One of our main investing goals at this point is to choose tax efficient funds with low fees and modest growth to hold in each of our accounts. Some funds in our brokerage account will provide accessible cash to cover our current and near term living expenses as well as planned larger expenses, as outlined in our Money Jobs. Other funds in our brokerage account will cover unexpected costs during emergencies. And most importantly, we need funds for growth and longevity in our IRA and Roth accounts specifically for a long retirement. Ideally, everything we hold will provide us growth and stability all while being tax efficient.

We are not certified financial professionals. For more information please read our Disclaimer.

When we retired early we owned a variety of investments including individual stocks but since then we have vastly simplified our portfolio holdings. We now concentrate the majority of our investments in ETF’s as they trade throughout the day, can be very low cost, are more tax-efficient, and come in various asset classes. Our current holdings include a US Broad Market ETF, an International Equity ETF, a Short Term Bond ETF, and a Muni Bond ETF.

But how do you know which asset types are best for each account type in order to have a diversified tax efficient portfolio? Well, it depends! I know that’s not a popular answer, and I hate hearing that too. So let’s back up and focus on taxes first.

Tax Efficiency

No matter what kind of assets you own you will have to pay taxes on appreciation at some point. Maybe you’ll owe taxes on the dividends your funds produce, or on the capital gains realized when you sell funds. Some assets generate lots of dividends and others none. Some assets appreciate a lot but even then you don’t pay taxes on appreciation until you sell. And depending on the type of investment account those assets are in, you might have to pay taxes only on the contributions while the dividends or capital gains could have taxes due either NOW, LATER, or NEVER!

When people ask which assets are the best, or which accounts certain assets should be held in, the answer is… It depends. It depends on your personal investment strategy. It depends on the kinds of accounts you’ve been able to open and contribute to over time. It also depends on which investing phase you’re in, accumulation or deccumulation/longevity. Regardless, building a portfolio that lasts as long as you do is key.

