In Part 2 of our Allocation Strategies series we’re covering one of the most important topics relating to portfolio allocation, picking your equity to bond ratio.

What is portfolio allocation and why does it matter? Basically it’s about finding the right mix of investments, deciding which account buckets to put those investments in, and deciding when to tap into each of those buckets during your life. And like everything else in the world of investing, portfolio allocation is about balancing risk and growth.

Allocation strategies aren’t just for early retirees, or retirement in general. They’re useful concepts for anyone who invests. The goal is to make sure the success of your portfolio doesn’t depend on a single investment or even a single investing plan. Your portfolio allocation strategy should be designed to earn the total return you need over time for your entire life expectancy. And your strategy shouldn’t be a one-time decision either. You’ll want to revisit your allocation strategy annually as the market fluctuates and you make withdrawals or deposits so you can make sure it’s meeting your needs as well as your hopes and dreams.

We are not certified financial professionals. For more information please read our Disclaimer.

Everyone, Meet Jane Roe!

We need an example scenario for this post so in honor of the incredible importance of making abortion legal, safe, and accessible for every woman in the USA, we’ll call our example person Jane Roe. Because after all, having the right to choose for yourself is paramount to financial independence.

As we write this post Jane is in the process of figuring out her comfort level with risk so she can create her equity/bond allocation strategy. Of course Jane has already built her Money Job system to help her budget for annual expenses, but if you missed that first post in our Allocation Strategies series you can find that Money Job post here.

Here are a few more details about Jane…

- She is 45 years old, has no children, and single by choice

- She was a high income earner during her career

- She reached financial independence in 2020, and plans to start early retirement in 2022

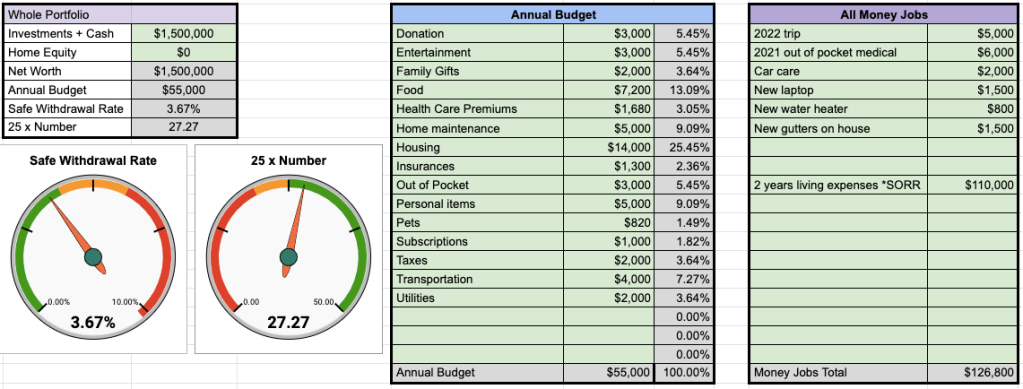

- Her post-retirement budget for annual living expenses (including taxes and health insurance) is $55,000

- She has $126,800 set aside in cash and cash equivalents to cover all of her Surprise and Experience Money Jobs for her first few retirement years

- Her total portfolio value is currently $1,500,000

- Her safe withdrawal rate (SWR) is 3.67%

- She saved 27.27 times her annual expenses before retiring

The following graphic gives us an overview of Jane’s portfolio and her SWR on the left, then a table for her budget in the middle, followed by a table for her additional Money Jobs on the right. The goal with this part of our spreadsheet is to keep an eye on the big picture of your finances.

What’s Your Risk Tolerance?

Anyone who invests in the market needs a baseline strategy that fits their age and risk tolerance. You need to know when you might start drawing down on your portfolio and you also need to know how freaked out you would be during normal (or unusual) market volatility. If you’re young and won’t need your money for decades, having all equities or a high percentage of equities in your portfolio will expose your money to the historical direction of the market… which is good because that historical direction is UP!! But if you’re retired and withdrawing from your portfolio now, or planning to retire very soon, it might make sense to reduce your equities somewhat for less exposure to near term unpredictability.

