Wow, time really does fly by! It’s been a minute since I finished Part 4 in this allocation strategies series, focused on efficient fund placement. But I have a surprise for you! Since we’ve reached Part 5 of this series it’s time for me to give you all a new tool to use on your own. We’ve built some allocation and rebalancing tools within our bigger spreadsheet that we use to manage our own portfolio and for financial coaching, and now we’re releasing our new Allocation and Rebalancing Worksheet with this post!

2022 is year 4 of our early retirement which means we’ve gotten into a great routine that starts with replenishing our bucket of cash to cover our annual living expenses at the start of each year. We use our allocation and rebalancing tools to plan our withdrawals and make the process easier. When we withdrew our cash for this year a few months ago in early January that was right before the market started dropping off its little ski jump into a correction, which it still hasn’t completely recovered from. Market fluctuations like this are a great reminder of the importance of having a strategy for allocation and rebalancing, and that was a great reminder for me to wrap this series up!

We are not certified financial professionals. For more information please read our Disclaimer.

What’ve we been up to?

In February we got busy collecting our tax related info to send to our new CPA. Simultaneously, we started the process of updating our wills since we moved our residency from Washington State to Arizona last year. And we also created a new trust to hold our real estate and brokerage account since we now own a compound and our housemate and his puppy live here with us. Our housemate is 15 years older than I am and Ali is 11 years younger than me, so I assume we’ll outlive our housemate. But we take this responsibility seriously and we wanted to make sure our plans won’t be foiled if we both die before our housemate.

We last updated our wills in 2018 when we retired and planned to live as full time travelers all over the world, and a lot has changed since then. Outlining plans and wishes to follow in case we die unexpectedly isn’t the most fun task to work on, but it’s important and it feels even more important because of the compound. We got a recommendation for a lawyer in our area from some FI community friends but after two meetings we decided to fire her as it became clear she wasn’t a good fit for us. That particular lawyer approached estate planning from a place of fear and distrust, and wasn’t honoring the fact that we come from a place of love for our chosen family. Luckily the second lawyer on our list was a perfect fit for us so building our new wills and trust went smoothly once we made that change.

That experience was another good reminder for us, that we will continue to be true to our personal stance to lead with optimistic generosity, not fear. So here’s a nudge for you all before I dive into the topics of allocation and rebalancing — Make sure you have a will or estate plan that makes your wishes clear and easy to follow. (And in case our nieces and nephews are reading this, Ali and I want to be cremated and have our ashes spread somewhere FUN! We don’t care where (our nieces and nephews can decide that), just as long as our ashes are scattered and not kept on a shelf!)

Our other big distraction in Q1 of this year will come as a surprise to most folks who actually know us… we bought a 16 foot travel trailer! That was a cool way to fulfill a dream that started before we retired. We’ve always wanted to take more road trips around the US but never felt ready or equipped before now. We’re thankful to the friends who inspired us to take the RV plunge, like the Geekstreamers who used to have a bigger Airstream of their own. In fact, I started writing this post while we were camping in our little trailer at the Grand Canyon. We got a few inches of snow one day so we stayed inside our trailer, drank hot chocolate, watched the clouds move through, and relished the time for writing!

Our simplicity strategy

In 2018 when we retired and set up our portfolio we decided to consolidate all of our accounts into one banking institution for ease of accessibility, transfers, and conversions between accounts. Consolidating our accounts at Schwab came with one additional benefit that we value — simplicity! The easier it is for us to manage our portfolio, the more we’ll enjoy sticking with our plan, and the less we have to worry about getting overwhelmed by the process. Thus far it’s working great!

Why Schwab? We do think Vanguard, Schwab, and Fidelity are all great options. We both had a strong preference for Schwab since we each had individual experiences with Schwab before we met, and over time we pushed more and more of our money to Schwab. My early investing experience was with Schwab since I opened my first brokerage account there a million years ago when I needed a place to hold some individual stock shares my grandparents gave me back when I was in my 20’s. I didn’t know much about investing back then but it was clear at the time that Schwab was a well known, low cost institution that made it easy for me to open an account and transfer over those shares.