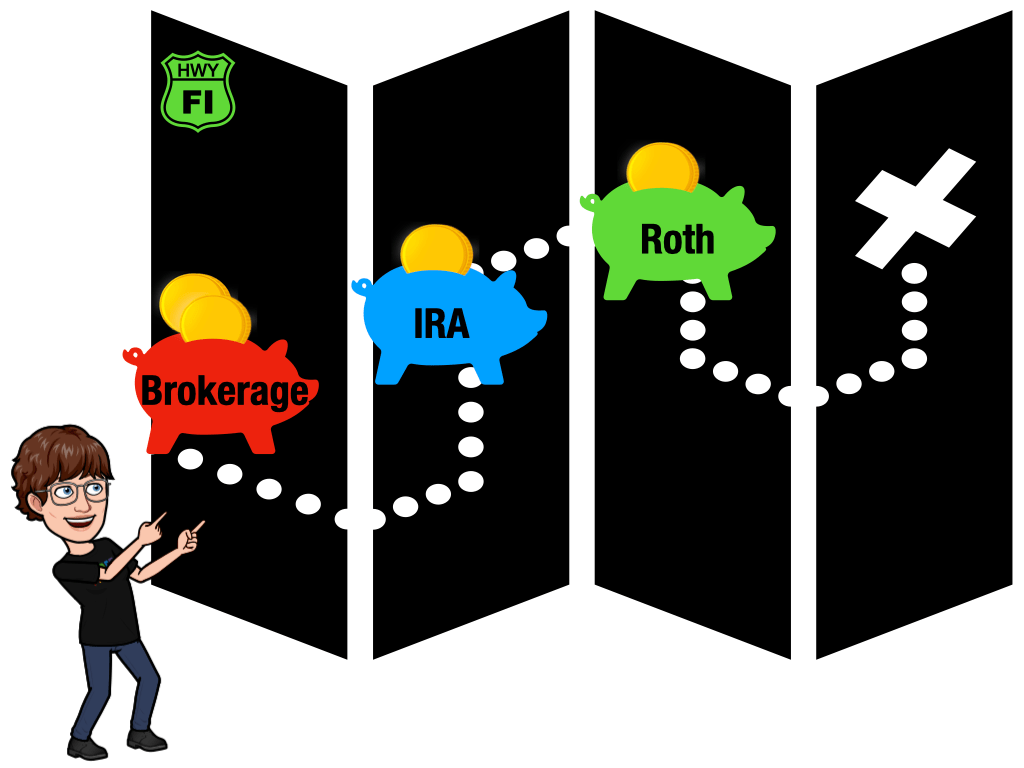

Now, Later & Never Accounts

Now – Taxable Brokerage

Since we’re in our early retirement years and we don’t have access to our IRA’s or Roth’s yet, we’re using our brokerage account to fund our current lifestyle. Because of this, we have to pay taxes on any gains and dividends NOW when we withdraw our annual living expenses. Since we’ve held the assets in our brokerage account for over 12 months we pay taxes on realized gains at the long term capital gains tax rate of 0%, as we keep our total income under the 0% capital gains bracket of $80,800 and our filing status is Married Filing Jointly (MFJ). It doesn’t get any more favorable than that!

Later – Tax Deferred IRA

When we were still employed we contributed to 401k’s and once we retired we rolled those over to personal IRA’s. We won’t start withdrawing funds from my IRA until after I’m 59.5 years old so those funds and their taxes will come LATER. And since Ali is 11 years younger than me and we won’t withdraw funds from her IRA until after she’s 59.5 years old, those funds and their taxes will come much LATER.

For now we can buy, sell, and receive dividends in our IRA’s without paying taxes on any of those funds, as long as we don’t make any withdrawals. When I’m 60 years old we’ll start pulling our annual living expenses from my IRA and at that point we’ll pay taxes for those withdrawals at our ordinary income rate. The tax brackets will change before I start making withdrawals but for now we’ll assume they’ll be similar to our current bracket, which is 12% and tops out at an income of $81,050.

Never – Tax Free Roth

We also opened Roth IRA accounts and started contributing to those during our working years. Amazingly, we can buy and sell securities and receive dividends in those accounts and NEVER pay taxes on any of those funds again. That’s because we’ve already paid taxes for all contributions and conversions in our Roth accounts. Done!

We’ll have full access the funds in our Roth accounts after we are 59.5 years old, which fits perfectly with our investment and withdrawal strategy. In fact, we’re glad to have the extra time to convert funds from our IRA’s to our Roth’s and pay taxes on those funds during our early retirement years while we’re in a lower tax bracket. In our case, making annual Roth conversions and paying taxes on those funds now helps us moderate our lifetime tax obligations by reducing our future RMD’s.

Which Accounts Do You Have?

We all have to pay our taxes! The goal is to position your portfolio with the least possible amount of drag from taxes in order to allow for steady growth. Over time it will be important to understand and plan your account types and the kind of taxes they’ll be subject to. You’ll also need to understand which investment types and asset classes you want to hold, along with any costs and fees associated with them, and what kind of growth, stability, and dividends they’ll produce.

There’s more than one way to create a balanced investment portfolio. And if you’re like us your portfolio will look different depending on whether you’re in the accumulation or deccumulation/longevity phase.

Regardless of what your specific investments might be, if your goal is to save enough money to fund your retirement years then retaining as much growth as possible by paying fewer taxes over time is a good strategy. One of the best ways to reduce your tax obligation is to optimize which accounts you hold each asset class in. And over time as life changes you can make adjustments to your portfolio so your money can continue to grow, be protected, retain value after withdrawals, and keep enough momentum to last as long or longer than your life expectancy.