In other words, if you don’t need to withdraw from your portfolio anytime soon that volatility is probably a good thing since that upwards volatility helps create longterm compounding growth. But during retirement if you’re making regular withdrawals like we are, that volatility can create adverse sequence of returns risk and cause a portfolio to run out of money before you run out of time.

Do You Have (a) PMS?

We all have unique plans, goals, and dreams so we all need a financial plan that considers our goals and circumstances. And we all deserve better than the silly old rules of thumb that weren’t designed for us in the first place. From our perspective, every investor is a special unicorn.

If you’re thinking about what your allocation should be, pause to fill out a Personal Money Statement (PMS) or any other style of document that lets you outline your unique plans and put target dates on them. What are your hopes and dreams for your life now? And for your life after retirement? How would you feel during normal market fluctuations? How would you feel during a Black Swan event? What kinds of changes would you see as appropriate for you and your portfolio during normal market volatility, and during Black Swan events?

At the end of February in 2020 when the Coronavirus Crash first started we definitely had a moment of surprise and anxiety when we saw that crash keep crashing. I remember turning to Ali and asking, “What are we going to do?” In that moment we didn’t do anything other than refer back to our PMS document. Our PMS stated very clearly: “We will not panic as a result of the ups and downs of the market. And we will especially not panic if there is a major Black Swan event or a prolonged downturn. We will not sell securities due to market corrections. And we will not invest the cash set aside for our living expenses as a reaction to a downturn in the market.” Since we had our guidelines set before the crash we did not panic. We responded to the crash by doing nothing! Well nothing other than to go for a walk and focus on what we wanted to have for lunch.

What would you do if you experienced a market crash in retirement? Before that happens lay out your plan in a PMS!

What’s Your Equity to Bond Ratio?

When we filled out our PMS a year before we retired we talked a lot about what our equity to bond ratio should be as we approached early retirement, knowing our real goal was to make sure our portfolio could last for 60 years. We wanted enough bonds to give us some stability and we wanted enough equities to allow for growth. We talked about options like a more risk averse 60/40 ratio, as well as a more risk tolerant 80/20 ratio, and then we settled on an equity to bond ratio of 75/25. We can’t control much but we can control our equity to bond ratio and that means we have at least a little control over the long term reliability of our portfolio.

There are some generic retirement rules of thumb that traditional investment managers still recommend, such as the old idea that your percentage of stocks should equal 100 years less your age. According to that old rule of thumb Jane should hold only 55% equities and 45% bonds in her portfolio — we object to that! This is 2021 and people are living longer and retiring earlier than they were when that old rule of thumb was created. Today’s retirees need more growth oriented equity to bond ratios to make sure their portfolios last.

There actually is a new version of that old rule of thumb that says that your percentage of stocks should equal 120 years less your age. According to this new rule of thumb Jane should hold 75% equities and 25% bonds in her portfolio since she’s 45 years old. That sounds much better to us, but we still think it’s a bad idea to simply follow a standardized rule of thumb without taking everything unique about your situation into consideration.

Know Your Variables!

There are important variables to consider when trying to pick your portfolio’s equity to bond ratio. We each have circumstances, plans, and goals that compound to give us unique financial needs. We can control some variables to some degree, like how much we spend. But there are also some variables we can’t control at all, like inflation.

Variables you can hopefully control:

- How much you save

- How much you spend

- Your risk tolerance

- Your investment fees

Variables you can’t control:

- Inflation

- Market fluctuations

- Market return

- Your life expectancy

All of these variables are worth understanding and tracking, whether you can control them or not. For all of those things we can’t control we just do our best to make informed assumptions. We gather data, make plans, and stay open to making changes when we learn new things that give us a deeper understanding of our finances.