Ali’s first 401k was started by her favorite employer two years after she graduated college and that company held all of their employee 401k plans at Schwab, which means Ali started investing for retirement at Schwab from the beginning. When Ali left that firm she rolled her 401k funds into the IRA she had already opened at Schwab, and when she quit her last job before retirement she rolled that high fee, under-performing 401k into the same IRA at Schwab as well so those funds could finally thrive. It’s fair to say that we chose Schwab not because we think they’re better than Fidelity or Vanguard, but because that was always the most convenient option for us.

And yes others have tried to advise us to move to Vanguard because that’s where the cool kids are. But Vanguard’s online platform is too basic for us, we love Schwab’s dashboard full of data and cool research tools to play with. Everyone should choose for themselves!

Our allocation learning curve

When we first laid out a roadmap for our retirement portfolio in 2018 we were using version 1 of our fancy spreadsheet to help us decide which asset classes we would hold in our portfolio. And of course we had read every blog post we could find on the subject. Somehow we had gotten it in our heads that we were “supposed to” set up our portfolio to hold the exact same 75/25 equity to bond ratio in each account.

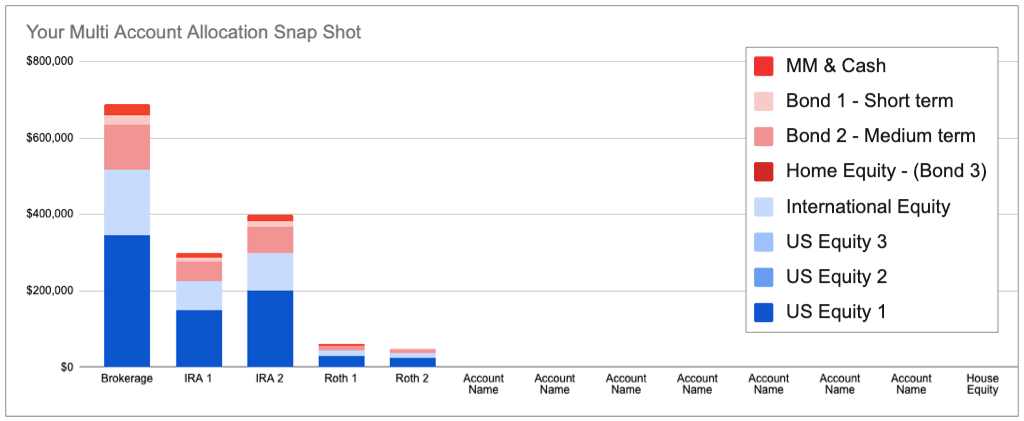

If we had stuck to that copycat allocation plan our portfolio would have looked a lot like the screenshot below. Don’t get too excited, this example shows our 5 accounts but with our fictitious case study volunteer Jane’s portfolio numbers (there’s more info on Jane below). Our numbers are private! And if you’re wondering why there are so many blank accounts in the screenshot below that’s because our new Allocation and Rebalancing Worksheet wasn’t designed just for us, we’ve learned through coaching that some people have lots of accounts in their portfolios.

The screenshot above shows the same 75/25 allocation in five accounts. We only had to model that strategy once to learn why that wouldn’t work for us. Having to check account balances in 5 different accounts and rebalance all 5 accounts back to 75/25 would have been too overwhelming and time consuming for us.

Eventually we found the concept of asset allocation in multiple accounts on the Boglehead Wiki. We like to think of that concept as holistic asset allocation across all of our accounts. That works great for us since we don’t spend a lot of time looking at our accounts individually. Each of our accounts really has its own Money Job strategy but that doesn’t change the fact that our personal finance strategy is all about designing and managing our portfolio as a whole.