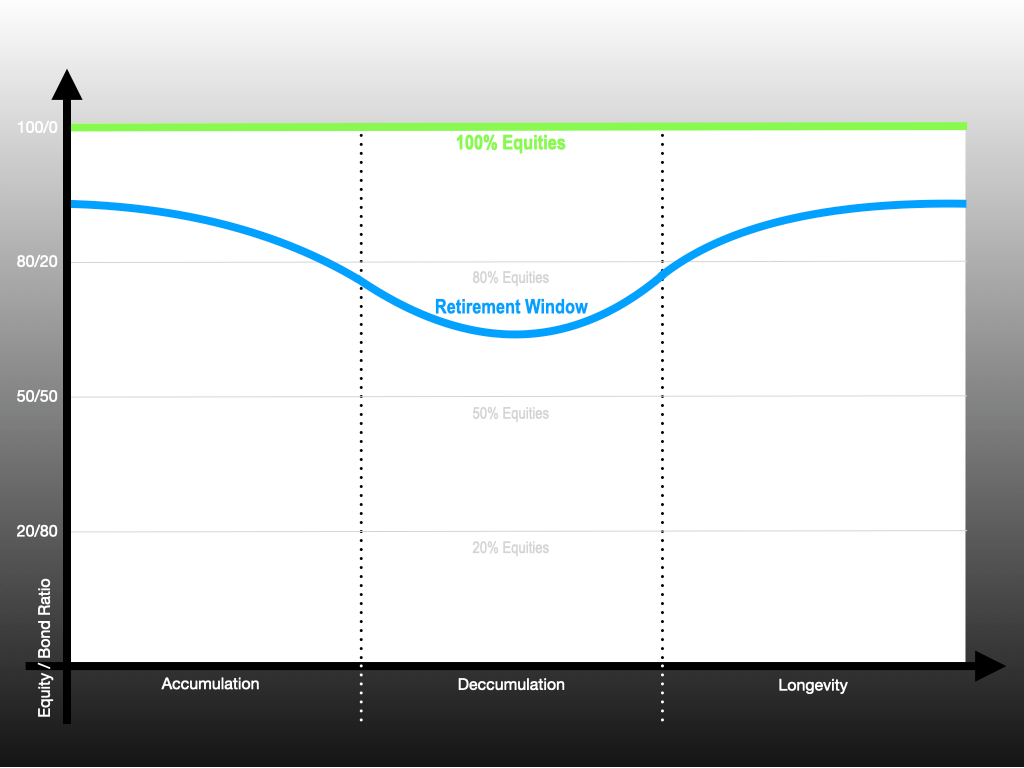

Investment Phases

Accumulation

In general we’ve seen people saving for retirement using these common tax advantaged account types: 401k, 403b, 457, traditional IRA, Roth IRA, and brokerage accounts. People typically don’t access funds in their traditional retirement accounts like a 401k or 403b before they reach 59.5 years old. Early withdrawals can trigger an IRS tax penalty of 10%, which is bad enough. Even worse is that early withdrawals can cost you the compounding gains those accounts are designed to create over time. Holding equities in those accounts for a longer period of time allows for compounding growth and the bonus of not paying taxes on growth or dividends until you start taking withdrawals in retirement.

In general, there’s no need to hold bonds in any of your accounts during the accumulation phase, since the goal is long term growth when no withdrawals are needed. But there’s a lot of value and security in holding accessible funds for emergencies during the accumulation phase. The cash equivalents you might hold for emergencies could include bonds, money market mutual funds, or CD’s (depending on how they’re performing at any given time). Since these funds need to be accessible they could be held in high yield savings or brokerage accounts.

If you intend to retire early before you’re 59.5 years old like we did, investing in a brokerage account can be critical because it’s always accessible regardless of your age. You can hold broad market equities as well as bonds in a brokerage account without needing to pay taxes on unrealized gains until you sell shares, except in the case of dividends. And depending on your ordinary income tax bracket it’s possible that your dividends could be taxed at the far more favorable capital gains rate of 0% (like ours), or the higher capital gains rates of 15% or at most 20% which are still relatively favorable as well.