The chart below shows some of Jane’s basic portfolio data including her estimated real return and expenses. This gives her a baseline to start with when testing her portfolio.

Estimate Your Portfolio Longevity!

When estimating portfolio longevity we like to start very conservatively with a lower range of annual market growth and dividend yields. We also like to reduce nominal growth by estimated inflation and known fees to calculate a real return rate and finally target an allocated return rate.

Without a crystal ball it’s impossible to predict exactly how long a portfolio might last. But coming up with a baseline prediction is still an important part of the process. If you want to run your own estimate check out the spreadsheet we share, our Simpli-FI-ed Calculator.

75% Equities with a 3.67% SWR

Calculating real allocated return rates when estimating portfolio growth helps us clarify how our expenses (with annual inflation) impact our long term projections. It also helps us start to project how long our portfolio might last.

Based on the assumptions Jane started with such as 2% inflation and a 4.77% allocated real return, we can see in the example below that her portfolio is projected to run out of money in 47 years. And that initial example doesn’t even factor in things like major one time expenses or health care costs. That baseline starting point also excludes retirement income sources like pensions, Social Security, or rental property income. As shown in the graph below, Jane’s portfolio will continue to grow until her annually inflated expenses overtake her retained compounding growth.

The chart below shows how Jane’s growth and buying power with a nominal return of 7.8%, reduced by 2% inflation, leaves her with a real return of 5.77%. Jane’s 75% equity allocation further reduces her return rate down to an allocated return rate of 4.77%. When we subtracted Jane’s annual withdrawal rate we saw her 4.77% allocated return, less her 3.67% SWR, results in a 1.1% retained return. Having a retained return of only 1.1% may not seem like much but with the power of compounding growth it is still pretty magical.

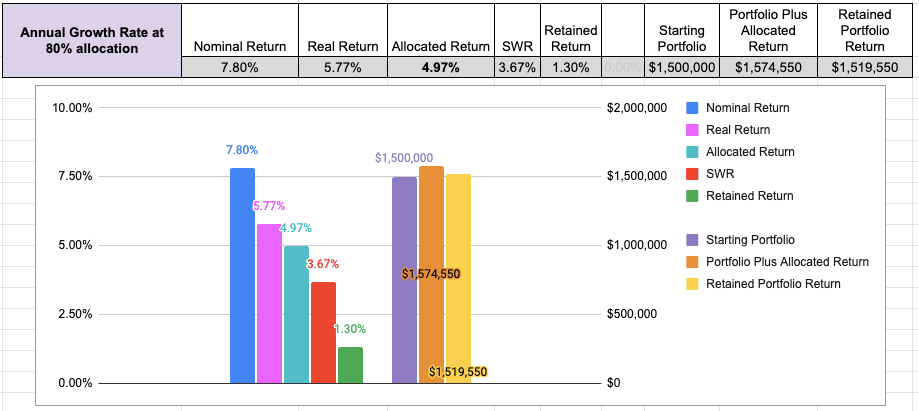

80% Equities with a 3.67% SWR

After running that initial baseline calculation above, Jane was a bit concerned that her portfolio would run out of money in only 47 years since she has projected her life expectancy at 95 years. And Jane knows those last years before her end of life could include costly medical expenses and health care needs so she’s definitely not comfortable with a 47 year portfolio. As a next step Jane wanted to move her equity allocation up to 80% to see how that would change things in the calculator.

You might not think a 5% change in equities would have that much of an impact, but incremental changes can have a big impact over the life of a portfolio. By increasing Jane’s equity allocation to 80% the calculator showed her portfolio would last an extra three years. That helps but it doesn’t get her to her full life expectancy. Jane might need to consider other variables that could extend the life of the portfolio even further like working for another one or two years to build a bigger portfolio and/or dropping her annual expenses by a few thousand dollars. All of the variables impacting your portfolio have either a negative or positive effect on growth so knowing what you can control is powerful.