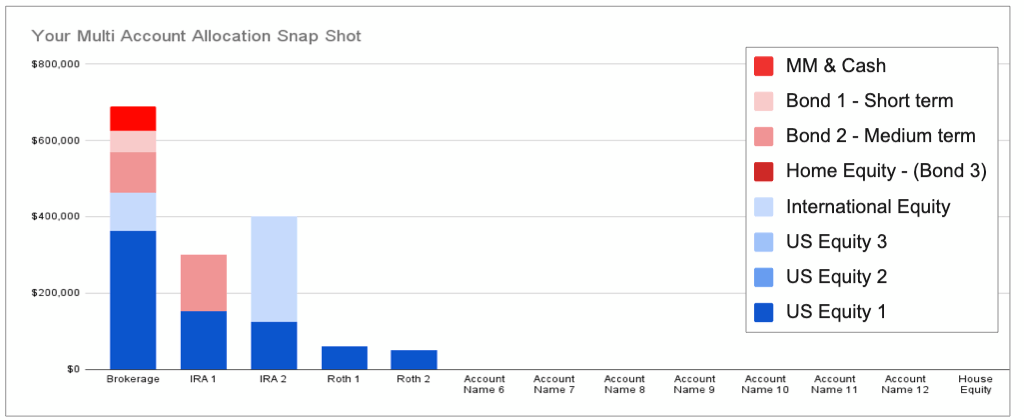

This screenshot above shows our 5 account portfolio (still Jane’s numbers and not ours!) with the relative size of each account and breakdown of asset classes held in each account. Our two Roth’s only hold one asset class, equities. Starting this year our two IRA’s are no longer allocated the same way because of our age difference, so now my IRA holds a mix of bonds and equities while Ali’s IRA still holds all equities and no bonds. Our brokerage account is the pièce de résistance since it holds equities and bonds, and it holds all of the funds we’re invested in. When we add up the equity to bond ratios across all 5 accounts in this exercise we hit the target allocation of 75/25, which is Jane’s target allocation and it was ours too up until this year. We’ve shifted to 80/20 this year from our original 75/25 ratio since we now own real estate and real estate feels more like a bond to us.

This strategy keeps things as simple as possible since we really only have to deal with rebalancing our brokerage account for now, and we are mindful about avoiding an unwanted taxable event when rebalancing. If we need to make bigger shifts in the future we would rebalance my IRA as well to keep any large capital gains and/or losses in the brokerage account in check. This approach makes our strategy a thousand times simpler and the need for rebalancing seems much less intimidating.

About that new toy!! Our Allocation and Rebalancing Worksheet

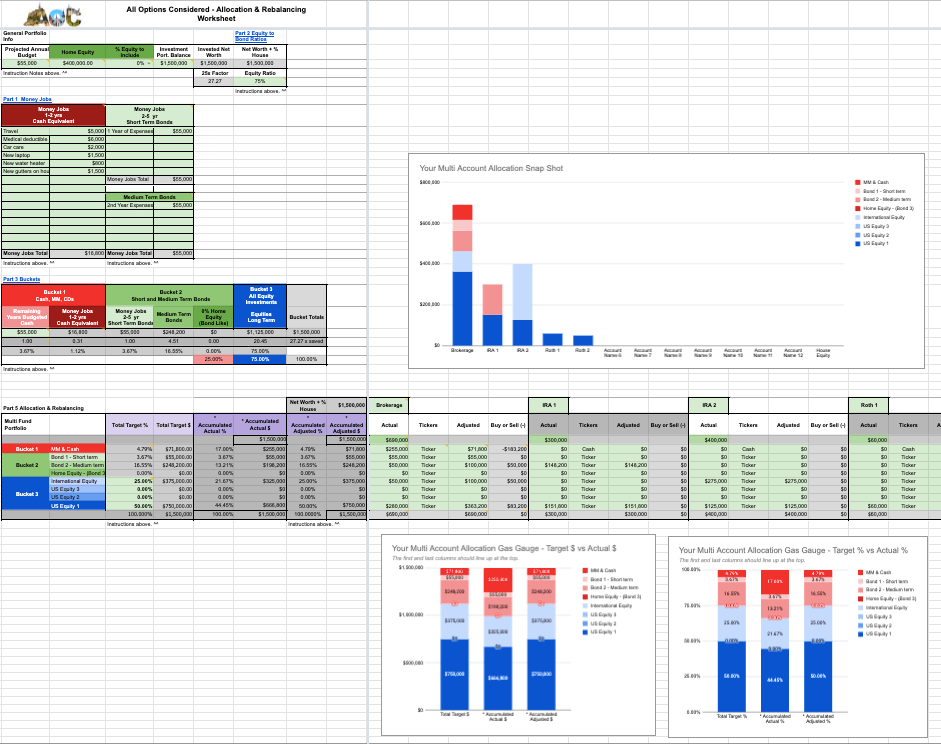

We still get people asking for our big fancy spreadsheet that we use for coaching regularly but we don’t share that publicly, at least not in its entirety. Instead we are including a few tabs from that spreadsheet in our new Allocation and Rebalancing Worksheet to help folks figure out how to set up the allocation in your own portfolio.