When we were in the accumulation phase we bought, held, and sold individual stocks in our brokerage account. We also invested in mutual funds in our 401k’s, and we were even known to do a little swing trading in our Roth’s. If we could go back in time we’d still try all of that since those lessons were all important parts of our financial education. We loved trading daily and weekly along with the investment classes we took and the investment club we joined. But if we could have a do-over during our accumulation phase we’d skip ahead much more quickly to holding only indexed US Broad Market ETF’s and International Equity ETF’s. That strategy would have kept our focus on generating diverse, indexed, low cost, long term growth without as many dramatic ups and downs.

Deccumulation

When you’re ready to retire it’s a good idea to shift a percentage of equities into some kind of bonds within the account you’ll be accessing to fund your first few years of retirement. Bonds are critical in retirement since they have the stability to help you avoid sequence of return risk (SORR). They can help you build protected funds in case your equities are down in those early years. Brokerage accounts are excellent tools for early retirement years so make sure some bond funds live in your brokerage account if you plan to fund your retirement lifestyle from there.

Now that we’re retired and in the deccumulation phase ourselves, our investment strategy includes holding a short term bond ETF and a muni bond ETF in our brokerage account. This strategy allows stability from bonds that hold value when equities are down along with very low fees. And most muni fund dividends are tax free!

As you approach age 59.5 when you’ll be old enough to access your tax deferred accounts like a 401k, 403b, IRA, or Roth, it’s time to introduce some bonds to those accounts as well, based on your predetermined asset allocation and equity to bond ratio. The idea is to always have access to some kind of stable bond fund in the account you’re drawing from to avoid selling equities if the market is down when you need your funds.

Longevity

Longevity isn’t a completely separate phase like accumulation and deccumulation, it’s a concept that needs to stay at the forefront of your strategy during all of your investment phases. But I still like to think of longevity as the 3rd and final phase of our investing journey.

Managing longevity is about balancing growth with withdrawals. It’s a bit like making sourdough bread because you never want to use up all of your starter. You need to keep enough starter tucked away and growing so you can take a little bit each time you make a loaf of bread, always leaving enough starter growing basically forever. You have to keep your starter healthy so it will keep compounding, just like having enough equities will keep your portfolio compounding.

Since current generations are living longer we know Social Security is most likely not going to cover all of our expenses during our later years, especially due to inflation. That means the savings we put aside has to grow and last longer as well and holding a higher percentage of equities is especially critical for growth in today’s low interest rate environment.

As you begin drawing down your portfolio the goal is to withdraw lower percentages (less than 4%) in order to retain sufficient growth. The goal is to hold enough equities for sustainable growth while retaining enough bond funds to be able to rely on them when markets are down, but not enough bonds to keep your portfolio from riding the natural direction of the market… which is UP!

Using the most tax efficient account for each kind of asset during each phase of your investment life will help you manage your tax obligations and reduce the overall drag on your portfolio over time. Managing your tax obligations along with managing your yearly budget should allow you to retain more growth.

Remember, there is no one size fits all when it comes to this process. Stay aware of what you own, understand how and when your funds will be taxed, and pick the best account during each investing phase to hold assets for accessibility, growth, and wealth preservation. This is an ongoing process of improvement over time, as you continuously learn from the past and become a bit more confident and efficient each year.

Diversification

One of the best ways to manage risk in a portfolio is through diversification. If you’re holding different asset classes like US equities, international equities, bonds, and real estate, when one of them is down the others might be up. This is also known as holding uncorrelated assets.

If you were building a portfolio of stocks and wanted uncorrelated diversification maybe you would pick a bank stock, a cruise ship stock, a consumer goods stock, and a big tech stock since those stocks are not in the same industries or sectors, or serving the same clients. When Covid became a global pandemic cruise related stocks mostly dropped in value while tech stocks continued to perform well. Holding a selection of uncorrelated assets can protect your portfolio from the ups and downs of different industries.

You could also diversify your portfolio with uncorrelated assets outside of the stock market, such as real estate and/or your own small business or side hustle. If you’re interested in real estate you could invest in a personal home, long term rentals, vacation rentals, or a real estate investment trust fund (REIT). REIT’s are probably the simplest of those options since they can give you access to commercial or residential rental properties and income through a mutual fund or ETF.