Changing her equity allocation up to 80% extends the life of Jane’s portfolio to 50 years. The chart below shows how Jane’s growth and buying power with a nominal return of 7.8%, reduced by 2% inflation, leaves her with a real return of 5.77%. This time we see that Jane’s allocation of 80% equities further reduces her allocated return rate to 4.97%. Jane’s 4.97% allocated return, less her 3.67% SWR, results in a stronger 1.3% retained return.

Living with Volatility

One of the biggest factors for investors to consider is the higher your equity exposure the more your portfolio will be subject to the natural ups and downs of the market. Of course we don’t want volatility in our personal lives. But as longterm investors market volatility seems fairly normal in the same way that the overall longterm upward trend of the market seems normal. But even if you understand that reality, it can still be hard for lots of people to trust that what goes down must eventually come up again.

It’s also interesting to test your portfolio with real market activity. One example we’ve been using from our very recent history is the 2020 Coronavirus Crash, a Black Swan event that caused the Dow to lose 37% of its value and the S&P 500 to lose 34% of its value between February and March of last year. We decided to test Jane’s portfolio using a 75% equity allocation and a 30% market drop. Even though her portfolio showed a large drop along with the market she was relieved to see that her drop was less dramatic because her portfolio was only exposed to 75% of that total market crash. Jane’s portfolio only experienced a 22.5% drop in value compared to a 30% drop in the market. But that protection is a tradeoff against growth since Jane’s portfolio would have an allocated real growth rate of only 4.77%.

Conversely, if Jane’s portfolio was allocated to hold 80% equities her portfolio would be exposed to a larger drop as well as a potentially faster recovery. With 80% equities her portfolio would drop 24% in value during a 30% drop in the market, and then would hopefully recover faster with a larger allocated real growth rate of 4.97%. Allocation really is a balancing act between reducing risk and reaching for growth.

Growth is Key!

Picking an allocation rate that helps manage your reaction to volatility has value, but picking an allocation that keeps your portfolio growing for the amount of time you need is essential. Jane wants to do as much portfolio testing as possible now that she’s locked in a retirement SWR of 3.67%. Since we already tested Jane’s portfolio with 75% equities and then a more aggressive 80% equities rate, it’s time to see what a more conservative 60% equities rate looks like.

60% Equities with a 3.67% SWR

In this test Jane’s equity ratio has been reduced to 60%. The chart below shows the same nominal return of 7.8%, less 2% inflation, with her a real return of 5.77%, which gives her a 4.17% allocated return. Again we subtract Jane’s withdrawal rate to see how much growth she would retain. This time her 4.17% allocated return, less her 3.67% SWR, gives her only a 0.5% retained return.

Dropping the equities in Jane’s portfolio to only 60% doesn’t do her or her money any favors. The chart below shows that 60% equities with a 0.5% retained growth rate means her portfolio will only last 39 years. With these numbers rate Jane would run out of money by age 84, long before her projected life expectancy. The numbers in this test might keep her calm during a market drop but they won’t give Jane the annual growth rate she needs to make her portfolio last through a long retirement.

The only bright side to this test is shown below. Jane saw that 60% equities means her portfolio would only be exposed to an 18% drop during a 30% market drop, and of course she liked realizing her portfolio would take much less of a hit with this allocation if there was a market crash like the Coronavirus Crash today. That was a great reminder that having a lower exposure to risk can do a lot to protect your portfolio in a down market.

Fees Can Cause Problems!

One of the most overlooked variables in this complicated puzzle is investment fees. Some of us are DIY investors, but we’ve heard from plenty of people who don’t have the confidence to manage their own money and so prefer to work with CFA’s who actively manage their portfolios. We like to invest in more passively traded index funds that are designed to track a benchmark like the total US broad market. But others want to invest in funds that are more actively managed with the idea that they might bring in a home run hit that sets them apart from the pack. Regardless, we all pay some level of fees.