Honestly, the most fun part about writing this series for me was setting up this new worksheet so people can copy it to their own Google Drives and play with it. It was fun to cut some tools out of our personal spreadsheet so we can share a few bits and pieces with you all! Our new Allocation and Rebalancing Worksheet starts with a Money Job widget and works through each of the steps in this series ending with an allocation widget. If you follow the steps in this series you’ll be well on your way to allocating your own portfolio with one relatively simple tool.

A reminder about our case study, Jane!

Jane is the namesake of our example scenario for this series, in honor of the incredible importance of making abortion legal, safe, and accessible for every woman in the USA. Having the right to choose for yourself is essential to financial independence, just like the right to choose is essential to sexual and reproductive health.

So far this series has focused on understanding your budget, equity to bond ratio, withdrawal strategies, cash accessibility, and tax efficient fund placement before you start slicing and dicing your portfolio. Allocation strategies should not be set willy nilly, but that doesn’t mean you have to obsess over fractions of a percent before you can take action. With any recipe you’ll want all of your ingredients ready before you start mixing things together, and when it comes to managing your own portfolio you’ll want your budget and fund choices set before deciding how to allocate your portfolio.

Jane has been in the process of figuring out her comfort level with risk so she can set her own equity/bond allocation. We wanted Jane to think about how she would feel if the market experienced a planned or unplanned correction, and Russia’s invasion of Ukraine gave Jane a perfect example of what we’re talking about since this latest Black Swan event definitely gave the markets a pounding.

Here are a few more details about Jane…

- She’s 45 years old, has no children, and is single by choice

- She was a high income earner during her career

- She reached financial independence in 2020 and started early retirement in 2022

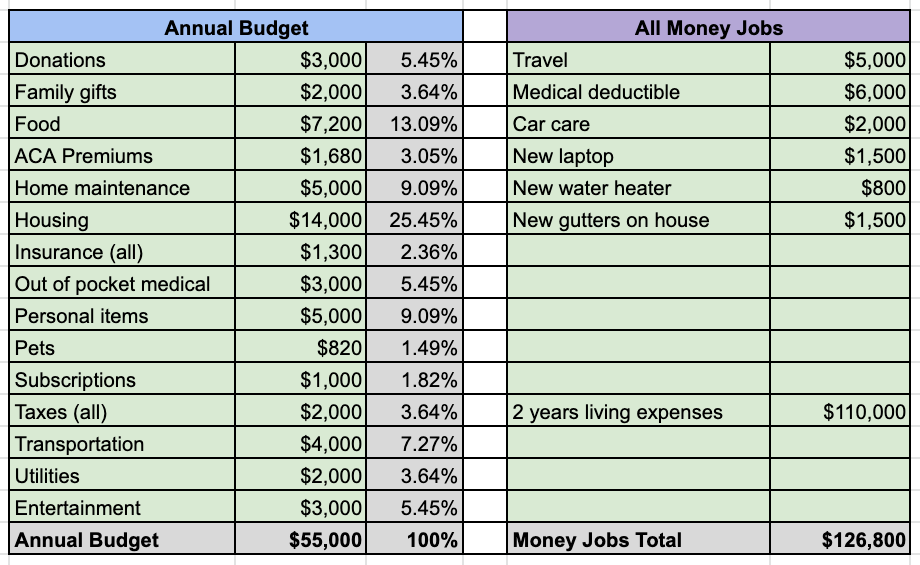

- Her post-retirement budget for annual living expenses (including taxes and health insurance) is $55,000

- She has $126,800 set aside in cash and cash equivalents to cover all of her Surprise and Experience Money Jobs for her first few retirement years

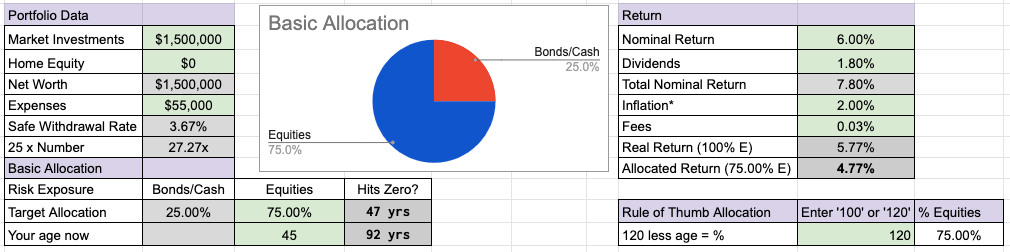

- Her total portfolio value is currently $1,500,000

- Her safe withdrawal rate (SWR) is 3.67%

- She saved 27.27 times her annual expenses before retiring

Now lets review what Jane has already set up in this process…

Step 1: Money Jobs and Budgeting

As a first step in our new Allocation and Rebalancing Worksheet, Jane built her Money Job system to help her budget for annual expenses.

