create her equity/bond allocation strategy. Of course Jane has already built her Money Job system to help her budget for annual expenses, but if you missed that first post in our Allocation Strategies series you can find that Money Job post here. […]

LikeLike

[…] Maintain enough near term liquidity to fund five years of living expenses plus other cash needs as outlined in our Money Jobs, […]

LikeLike

[…] our current and near term living expenses as well as planned larger expenses, as outlined in our Money Jobs. Other funds in our brokerage account will cover unexpected costs during emergencies. And most […]

LikeLike

[…] Step 1: Money Jobs and Budgeting […]

LikeLike

[…] first parameter was our budget. We took the remainder of our home remodeling cash and gave it a new Money Job to buy a van or trailer. Of course we didn’t have exactly $50k but that’s the amount we […]

LikeLike