In the above examples Jane has been investing in passively managed index funds as much as possible with a net expense ratio of 0.03%. That’s a really, really low fee percentage and we’re using that number because it’s the same fee percentage we paid in 2020. In an effort to help Jane understand how her 0.03% fees are working in her favor, we’re going to test her portfolio with slightly higher fees. The example below shows what her portfolio would do over time if we increased her fee percentage to 0.5%. You might think those fees are still low, but that increase has a huge impact on Jane’s portfolio.

With this one seemingly small change in Jane’s variables her portfolio would only last 36 years compared to the 47 years we saw with 0.03% in fees. We’ve found that many people don’t realize paying 0.5% in fees (or even higher fee percentages) across their portfolio is extremely consequential. It’s really important to understand that fees can make a BIG difference, and not a good one, in the life of a portfolio.

Choose Your Equity to Bond Ratio Wisely!

Your final equity allocation ratio is very personal. Maybe yours is one part rule of thumb (120 – age = equities), plus one part emotional needs (check your PMS), and one part life expectancy (portfolio longevity). Some people might copy another person’s plan or follow standard advice, both of which are a bit like throwing a dart at a dart board to see what you randomly get. In the end you need to pick an equity to bond ratio that’s right for you, both emotionally and financially. Be mindful of your investment strategy and you will sleep better at night.

As an investor you can’t capitalize on long term compounding growth without exposing your portfolio to some risk. Your time horizon and temperament will help you find your equity to bond ratio, and you can document your strategy in your PMS with a description of WHY you picked your equity ratio. Then you can rebalance according to plan and on schedule, regardless of what the market is doing. There will be times when you need a reminder of what your goals are and why you picked your numbers, and there might also be reasons to adjust your equity ratio at some point. If you do make any changes, be sure to document your reasoning for those changes in your PMS. The goal is to make sure you don’t make adjustments on a whim or have knee jerk reactions based on fear or greed. And since I love sports analogies I’ll share my current favorite — Remember to go for base hits and don’t get caught up in the fervor of swinging to the fences.

The next post in this Portfolio Allocation series will focus on bucket strategies as a way to make sure we have money positioned in accounts that are accessible when we need them, as well as tucked away for long term growth.

[…] Part 2: Picking an Equity to Bond Ratio […]

LikeLike

While building up the emergency fund, my bond percentage was much higher. During the accumulation phase, my current plan is to keep buying equities to build up to 90-95% equities. Once that ratio is met, I’ll aim to achieve rebalancing by purchasing whichever is the lower percentage with new income.

As I get closer to FI, I’ll likely keep that ratio since I’m building in the ability to drastically reduce spending if necessary. The goal is for core expenses to be covered by 2% of the portfolio. Still figuring out what those core expenses will be, especially around healthcare and end of life care.

I ignore home equity since I’m not sure if I will sell it and what the market will value it at in the future.

LikeLiked by 1 person

Hey Chickadee! I do like “no selling” rebalancing if you are adding enough new money to move your allocation far enough. Just make sure you don’t set up a prolonged situation where you are always chasing your allocation. And 90-95% equities is aggressive. That being said, if you have enough actual dollars in your bond or cash portion of your investments to cover all your Money Jobs and you can handle the increased volatility of 95% equities then good on you. Have you modeled your portfolio in Portfolio Visualizer? It would be a great place to back test your plan to further verify your strategy. Have fun!!!! https://www.portfoliovisualizer.com/backtest-portfolio

LikeLike

Thanks for the link! Haven’t done a lot of modeling yet since I’m on auto pilot saving and investing. Looks like a toy for the weekend 🙂

The aggressive allocation is due to being single, having no dependents other than my cat, and being fairly confident in my career lasting as long as I want it to. My FI plans are likely to produce some income since I want to use FI to be able to pursue a PhD with my full attention and no financial worries. Next would be to join research teams in looking for solutions for how to save ourselves from the environmental hellscape we are getting deeper into. No point in being RE if it’ll be short lived due to ever increasing disaster frequency and intensity.