The old advice that you shouldn’t keep all your eggs in one basket is still very true when it comes to building a diversified portfolio. Better to divide your portfolio up into different asset classes to protect your total portfolio from sector specific drops while still exposing it to strong sector specific growth.

But how do you make sure you have enough diversification? Well, you can do the research to find stocks you’re comfortable with, then buy those individual assets, track their performance, and continue to buy and sell them based on the criteria you’ve formulated for your own risk profile.

Or you can buy a large broad market fund that self-manages its holdings over time, which is much less time consuming and far less stressful. We love indexed broad market ETF options since healthy stocks are continuously added to the fund as companies do well and unhealthy stocks that are underperforming are dropped, all while you do nothing. When you buy a broad market index fund you’re investing in a variety of healthy stocks for that fund type, which takes the guesswork out of investing.

There will be people you run into during your investing journey who try to push their favorite stocks and sectors because they believe they’ve found the golden egg. But how do you know if they’re right? Research has shown that over time broad market index funds outperform both managed funds and individual diversified stocks. And sure, some people hit a home run when they bought early shares of Apple, Amazon, or Tesla. But home runs are never guaranteed and it doesn’t take a home run to be a successful investor.

Just remember the 2021 World Series winning Atlanta Braves had a batting average of only .244, with 239 home runs in their 2021 season. They were not the best in the league in any category. They ranked 14th for hits and 20th for at bats, with only a 2.9% chance of hitting a home run each time they approached the plate. Not very good odds if you ask me, and yet they still won the World Series. Some people have investing strategies that sound like baseball stats, they’re always looking for individual stocks that have a chance of performing like home runs. We know from experience that kind of strategy can be thrilling, but it’s not very dependable. That’s why we stick to consistent, steady, diversified investing which has been far more satisfying and fruitful for us over time.

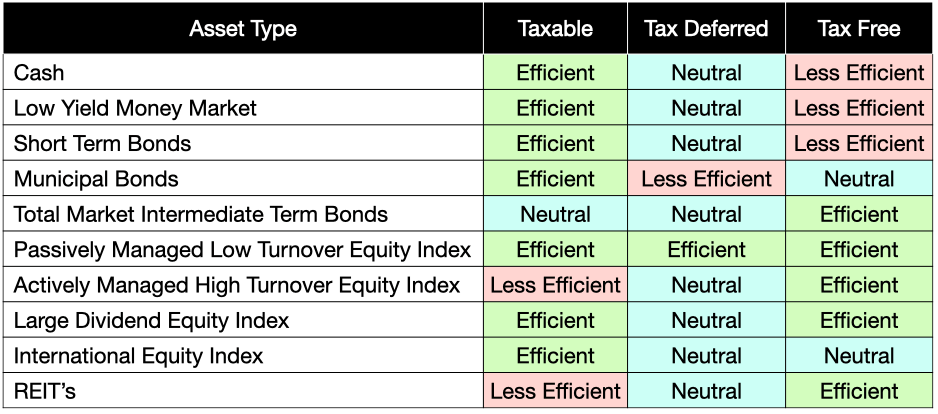

Basic Asset Class Funds

Once you have drunk the kool-aid of simplified and diversified investing using indexed mutual funds or ETF’s, you can focus on how to place the right funds in each of your accounts during each investing phase to minimize tax drag and maximize long term growth.

Efficient fund placement is all about how taxable a particular fund is over time in a given account type. The taxability of a fund depends on the type of fund, how actively traded it is, and what it’s invested in. For instance, municipal bond funds are generally not taxable but equity dividends are. And a US broad market equity fund could really be held in any type of account with a little planning to make sure it fits with your strategy. There truly is a fund for every need, season, or personality so ignore the noise and choose funds that work for your particular situation.