Jane mapped out all of her short term and longer term money needs and gave them Money Jobs. She listed her annual living budget with all of her planned expenses, plus funds for some larger expected and unexpected Money Jobs. Jane made sure to set money aside for any out of pocket medical expenses she could imagine needing to cover this year, and then she made sure to set money aside for travel as well. And once Jane had compiled and updated this list of near term money needs she knew how much cash she would need in her total annual budget, which would help her decide which account to pull it from.

Step 2: Picking your Equity to Bond Ratio

Jane’s next step in the Allocation and Rebalancing Worksheet was to choose an equity to bond ratio for early retirement. Jane set a 75/25 ratio because she needs access to some funds now and she’ll also need her portfolio to be exposed to the upward trend of the long term market for growth to support her long retirement. She also likes having a healthy exposure to market growth as a hedge against inflation. Jane is prepared to stick to the goals and strategies she set in her Personal Money Statement (PMS) when the next Black Swan event hits.

Since we’re currently living in a world with high inflation we’ve been experimenting with increased inflation numbers in our own spreadsheet so we can model portfolio activity with a range of inflation numbers. We’ve experimented with our own portfolio and long term inflation up to 3%. That’s quite a cold shower but it’s important for us to understand how that would look. As shown in the screenshot below we modeled Jane’s portfolio with a more average inflation rate of 2% with only a 6% nominal return as the baseline.

Step 3: Buckets for Withdrawals

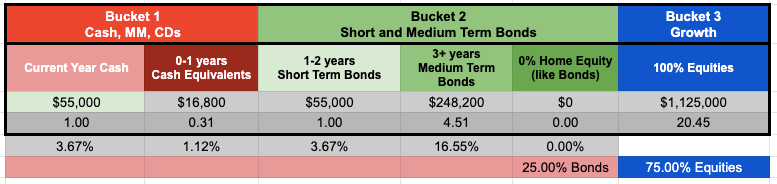

The idea of planning withdrawal strategies was intimidating for Jane initially, but the more she worked on our strategy the more her confidence grew! Jane used a basic bucket strategy in the worksheet with buckets for 3 different spending and saving scenarios in order to position her money for accessibility to cover near term needs, long term growth, and a bit of down market protection just in case.

Jane planned to start her first year of early retirement with $55,000 in cash in a fully accessible savings account to cover her entire budget. She linked that savings account to a checking account with automatic transfers of $4,500 each month replacing her previous W2 paychecks. She also keeps a minimum balance of $1,000 in that checking account at all times so there’s still a cushion after she pays her bills for the month, just in case of small surprises.

Next Jane decided to keep one year of living expenses in a short term bond fund as a backup for accessibility, though she might hold that kind of money in CD’s in the future when interest rates are higher again. For now her bond fund will help protect her portfolio from the natural ups and downs of the market so she can avoid selling equities during a big correction. Her plan means she’ll have access to the funds she needs for one year if the market happens to be down in early January when she collects cash for the next year’s living expenses. Jane also decided to keep an extra year of living expenses in a medium term bond fund for the same reasons described above.