Being FI will provide a sense of safety and reasonable work life balance while contributing in the best way I am able to. Having the savings to insist on a reasonable work schedule would allow time with friends and family, traveling, and enjoying hobbies like kayaking and haphazard attempts at art. I want to participate in making helpful discoveries, but don’t think it’s necessary or healthy to sacrifice all of the rest that life has to offer.

LikeLiked by 1 person

I also thank you for the link to backtest portfolios!

After reading this article I got out my spreadsheets and looked more closely at how we are invested. There is a bit of an age gap between my spouse and I so I’m trying to find a comfortable spot to keep things stable enough for his lifetime and get enough growth to cover myself. We have some additional variables that could make this challenging. However, we were only 49% equities as a total portfolio and I have started making some changes to increase that. Your posts are always a nice reminder to get on top of this and not let it slide

LikeLiked by 1 person

Thanks Jess. Its really important to get things set for your current circumstance then make sure you follow up at least once a year. In our PMS we have 4 times a year that we check in on our allocation. 1) May for general rebalancing 2) Any new money coming in to invest 3) Annual funding of our yearly expenses 4) Large market drops of 5% or more. This really helps remind us how important allocation and rebalancing are to the success of our overall portfolio. Good luck!

LikeLike

How funny, I rebalanced a day before you published this!

I just turned 50 so I decided to pick an allocation that would be good for my last 5 years of work before retiring (knock on wood).

My previous plan had been to have 15% of my portfolio in bonds, and another 4% was in cash/money market. That left 81% of my whole portfolio/85% of my retirement funds in stocks. Since I hope to be on a short runway to retirement, I don’t want to be so aggressive anymore, so now I have 35% of my whole portfolio in stable investments and 65% in stocks. (Looking at only my retirement accounts, the split is 30/70.)

It’s clearly more conservative than I’ve been in the past, but thanks to the truly epic market growth in the last year, the actual dollar amount I have in stocks is equal to my entire portfolio at the start of 2020. That makes me feel like I’m still in good shape to benefit quite a lot from the robust market, while better shielding my entire account from really adverse returns.

It’s hard to make these decisions since we don’t know what the future holds! But I’d rather decide and act than waffle about it forever.

LikeLiked by 1 person

There’s a ton of info out there that suggests shifting slightly more conservative a few years out from retirement. Then slowly increasing your equities back up to a level that will ensure a bit more growth to make sure your portfolio outlasts you. Bottom line, make sure you put all your money to work. Don’t leave any cash without a job. Invest it or keep it cash, but know why you are doing that and what you want to do as you move through your process. It helps so much to have your money organized and working so you can focus on getting ready to retire and then find your new personal, financial, and emotional baseline once you have made the leap into retirement. Have a plan and follow through. Keep up the good work!!!

LikeLike

Hi Alison,

I’m pretty new to your blog, could you tell me if you’ve written a post of nitty-gritty detail/plan of withdrawing money from your accounts in the FIRE’d life and before Medicare?

I don’t know if you live of your blog revenue or other side-hustle/gig income or if you and Ali are drawing from your taxable or IRA’s.

The reason I’m asking is that I received an invite to register for a Retirement planning seminar at a local community college at a cost of $50 for 2 days of 3 hours each. It will be taught by some kind of CFA but supposedly will not be pushing/selling his services to the attendees. I wonder if it’s worth going there or if it could be too basic and waste of my time on Saturdays or who knows I might also hear a sales pitch too. $50 is a small fare if I heard a valuable training.

LikeLiked by 1 person

Hey Smiley, we have not written a step by step post for withdrawing from our accounts in retirement. Yet. But now that we are finishing our 3rd full retirement year we are feeling ready to write that post.