The table below shows which accounts are generally more or less efficient for holding some typical asset classes. To be clear, I both love and hate graphics like this one because they can come across like advice and they don’t make room for the intricacies of an “it depends” way of thinking. There’s really no hard and fast rule when it comes to holding a particular asset in a particular account. Things can and will change over time and things also depend on whether you’re in the accumulation or deccumulation/longevity phase. That’s why we love the “it depends” answer to allocation questions. It will ALWAYS depend on your specific circumstances.

Picking Funds in Real Life

The truth is there are lots of ways to build a diverse portfolio, ranging from super simple to really complicated. We like to keep things simple these days and that includes our portfolio management strategy.

If you want to manage your own portfolio it’s especially important to choose assets that fit your comfort level as a manager. It’s useful to learn about more than one strategy and then decide what kind of portfolio you want, then you can lean in your own direction!

2 Fund Portfolio

You can be like JL Collins and only invest in one equities fund, VTSAX, which is Vanguard’s US Broad Market index fund. Collins argues that VTSAX holds enough large US corporations doing business in other countries that it’s like holding US and international funds (to which Ali argues that’s like saying if you eat a taco in Seattle you’re investing in Mexico). I see both of their points! If you dig a little deeper you’ll find that Collins has also held VBTLX bond funds and he has owned real estate in the past as well. Everything changes over time, and perhaps just one broad market mutual fund can get wide enough diversification to fit your strategy. And if you toss in a bond fund like VBTLX or a money market fund (Collins uses VMMXX) you might be good to go.

But what if you don’t have accounts at Vanguard? Not to worry, neither do we! Vanguard was the original trail blazer for low-fee investment products but there are other institutions like Fidelity and Schwab that are similarly awesome. All three brokerage firms offer comparable ETF, index, and mutual fund options and each also allows clients to trade without fees and commissions. Pick what works for you!

3 Fund Portfolio

The Bogleheads have widely suggested the idea of holding three basic asset classes that are each total market index funds — a US index fund, an international index fund, and a bond index fund. We love this idea because it offers equity to bond diversity as well as sector diversity. It’s simple as well as comprehensive. Holding multiple asset classes changes the tilt of a portfolio from leaning in one direction, however broad it might be, to being truly balanced.

4 Fund Portfolio

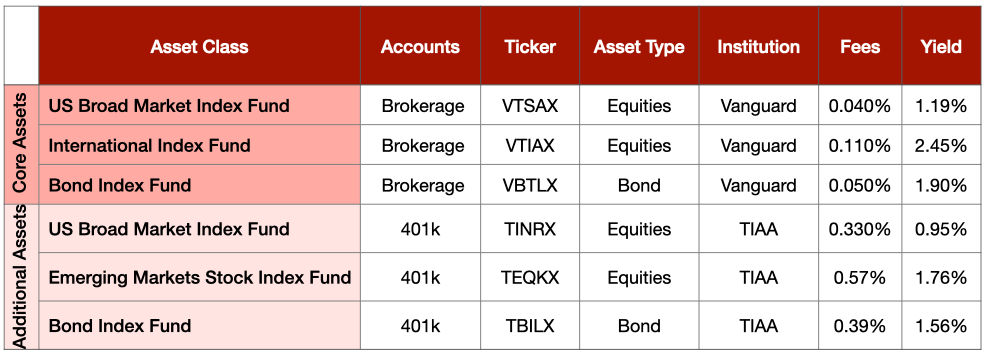

We loved the 3 fund strategy described above but we wanted to add a little more flexibility to that basic concept so we created a 4 fund strategy for ourselves to meet our needs during our early retirement years. Our brokerage account currently holds a US broad market ETF, an international equity ETF, a short term bond ETF, and a muni bond ETF. We also have a money market mutual fund to hold our annual living expenses after we’ve withdrawn our funds for the year.