Step 4: Efficient Fund Placement

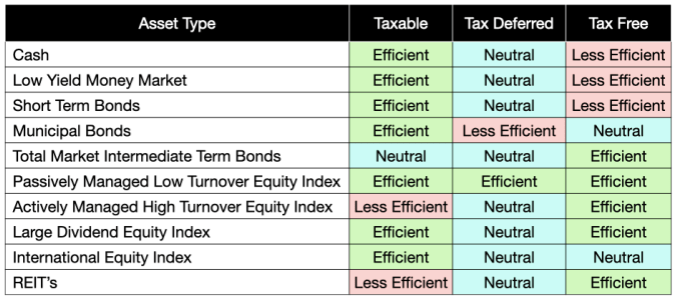

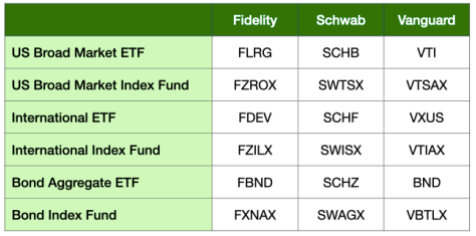

Jane has several different kinds of tax advantaged and taxable accounts in her portfolio, and she’s using the following table as a suggestion for tax efficient placement of funds in each account type. These kinds of fund guides don’t provide black and white answers or advice, and that’s a good thing since efficiency depends on a lot of different factors and personal preference is one of the more heavily weighted factors to consider. What matters most is understanding why the funds you’re interested in might be more or less tax efficient for you specifically so you can make choices that are best for your particular portfolio.

The next thing Jane did was spend time researching the types of funds she wants to hold at each institution where she has an account. Jane is a big fan of index funds just like we are, and she holds only ETF’s (no mutual funds) including some of the funds shown below.

Step 5: Allocating Your Portfolio

When Jane was ready to focus on asset allocation she wanted a simplified approach. She started by filling her smaller tax deferred and tax free accounts with the asset class she wants to hold the most of which is equities. Jane filled her smallest account, a Roth, with 100% equities. Her next smallest account is an IRA so she allocated that one next, also with 100% equities. With this approach Jane set up a good chunk of her portfolio to ride the equity train long term since she’s only 45 years old and won’t tap into her tax deferred or tax free accounts until after she turns 60. Then when she’s around 55 years old with less than 5 years left before she’ll have access to all of her age restricted accounts she’ll make some strategic moves to prepare those accounts for withdrawals, which could mean new allocations for her accounts.

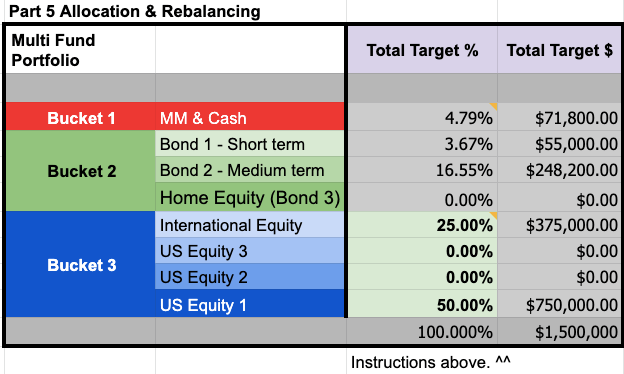

Back in Step 1 we made sure Jane’s values and goals matched her Money Jobs which helped her pick her equity to bond ratio. Then Jane picked the asset classes she wants to hold and divided them into the three buckets shown in the screenshot below so she can drill down to the percentages of each class she’s going to hold in each account. After a little more research Jane decided she wants to hold 25% international equities in addition to US equities because she doesn’t want her portfolio to be too US-centric. The worksheet that accompanies this series calculates percentages of cash, short term and long term bonds for each bucket based on when Jane wants access to funds and dollar amounts she assigned to her Money Jobs.