Our current plan is to live off our brokerage account until I turn 59.5, which is in about 2 years. Then we will tap my IRA for our living expenses and focus on Roth conversions in Ali’s IRA since she’s 10 years younger. We had intended on doing BIG Roth conversions while traveling internationally and using international health care. But now that we are on the ACA we have to watch our income limits so we can qualify for the ACA subsidies so that changed our Roth conversion plans.

We do not make any money off our blog or from coaching. Our blog has been online since Feb. 2019 and in that time we have earned $15.38 from Amazon, plus a few free months for our Trusted Housesitters account and our Traveling Mailbox account. But that’s it! We do not run adds or accept any partnerships, and we get a kick out of declining offers (the last one was from Personal Capital just this month when we said “No thank you!” Our blog is a hobby and a giving tool, but it’s not a business and it’s not an income earner. And it never will be.

We saved and planned for retirement as best we could over time, and we made a lot of mistakes, but we kept learning. We really got focused when we found the FIRE movement in 2014 and finally made some connections and people to share ideas with. The FIRE movement has grown so much and become a diverse community since then!

Regarding the retirement seminar, if you are interested, go. But watch out as most CFA’s will have a bias in one way or another. As long as you know that’s going on and don’t feel obligated to buy anything they’re selling, you might find things to learn and benefit from. Have you ever worked with a fee-only CFP? We do recommend to pretty much everyone we talk to that you might consider working with a CFP who can look at your specific situation and help you build a plan that will work for you, without any sales messages interfering in your best interests. Cheers!

LikeLike

Thanks for your response, Alison.

I took a look at the brochure about the seminar. Actually, this guy seems to be CFP/CRPS/financial advisor. No clue what CRPS stands for. Since I trust none of them, I called him a CFA. I think I’ll register and go. I just have this curiosity suddenly and the gut feeling says to go and satisfy it, LOL.

I’ve been reading forums and FIRE blogs for years, but it has dawned on me recently that I haven’t seen any articles or blogs explaining some real-life examples of withdrawing money including the Roth IRA conversions if it’s part of their plan. Would you know by any chance of any person who might have presented such examples along with the math walk-through? PF blogging is as wide as looking for recipes online, so I don’t google them unless somebody recommends that specific blog.

I’m considering a fee-only CFP in the future. Since my spouse wants to continue working for a few years, but I’m itching to quit much sooner, I am in no hurry to pursue this now. However, I love reading about real life experiences of FIRE’d people and how they handle their finances. It’s been a pleasure reading your blog so far because indeed it’s not trashed with ads popping on the right and on the left and after each paragraph. Very few such blogs like yours out there. OTOH, I read a couple of blogs even with heavy advertising because they present useful material.

I’ll be back to read some more ;-). Hope you both are doing well health-wise and in your new compound.

LikeLiked by 1 person

We went to tons of seminars and read every blog and book we could get our hands on. But none of them went through the math to explain how it all worked. That’s why we started building our own spreadsheet which we use and keep improving for coaching others, though it’s not perfect and it’s not a crystal ball. We know we can’t accurately predict the market, tax rates, or our future needs. But we can guesstimate and do our best to make flexible plans since we can see how things “might” work, and that has to be good enough until we get more data in the future.

With some planning you will get much closer to your goals. Making incremental small changes as you go along is what works best because tomorrow something might be different. Stay open and flexible and know the information and tools you need are out there. There is so much power in taking the position that you are in charge of your money, because no one is going to care about your money as much as you do. Pay for help when appropriate, but you should be in charge. And don’t let anyone suggest that you can’t do this. You can. You will find a process and a system that works for you.

LikeLike

[…] and brokerage accounts to match our schedule for drawing those funds down. Make sure you figure out your ideal equity to bond ratio and stick with your unique […]

LikeLike

[…] to introduce some bonds as well to those accounts based on your predetermined asset allocation and equity to bond ratio. The idea is to always have access to some kind of stable bond fund in the account you are drawing […]

LikeLike

[…] Step 2: Picking your Equity to Bond Ratio […]

LikeLike