We wanted to make sure we had more access to international markets as well as uncorrelated US investments. We also wanted to have bonds for SORR protection and for some longer term Money Jobs since we bought a house and have some remodeling projects to work on. Most of our diversity is held in our brokerage account right now since that’s the account funding our early retirement years. We can’t dip into our IRA’s or our Roth’s for a few more years yet so those accounts are still 100% growth oriented and only hold a US broad market ETF and international equity ETF.

6+ Fund Portfolio

Personally, I take my coffee black and hot so it makes sense that I like a simple 4 fund portfolio. But I know a lot of other people like to add sweetener or cream, or they like their coffee iced. Maybe the number of funds you want in your portfolio is kind of like the way you prefer your coffee?

A 6 or more fund portfolio typically has separate large cap, mid cap, and small cap US equities, along with an international fund and/or an emerging market fund. It might also have a REIT fund or other types of sector or region specific funds. It would likely also have one or two bond funds. Again, it all depends on what you’re interested in owning.

If managing 6 or more funds sounds complicated to you, you might wonder why a more complex strategy makes sense. People typically like to add additional funds beyond the basics when they want more control over the companies they’re invested in. Some want to have more exposure to mid and small cap companies, some want more dividend producing companies, some want REIT’s so they can hold real estate without having to deal with actual properties, some want to own companies that focus on sustainability or climate tech, and others just love individual stocks so much that they can’t imagine simplifying their holdings.

Is it possible that we’ll hold a 6 or more fun portfolio in the future? Yes! In fact Ali has been looking at a climate tech ETF and a gender diversity ETF which we’ll discuss when we do our end of year portfolio review. Again, it’s personal!

Picking the Best 401k or 403b Funds

It can be tricky to figure out your fund options through your employer’s system since they’re often quite limited and sometimes intentionally vague. In many cases you’ll find less optimal choices through employer programs particularly if they offer more proprietary funds through less transparent institutions. If that’s what you’re seeing you’re not alone. I had that issue through my employer provided 401k plan unfortunately. Hopefully you’re lucky like Ali was since her primary employer had Schwab 401k plans, which meant she had tons of excellent low fee options to choose from.

Employer provided retirement accounts might have lots of choices or a more restricted list of funds to invest in. If your employer’s retirement accounts are managed by one of the big three low fee brokerage institutions (Fidelity, Schwab, or Vanguard) you’ll probably have access to pretty much any fund you might want. But if your 401k is like mine was you might not have access to very many good options and you might not be able to choose the funds you’re most interested in. No matter what you have access to start with setting your investment goals and make sure your retirement accounts support your goals.

- What is your equity to bond goal for your current investing phase?

- How many funds do you want to own in your current investing phase?

- If you’re still in the accumulation phase, how many funds do you want to own in deccumulation?

- When do you need access to your funds?

- Can you identify the fees associated with your fund options?

- If you plan to roll any employer sponsored retirement accounts to a low fee institution, which brokerage firm (Fidelity, Schwab, or Vanguard) is best for you?

- Do you have access to low cost, passively managed index funds that meet your needs at your investing institution?

When reviewing your 401k’s list of funds, look for options that have “ETF” or “index” or “broad market” or include some other kind of index like S&P in the name. Basically, look for the best-worst fund among all your choices since employer sponsored fund options aren’t typically the best. More passively managed index style funds are a good option because they typically come with lower fees. If the fees are higher, the fund is mostly likely actively managed. If the fees are lower the fund is probably designed to follow an index and be passively managed.

Researching Funds

Assemble a holistic view of your portfolio to identify each of your accounts and the basic asset classes you might hold in each one. This process can help you identify the investment style that feels right for you as you evaluate which asset classes to hold in each kind of account.

Build your fund list by institution and asset class, and then fill in actual tickers so when it’s time to start applying your allocations across your accounts, you’ll know exactly which fund you’re going to use at any given time. Having this list can make setting up all of your accounts much faster and less stressful. No fuss no muss!

Start by making a list of each kind of fund you would consider owning at each institution where you have an account. And be sure to note the fees with each fund you invest in. And check to see if your employer provided retirement account is included in the lists already researched by the Bogleheads since they have compiled a really helpful list of funds at various institutions for you to consider. The goal is to pay the lowest possible fees in your traditional retirement accounts.