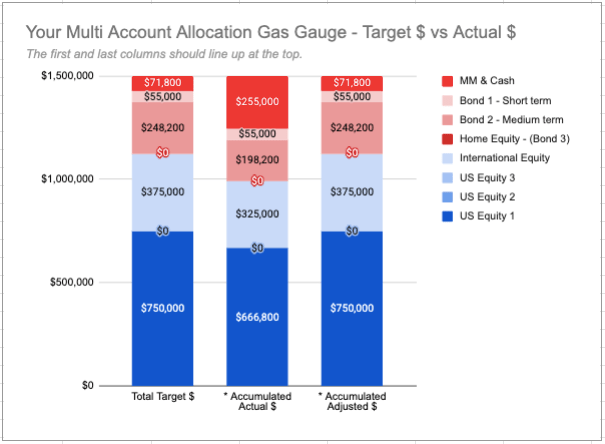

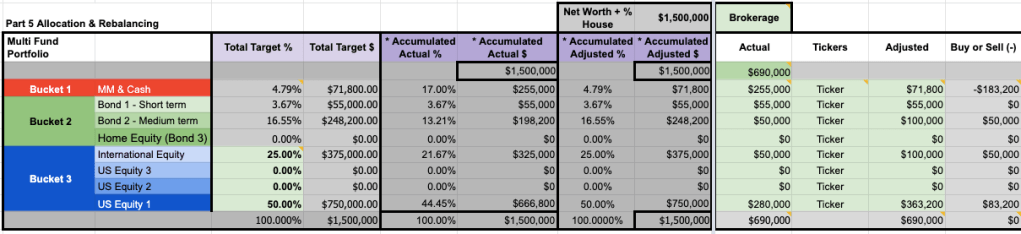

Now that Jane knows her asset class percentages she can assign them to the dollar amounts in each account based on tax efficient placement and the timing for accessing each account. The screenshot below shows a widget from the worksheet that calculates the total balances of each account and which asset class will be assigned to each account.

In the last step of the allocation process, it can be very straight forward to assign dollar amounts to asset classes in each account while accumulating percentages across your total portfolio.

And just like that, Jane has set the allocation for her whole portfolio. By entering all her values in the worksheet she had all the information she needed to make adjustments in her accounts.

This process can take a day to accomplish, or several months, or longer, depending on where your accounts are held and which phase you’re in on the road to managing your own money. And most importantly, this process can be tackled one step at a time in easy to manage smaller bites so you don’t get overwhelmed. Jane started this process last year and just finished it now, and that’s just fine! Once you get your worksheet set up correctly you can update the values, run the percentages, and make adjustments each time you rebalance. Simple. Well, relatively simple anyway!

No two people will have the same asset allocation, asset classes, and accounts. Just like my chocolate chip cookies don’t taste the same as my mom’s, because I like a higher ratio of brown sugar in mine. But both cookies taste great and make us smile!

How to rebalance

The fun thing about annual rebalancing is that if your Money Jobs and equity to bond target haven’t changed, your worksheet doesn’t need to change either. You simply start by checking the current balances in your portfolio and pick the accounts you need to adjust to bring your holdings back in line with your targets. That process took us 15 minutes last May when we did annual rebalancing, and 30 minutes in January since it was time to start holding bonds in my IRA. When we made that bigger strategy change this year I just entered new values in the worksheet, identified the funds to trade and the accounts to trade in, determined the amounts to adjust, and took action.

If your Money Jobs and equity to bond ratio targets change, don’t be intimidated. Things can and should change over time, so after you update and change your strategy just start with your new target numbers and pick the accounts you need to adjust to hit the new targets. Then reenter your account balances and holdings following the gas gauge and sheet to see where you need to make adjustments.

When to rebalance

By this point in the process you should have already picked the circumstances that would cause you to rebalance. In our case we chose 5 different instances when rebalancing would make sense to us, and outlined those in our PMS document…

- January: We withdraw a full year of cash to cover our living expenses, which makes it a great time to rebalance and perform two functions at once. We withdraw funds in January in such a way that it brings us back to our target allocation. We also do an initial Roth conversion in January since we expect the market to be up from there by end of year. Rebalancing doesn’t have to be exact, so if our withdrawal gets us to 79% instead of 80% equities that might be close enough, depending on how exact we want to be and whether it would be easy or complicated to sell one more fund to try to get closer to the exact target.

- May: No matter what’s going on in the world we have a date for rebalancing on Ali’s birthday in May. We’ve found that so far in our early retirement our allocation has drifted off target by end of May each year and our portfolio is in need of a little rebalancing.

- December: We do the second half of our annual Roth conversions in December, which means we’re shifting money from Ali’s IRA to her Roth (not taking early withdrawals just making conversions). The conversions are taxable events but since we’re moving equities from her tax deferred IRA to her tax free Roth we can make other moves in our portfolio at the same time to adjust our allocation as well if something is really out of whack.

- Opportunistic: Large market events, up or down, can make for great rebalancing opportunities. Some folks even set targets that would trigger rebalancing during more dramatic market fluctuations. For instance, if the market drops 15% you might check your overall allocation and if you were more than 5% off your target that would be a good time to rebalance. We are not interested in trying to time the market in general, but a major market drop is a valid reason to buy low and also do some rebalancing.

- Windfalls: When we were still working we got a few small bonuses once in a while, and those fell into the windfall category we track in our spreadsheet. For anyone who gets bonuses at work or gifts of money from family, those one time windfalls are a perfect “no sell” opportunity to rebalance your portfolio since you’re adding new funds anyway. No matter what, make sure you have a plan in your PMS to handle windfall funds so you can opportunistically fill up depleted buckets and put that money to work.

Rebalance guide rails

Our rebalancing strategy also includes a guide rail rule which we stick to very religiously. In order for us to rebalance our portfolio during any of the times listed above, our allocation has to be at least 5% off of our target. If our portfolio is truly out of balance that means our equity ratio has to be at least 5% higher or lower than our 80% equity target. And if that is the case during any of the time frames listed above we will then rebalance back to our target allocation. Why do we stick to this rule? We stick to it because we don’t want to mess with our holdings if we don’t have to. This way we don’t force ourselves to rebalance if we are +/- 1% or even 2%. And it means we don’t have to look at our portfolio all the time. We really don’t want to micro manage it in that way.

Dealing with limited asset class options

Before we retired we had 401k accounts sponsored by our employers where most of the funds had high fees and underwhelming growth even in a strong market. I had that type of 401k limitation for more than 15 years, but luckily Ali only had that type of 401k for two years at the end of her career.

So how do you fold those kinds of accounts into a portfolio when building your allocation plan? If you’re still working it’s simple, just find the “least worst fund” in the asset class you want to hold and start with that. If you can find one little S&P 500 index fund with a 0.4% fee and that’s the best you can do in your 401k, then that’s the first one you pick to fill up your equity target. After that you can add the equity funds you really want to hold in other accounts. It’s all about doing the best with what you have and not dwelling or getting stuck on your choices.

If you’re ready to retire it’s even more simple. Once you retire or quit your job you can roll your employer sponsored account over to an institution that offers better investment choices (like at Vanguard, Fidelity, or Schwab). The ability to manage your own investments independently with control over your fund choices and no high management fees can make an enormous difference in your long term growth potential.

Thats it!

There are lots of different tools available to help you with the rebalancing process. You can build your own tool from scratch to suit your needs and goals, or use the calculators and tools you find from others to make things easier for you. It’s really not that complicated so don’t let anyone tell you otherwise!

This is Money Crush, so feel free to copy our new Allocation and Rebalancing Worksheet to your Google Drive and have fun with it! And by the way, I froze some rows and columns in the worksheet because that’s the way I like it, but if you’re like Ali and you don’t want it to work that way you can unfreeze those rows and columns and make the worksheet function the way you want!

[…] Now check out Part 5! […]

LikeLike

[…] Part 5: Allocation and rebalancing […]

LikeLike

You always have such great content, it’s worth the wait! And I have to reread them about 4 times to start absorbing it all 🙂

I know that I have to decide for myself about my allocations .. but I sure wish there were some rules of thumb or guidelines I could lean on. I turned 50 last year and shifted from 80% in stocks to 70% stocks, 30% bonds/cash … but did not factor my home equity into that calculation at all. Mostly that’s because I have no intention or plan to sell so I don’t really consider my house when I think of my investments and net worth. Now I’m thinking that 70% might be too conservative, and that I should revisit, but .. we’ll see. I’m still planning to take a year off work (starting later this year!!) so figure it’s not the worst thing to leave my retirement savings a little conservatively invested while I’m too busy to pay close attention to them.

LikeLiked by 1 person

I think your approach regarding your home equity is good. And the new rule of thumb for doing your equity allocation is 120 – Age = Equity. So 120 -50 = 70. I think you are there!!!! And remember, the longer your retirement the higher your equities should drift. But 70% sounds good for now. Oh and how did you feel during the Ukranian Drop? And yes, if your house is not “liquid” then I would not add it to the equation. For us, everything is on the table so we wanted a way to include it in the equation. Can’t wait to hear about your year off. You must be getting excited.

LikeLike

I felt fine (mostly) during the drop. It’s funny, now that I consider myself Coast FI there wasn’t really any up side to the downturn, but I wasn’t worried or alarmed. Mostly annoyed because my accounts had been doing so well!

I’ll be more excited after my employer knows – right now it feels like living a double life to be making plans that are so different from daily life. Couple more weeks and all will be known!

LikeLiked by 1 person

Do drop us an email to let us know how your “notification” at work goes. And it sounds like you have successfully crossed over to managing your market reactions and that 70% is the right number for you at this point. It’s all good…

LikeLike

[…] in our Allocations Strategies Series we talked a lot about asset allocation and asset location. Keeping your investments in accounts […]

LikeLike