Now You’re Ready!

Now that you have your budget organized, you’ve picked your equity to bond ratio, you understand the importance of a bucket strategy, and you’ve outlined efficient fund placements, you’re ready to put all this information into practice. In the next post in this Allocation Strategies series you can practice setting up your accounts with the most efficient funds for your investing phase.

[…] Now check out Part 4 in this series! […]

LikeLike

[…] Part 4: Tax efficient fund placement […]

LikeLike

I like the primer!

One thing to note is that if your traditional IRA withdrawal (or RMD) plus, where applicable, Social Security payment, is less than the upper end of the 0% long term capital gains tax bracket, you have an opportunity for long term capital gains tax harvesting (or, if you have sufficient gains in your taxable account, you may not need to withdraw from the IRA…YMMV, check with your CFP, etc.).

Michael Kitces (whom my phone wants to autocorrect to Michael Kitteh) has an excellent primer on how ordinary income and long term capital gains stack: https://www.kitces.com/blog/understanding-the-mechanics-of-the-0-long-term-capital-gains-tax-rate-how-to-harvest-capital-gains-for-a-free-step-up-in-basis/

LikeLiked by 1 person

Thanks Jason. Yes, I agree regarding room for capital gains harvesting if your “stacked” income leaves room in that 0% range. And I love Michael Kitces. He has some of the best posts on many of the topics we write about. He is for sure one of my research go to sites. Cheers!

LikeLike

This is a great explanation of a complex topic. I also appreciated the baseball analogy!

LikeLiked by 1 person

Thanks Jess. This can be a complex topic but I think there are lots of ways to make it relatable to our daily lives. When we broke it down into manageable topics we felt a lot more in control.

LikeLike

I love the coffee analogy! I’m also a black coffee drinker and I’m in the JL Collins camp with 3 funds – stock funds, bond funds, and a money market; also cash, of course!

It’s funny, I have no problem with the concept of long-term savings, but it’s the much shorter-term that always trips me up. I’m saving up quite a chunk to be used in later 2022 and the vast majority of it is in VTSAX; the rest I’ve been putting into a savings account. Thanks to your talking about allocations, and a passing mention from Revanche, I did a little poking into I bonds and realized I could get 3%+ interest for 6 months, which isn’t a lot, but is a lot better than my 0% (but so convenient) savings account. So I’m off to do some allocating!

LikeLiked by 2 people

I’ve been hearing about those I-Bonds. Sounds like you have to buy them from a savings or bank account? Not a brokerage? And what is the investment limit? I say use what ever makes it easy to save for sure! Oh, and just wait for the cookie analogy.

LikeLike

[…] Allocation Strategies (Part 4: Tax Efficient Fund Placement) All Options […]

LikeLiked by 1 person

New but avid reader — really appreciate your posts! I’m wondering why you hold muni ETFs in your brokerage. Given your income, aren’t taxable bonds a better deal for you?

As for I-bonds, you buy them from https://www.treasurydirect.gov/indiv/research/indepth/ibonds/res_ibonds_ibuy.htm

LikeLiked by 1 person

Welcome Hope — We hold a muni ETF for its liquidity, reduced volatility and tax-free dividends. We’re also very interested in a simplified portfolio so holding multiple bonds with a range of maturity dates isn’t very appealing to us. I know there is a lot of interest in I-Bonds but we are not, partly because they are limited to $10K per person which isn’t very much. With interest rates so low these days it is hard to find anything that will pay enough to beat inflation, and that’s one reason to be in the stock market because it has over time more than beat inflation if you are willing to accept market risk. Cheers!

LikeLike

[…] by! It’s been a minute since I finished Part 4 in this allocation strategies series, focused on efficient fund placement. But I have a surprise for you! Since we’ve reached Part 5 of this series it’s time for […]

LikeLike